Potrebbero piacerti anche

- Istituzioni e Mercati FinanziariDocumento61 pagineIstituzioni e Mercati FinanziariMattia ZuccaNessuna valutazione finora

- Docsity Diritto Dei Mercati e Degli Intermediari Finanziari 1Documento96 pagineDocsity Diritto Dei Mercati e Degli Intermediari Finanziari 1Andrea MauroNessuna valutazione finora

- Mercati FinanziariDocumento52 pagineMercati Finanziarimainardis.mailNessuna valutazione finora

- Intermediari FinanziariDocumento106 pagineIntermediari FinanziariGregorio GalatiNessuna valutazione finora

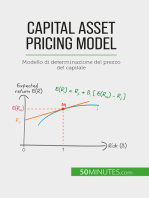

- Capital Asset Pricing Model: Modello di determinazione del prezzo del capitaleDa EverandCapital Asset Pricing Model: Modello di determinazione del prezzo del capitaleNessuna valutazione finora

- Struttura Organizzativa Di Una BancaDocumento60 pagineStruttura Organizzativa Di Una BancaAnonymous gxAd4liNessuna valutazione finora

- Diritto Delle BancheDocumento25 pagineDiritto Delle Banchekhalilmanaalla2909Nessuna valutazione finora

- LEZIONE Debito Mezzanino FinaleDocumento25 pagineLEZIONE Debito Mezzanino FinaleAlessandro Fiore NicchiaricoNessuna valutazione finora

- La psicologia dell'investimento: Educare la mente finanziaria per investire in modo consapevoleDa EverandLa psicologia dell'investimento: Educare la mente finanziaria per investire in modo consapevoleNessuna valutazione finora

- Economia Degli Intermediari FinanziariDocumento42 pagineEconomia Degli Intermediari FinanziarielisaNessuna valutazione finora

- Economia Degli Intermediari FinanziariDocumento5 pagineEconomia Degli Intermediari FinanziariHiba CrucianiNessuna valutazione finora

- Intermediari FinanziariDocumento135 pagineIntermediari FinanziarimatteoNessuna valutazione finora

- Azioni per principianti: Imparare a scegliere il proprio Portfolio, comprare/vendere quote e ad ottenere risultati redditizi a lungo termineDa EverandAzioni per principianti: Imparare a scegliere il proprio Portfolio, comprare/vendere quote e ad ottenere risultati redditizi a lungo termineNessuna valutazione finora

- Economia Degli Strumenti e AssicurativiDocumento19 pagineEconomia Degli Strumenti e AssicurativiMarvelAmericaNessuna valutazione finora

- Il Private Equity Nel Sistema Impresa.: 1.1 Considerazioni IntroduttiveDocumento29 pagineIl Private Equity Nel Sistema Impresa.: 1.1 Considerazioni IntroduttivemarioNessuna valutazione finora

- 17 - MERCATO MONETARIO CAP 20 e Poi MERCATO OBBLIGAZIONARIO CAP 21Documento12 pagine17 - MERCATO MONETARIO CAP 20 e Poi MERCATO OBBLIGAZIONARIO CAP 21GloriaNessuna valutazione finora

- Gli Intermediari Finanziari - Le BancheDocumento9 pagineGli Intermediari Finanziari - Le Bancheada.lanotte.d77Nessuna valutazione finora

- Appunti D Sistema Finanziario LIUCDocumento102 pagineAppunti D Sistema Finanziario LIUCMarioNessuna valutazione finora

- MERCATO AZIONARIO PER PRINCIPIANTI, Da Zero a Investitore Esperto! Cosa è e Come Guadagnare in Borsa. Impara Passo Passo ad acquistare le Azioni Giuste, Generare Dividendi e Accumulare Reddito Passivo.Da EverandMERCATO AZIONARIO PER PRINCIPIANTI, Da Zero a Investitore Esperto! Cosa è e Come Guadagnare in Borsa. Impara Passo Passo ad acquistare le Azioni Giuste, Generare Dividendi e Accumulare Reddito Passivo.Nessuna valutazione finora

- Tecnica BancariaDocumento51 pagineTecnica BancariaLedian PrekaNessuna valutazione finora

- La Borsa ValoriDocumento5 pagineLa Borsa ValoriTizioNessuna valutazione finora

- Economia Degli Intermediari FinanziariDocumento79 pagineEconomia Degli Intermediari FinanziarisaraNessuna valutazione finora

- Il consulente finanziario di 5° generazione. Come diventare imprenditore di successo, realizzare alleanze strategiche vincenti e realizzare un vantaggio competitivo duraturoDa EverandIl consulente finanziario di 5° generazione. Come diventare imprenditore di successo, realizzare alleanze strategiche vincenti e realizzare un vantaggio competitivo duraturoNessuna valutazione finora

- Lezioni Finanza AziendaleDocumento111 pagineLezioni Finanza AziendaleAprican ApriNessuna valutazione finora

- Lezioni Di Matematica FinanziariaDocumento476 pagineLezioni Di Matematica FinanziariaRobby MonteduroNessuna valutazione finora

- Riassunto Capitolo 5 Del Testo Di Marco Onado "Economia e Regolamentazione Del Sistema Finanziario" Il Mulino, 2008Documento10 pagineRiassunto Capitolo 5 Del Testo Di Marco Onado "Economia e Regolamentazione Del Sistema Finanziario" Il Mulino, 2008ClaytonSummerNessuna valutazione finora

- Rischi Particolari Nel Commercio Di Valori Mobiliari - ASBDocumento36 pagineRischi Particolari Nel Commercio Di Valori Mobiliari - ASBPresenzaDiLuceNessuna valutazione finora

- 13.a) Gli Intermediari Non BancariDocumento22 pagine13.a) Gli Intermediari Non Bancarigio040700Nessuna valutazione finora

- Le azioni rese semplici: La guida introduttiva agli investimenti in titoli azionari per capire cosa sono, come funzionano e quali sono le principali strategie operativeDa EverandLe azioni rese semplici: La guida introduttiva agli investimenti in titoli azionari per capire cosa sono, come funzionano e quali sono le principali strategie operativeNessuna valutazione finora

- Riassunto Economia - Degli.intermediari - Finanziari.banfi - Aprile.2016Documento69 pagineRiassunto Economia - Degli.intermediari - Finanziari.banfi - Aprile.2016carmebNessuna valutazione finora

- Economia Degli Intermediari FinanziariDocumento35 pagineEconomia Degli Intermediari FinanziariMatteo IngrossoNessuna valutazione finora

- 6 Dic - ECON POLITICADocumento7 pagine6 Dic - ECON POLITICAfrancescaobregon97Nessuna valutazione finora

- Arbitraje Financiero. MASCDocumento10 pagineArbitraje Financiero. MASCP. ISELA MELO PERALTANessuna valutazione finora

- 3.1 - Contratti e Mercati FinanziariDocumento52 pagine3.1 - Contratti e Mercati FinanziariViorel.sNessuna valutazione finora

- Riassunto IntermediariDocumento82 pagineRiassunto IntermediariAntonioAlbertoCocco100% (3)

- Economia Degli Intermediari FinanziariDocumento18 pagineEconomia Degli Intermediari Finanziarimariagreta.denotarpietro01Nessuna valutazione finora

- Riassunto Saunders Economia Mercati FinanziariDocumento86 pagineRiassunto Saunders Economia Mercati FinanziaritrusteverNessuna valutazione finora

- RPT 2 2777Documento12 pagineRPT 2 2777paoloNessuna valutazione finora

- Le Operazioni BancarieDocumento40 pagineLe Operazioni BancarieAntonella SciancaleporeNessuna valutazione finora

- WarrantDocumento84 pagineWarrantcannizzo45091Nessuna valutazione finora

- Domande Emif GiugnoDocumento4 pagineDomande Emif GiugnoGrazia BiscegliaNessuna valutazione finora

- Domande Esame EMIF 26042021Documento10 pagineDomande Esame EMIF 26042021Grazia BiscegliaNessuna valutazione finora

- Analisi Dei Mercati FinanziariDocumento37 pagineAnalisi Dei Mercati Finanziarispidey2001Nessuna valutazione finora

- Vol-6 Formazione Guida Al Trading Con I CFDDocumento19 pagineVol-6 Formazione Guida Al Trading Con I CFDpippolino1Nessuna valutazione finora

- Trading Online: Guida Completa per Guadagnare e Investire con Successo: Forex Trading, Day Trading, Swing Trading, Azioni, ETF, Indici, Strategia, Analisi Tecnica, Criptovalute: Business by Stefano Maini, #4Da EverandTrading Online: Guida Completa per Guadagnare e Investire con Successo: Forex Trading, Day Trading, Swing Trading, Azioni, ETF, Indici, Strategia, Analisi Tecnica, Criptovalute: Business by Stefano Maini, #4Nessuna valutazione finora

- 1 Il - Sistema - Finanziario - 10HDocumento20 pagine1 Il - Sistema - Finanziario - 10HPaolo GalloNessuna valutazione finora

- Il Mercato Dei CambiDocumento10 pagineIl Mercato Dei Cambicir.serpicoNessuna valutazione finora

- Preparazione Esame EMMDocumento6 paginePreparazione Esame EMMfgiuly32Nessuna valutazione finora

- Imparare a Diventare Redditizio Commerciante di opzioni: Swing TradingDa EverandImparare a Diventare Redditizio Commerciante di opzioni: Swing TradingNessuna valutazione finora

- Investire per principianti: Come raggiungere l'indipendenza finanziaria e far crescere la tua ricchezza attraverso l'immobiliare, il mercato azionario, le criptovalute, i fondi indicizzati, la proprietà in affitto, il trading di opzioni e più.Da EverandInvestire per principianti: Come raggiungere l'indipendenza finanziaria e far crescere la tua ricchezza attraverso l'immobiliare, il mercato azionario, le criptovalute, i fondi indicizzati, la proprietà in affitto, il trading di opzioni e più.Valutazione: 5 su 5 stelle5/5 (6)

- Scheda GLOBAL CONVERTIBLE BOND2Documento2 pagineScheda GLOBAL CONVERTIBLE BOND2Francesco VignaliNessuna valutazione finora

- MyAdvice - Novembre 2009Documento148 pagineMyAdvice - Novembre 2009intermarketandmoreNessuna valutazione finora

- Finanza AziendaleDocumento19 pagineFinanza AziendaleNiccolò GubianNessuna valutazione finora

- Glossario BancarioDocumento32 pagineGlossario BancarioMariana KapetanidouNessuna valutazione finora

- I FONDI COMUNI D’INVESTIMENTO RESI SEMPLICI. La guida introduttiva ai fondi comuni e alle strategie d'investimento più efficaci nel campo del risparmio gestito.Da EverandI FONDI COMUNI D’INVESTIMENTO RESI SEMPLICI. La guida introduttiva ai fondi comuni e alle strategie d'investimento più efficaci nel campo del risparmio gestito.Nessuna valutazione finora

- Economia Degli Intermediari Finanziari - Teoria e Esercizi Swap OpzioniDocumento23 pagineEconomia Degli Intermediari Finanziari - Teoria e Esercizi Swap OpzionibastianitoNessuna valutazione finora

- 10.a) La Disciplina Delle CrisiDocumento51 pagine10.a) La Disciplina Delle Crisigio040700Nessuna valutazione finora

- 11.b) Le A.I. Consob, Antitrust, Ecc.Documento21 pagine11.b) Le A.I. Consob, Antitrust, Ecc.gio040700Nessuna valutazione finora

- L'accesso Al Mercato BancarioDocumento42 pagineL'accesso Al Mercato Bancariogio040700Nessuna valutazione finora

- 13.a) Gli Intermediari Non BancariDocumento22 pagine13.a) Gli Intermediari Non Bancarigio040700Nessuna valutazione finora

- Le Crisi Economico-FinanziarieDocumento16 pagineLe Crisi Economico-Finanziariegio040700Nessuna valutazione finora

- Lucidi Lezione 19 Ottobre 2021 (Con Correzioni)Documento26 pagineLucidi Lezione 19 Ottobre 2021 (Con Correzioni)gio040700Nessuna valutazione finora

- Lucidi Lezione 19 Ottobre 2021 (Con Correzioni)Documento26 pagineLucidi Lezione 19 Ottobre 2021 (Con Correzioni)gio040700Nessuna valutazione finora

- La Musica Barocca PDFDocumento3 pagineLa Musica Barocca PDFPierpaoloNessuna valutazione finora

- Lezione 20Documento10 pagineLezione 20angeloNessuna valutazione finora

- Girotondo Di Tutto Il MondoDocumento3 pagineGirotondo Di Tutto Il MondoMatilde OrlandoNessuna valutazione finora

- CustomCrome LightingDocumento94 pagineCustomCrome LightingstopandgoNessuna valutazione finora