Potrebbero piacerti anche

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Profit and Loss - 21TDY 659Documento47 pagineProfit and Loss - 21TDY 659aakash rayNessuna valutazione finora

- Chap11 11e MicroDocumento45 pagineChap11 11e Microromeo626laNessuna valutazione finora

- SCM Sunil Chopra Chapter 2 DISCUSSION QUESTION.Documento11 pagineSCM Sunil Chopra Chapter 2 DISCUSSION QUESTION.Seher NazNessuna valutazione finora

- Revenue Reorganization ISA 18Documento7 pagineRevenue Reorganization ISA 18BakhtawarNessuna valutazione finora

- Jobs in AccoutingDocumento4 pagineJobs in AccoutingYilmer MartinezNessuna valutazione finora

- Ann Taylor Owns A Suit Tailoring Shop She Opened BusinessDocumento1 paginaAnn Taylor Owns A Suit Tailoring Shop She Opened Businesstrilocksp SinghNessuna valutazione finora

- EOQDocumento4 pagineEOQRavi SinghNessuna valutazione finora

- All Out Case StudyDocumento25 pagineAll Out Case StudyChris AlphonsoNessuna valutazione finora

- Putri Julia - 119211275Documento7 paginePutri Julia - 119211275Amara PrabasariNessuna valutazione finora

- Galadari PDFDocumento7 pagineGaladari PDFRDNessuna valutazione finora

- Entrepreneurship: Quarter 1 - Week 4 - Module 4Documento6 pagineEntrepreneurship: Quarter 1 - Week 4 - Module 4Darlene Dacanay DavidNessuna valutazione finora

- Goods X and Y Are Compliments WhileDocumento48 pagineGoods X and Y Are Compliments Whilem-amirNessuna valutazione finora

- Mandap Decoration Project ReportDocumento50 pagineMandap Decoration Project ReportNeha Marathe100% (1)

- THW5 London Hilton-1Documento2 pagineTHW5 London Hilton-1junho yoonNessuna valutazione finora

- Note 5-Accounting For Budgetary AccountsDocumento17 pagineNote 5-Accounting For Budgetary AccountsAngelica RubiosNessuna valutazione finora

- Value Under The Central Excise ActDocumento6 pagineValue Under The Central Excise ActChandu Aradhya S RNessuna valutazione finora

- SMS Script Test BlastingDocumento5 pagineSMS Script Test BlastingGabe Coyne100% (1)

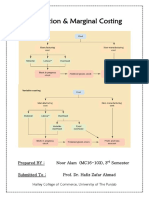

- Absorption & Marginal Costing - Noor Alam (MC16-103)Documento24 pagineAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- Indian Biscuit MarketDocumento15 pagineIndian Biscuit MarketRitushree RayNessuna valutazione finora

- Do Not Turn Over This Question Paper Until You Are Told To Do SoDocumento17 pagineDo Not Turn Over This Question Paper Until You Are Told To Do SoMin HeoNessuna valutazione finora

- Highly Competitive Warehouse Management: January 2012Documento46 pagineHighly Competitive Warehouse Management: January 2012prabhukamaraj26Nessuna valutazione finora

- CV RanjitDocumento3 pagineCV RanjitIto LawputraNessuna valutazione finora

- Nature & Scope of Managerial EconomicsDocumento9 pagineNature & Scope of Managerial EconomicsSuksham AnejaNessuna valutazione finora

- Executive: Stage 1Documento14 pagineExecutive: Stage 1Keka SamNessuna valutazione finora

- Examination Question and Answers, Set A (True or False), Chapter 1 - Introduction To Accounting and BusinessDocumento2 pagineExamination Question and Answers, Set A (True or False), Chapter 1 - Introduction To Accounting and BusinessJohn Carlos DoringoNessuna valutazione finora

- Solutions To Chapter 9 Using Discounted Cash-Flow Analysis To Make Investment DecisionsDocumento16 pagineSolutions To Chapter 9 Using Discounted Cash-Flow Analysis To Make Investment Decisionsmuhammad ihtishamNessuna valutazione finora

- PCS Model Explained 278Documento6 paginePCS Model Explained 278maged_abdnaghoNessuna valutazione finora

- Chapter 1 Accounting Equation - Double Entry BookkeepingDocumento5 pagineChapter 1 Accounting Equation - Double Entry BookkeepingKate BlossomNessuna valutazione finora

- Lesson 2 - Branches of AccountingDocumento15 pagineLesson 2 - Branches of AccountingLeizzamar BayadogNessuna valutazione finora

- Corporate Finance 10th Edition Ross Test Bank 1Documento70 pagineCorporate Finance 10th Edition Ross Test Bank 1james100% (39)