Potrebbero piacerti anche

- Change Point DetectionDocumento23 pagineChange Point DetectionSalbani ChakraborttyNessuna valutazione finora

- FlyletsDocumento1 paginaFlyletsKranthi KiranNessuna valutazione finora

- Asset and Equity VolatilitiesDocumento40 pagineAsset and Equity Volatilitiescorporateboy36596Nessuna valutazione finora

- Jackel 2006 - ByImplication PDFDocumento6 pagineJackel 2006 - ByImplication PDFpukkapadNessuna valutazione finora

- The Swiss Army Knife of Options Analytics: Vola DynamicsDocumento4 pagineThe Swiss Army Knife of Options Analytics: Vola DynamicsdanNessuna valutazione finora

- Predictingvolatility LazardresearchDocumento9 paginePredictingvolatility Lazardresearchhc87Nessuna valutazione finora

- MS&E448: Statistical Arbitrage: Group 5: Carolyn Soo, Zhengyi Lian, Jiayu Lou, Hang YangDocumento31 pagineMS&E448: Statistical Arbitrage: Group 5: Carolyn Soo, Zhengyi Lian, Jiayu Lou, Hang Yangakion xcNessuna valutazione finora

- From Implied To Spot Volatilities: Valdo DurrlemanDocumento21 pagineFrom Implied To Spot Volatilities: Valdo DurrlemanginovainmonaNessuna valutazione finora

- Option Trading: Pricing and Volatility Strategies and TechniquesDocumento5 pagineOption Trading: Pricing and Volatility Strategies and TechniquesrockochenNessuna valutazione finora

- Factor Investing RevisedDocumento22 pagineFactor Investing Revisedalexa_sherpyNessuna valutazione finora

- Derman Lectures SummaryDocumento30 pagineDerman Lectures SummaryPranay PankajNessuna valutazione finora

- AttilioMeucci BeyondBlackLittermanDocumento10 pagineAttilioMeucci BeyondBlackLittermanRichard LindseyNessuna valutazione finora

- SSRN d2715517Documento327 pagineSSRN d2715517hc87Nessuna valutazione finora

- Dupire Local VolatilityDocumento15 pagineDupire Local VolatilityJohn MclaughlinNessuna valutazione finora

- A Risk-Oriented Model For Factor Rotation DecisionsDocumento38 pagineA Risk-Oriented Model For Factor Rotation Decisionsxy053333Nessuna valutazione finora

- Deep HedgingDocumento21 pagineDeep HedgingRaju KaliperumalNessuna valutazione finora

- IEOR E4630 Spring 2016 SyllabusDocumento2 pagineIEOR E4630 Spring 2016 Syllabuscef4Nessuna valutazione finora

- Two Stage Fama MacbethDocumento5 pagineTwo Stage Fama Macbethkty21joy100% (1)

- Electronic Trading Masters: Secrets from the Pros!Da EverandElectronic Trading Masters: Secrets from the Pros!Nessuna valutazione finora

- Livevol Database StructureDocumento15 pagineLivevol Database StructureJuan LamadridNessuna valutazione finora

- Half-Day Reversal - QuantPediaDocumento7 pagineHalf-Day Reversal - QuantPediaJames LiuNessuna valutazione finora

- Copula Marginal AlgorithmDocumento17 pagineCopula Marginal AlgorithmCoolidgeLowNessuna valutazione finora

- Antoon Pelsser - Pricing Double Barrier Options Using Laplace Transforms PDFDocumento10 pagineAntoon Pelsser - Pricing Double Barrier Options Using Laplace Transforms PDFChun Ming Jeffy TamNessuna valutazione finora

- Static Versus Dynamic Hedging of Exotic OptionsDocumento29 pagineStatic Versus Dynamic Hedging of Exotic OptionsjustinlfangNessuna valutazione finora

- Guide To ACF PACF PlotsDocumento6 pagineGuide To ACF PACF Plotsajax_telamonioNessuna valutazione finora

- Hans Buehler DissDocumento164 pagineHans Buehler DissAgatha MurgociNessuna valutazione finora

- The IBS Effect Mean Reversion in Equity ETFsDocumento31 pagineThe IBS Effect Mean Reversion in Equity ETFstylerduNessuna valutazione finora

- Optimal Delta Hedging For OptionsDocumento11 pagineOptimal Delta Hedging For OptionsSandeep LimbasiyaNessuna valutazione finora

- Commodity Volatility SurfaceDocumento4 pagineCommodity Volatility SurfaceMarco Avello IbarraNessuna valutazione finora

- Dynamic Risk ParityDocumento31 pagineDynamic Risk ParityThe touristNessuna valutazione finora

- Options - ValuationDocumento37 pagineOptions - Valuationashu khetanNessuna valutazione finora

- SABR CalibrationDocumento21 pagineSABR CalibrationamitinamdarNessuna valutazione finora

- Sectors and Styles: A New Approach to Outperforming the MarketDa EverandSectors and Styles: A New Approach to Outperforming the MarketValutazione: 1 su 5 stelle1/5 (1)

- Trading Baskets ImplementationDocumento44 pagineTrading Baskets ImplementationSanchit Gupta100% (1)

- Rubisov Anton 201511 MAS ThesisDocumento94 pagineRubisov Anton 201511 MAS ThesisJose Antonio Dos RamosNessuna valutazione finora

- VolatilityDynamics DNicolay PrePrintDocumento411 pagineVolatilityDynamics DNicolay PrePrintIlias BenyekhlefNessuna valutazione finora

- Gamma Vanna and Higher Greek Exposure - Compiling The Dealer Order BookDocumento9 pagineGamma Vanna and Higher Greek Exposure - Compiling The Dealer Order BookArnaud FreycenetNessuna valutazione finora

- The Vol Smile Problem - FX FocusDocumento5 pagineThe Vol Smile Problem - FX FocusVeeken ChaglassianNessuna valutazione finora

- Auto Call Able SDocumento37 pagineAuto Call Able SAnkit VermaNessuna valutazione finora

- Bayesian Filtering: Dieter FoxDocumento132 pagineBayesian Filtering: Dieter FoxZoran BogoeskiNessuna valutazione finora

- FX Composite InstitutionalDocumento1 paginaFX Composite InstitutionalDanger AlvarezNessuna valutazione finora

- BLK Risk Factor Investing Revealed PDFDocumento8 pagineBLK Risk Factor Investing Revealed PDFShaun RodriguezNessuna valutazione finora

- A Simple and Reliable Way To Compute Option-Based Risk-Neutral DistributionsDocumento42 pagineA Simple and Reliable Way To Compute Option-Based Risk-Neutral Distributionsalanpicard2303Nessuna valutazione finora

- Log NormalDocumento12 pagineLog NormalAlexir86Nessuna valutazione finora

- Hull White PDFDocumento64 pagineHull White PDFstehbar9570Nessuna valutazione finora

- Earnings Theory PaperDocumento64 pagineEarnings Theory PaperPrateek SabharwalNessuna valutazione finora

- Arbitrage PresentationDocumento26 pagineArbitrage PresentationSanket PanditNessuna valutazione finora

- Drawbacks of Pearson CorrelationDocumento39 pagineDrawbacks of Pearson CorrelationZiyaNessuna valutazione finora

- Tactical Asset Allocation, Mebane FaberDocumento13 pagineTactical Asset Allocation, Mebane FabersashavladNessuna valutazione finora

- FCF Ch02 Excel Master StudentDocumento24 pagineFCF Ch02 Excel Master Studentannu technologyNessuna valutazione finora

- SSRN Id1997178Documento20 pagineSSRN Id1997178fahmiyusufNessuna valutazione finora

- Order Driven MarketDocumento42 pagineOrder Driven MarketXavier DaviasNessuna valutazione finora

- M7 Assignment - 72Documento18 pagineM7 Assignment - 72vickyNessuna valutazione finora

- 07a Hedge Funds and Performance EvaluationDocumento66 pagine07a Hedge Funds and Performance EvaluationdesbiauxNessuna valutazione finora

- Situation Index Handbook 2014Documento43 pagineSituation Index Handbook 2014kcousinsNessuna valutazione finora

- Lecture 11: Stochastic Volatility Models ContDocumento28 pagineLecture 11: Stochastic Volatility Models ContjefarnoNessuna valutazione finora

- 1improvement Algorithms of Perceptually Important P PDFDocumento5 pagine1improvement Algorithms of Perceptually Important P PDFredameNessuna valutazione finora

- Ishares Portfolio Analytics Coskew and CoKurt VBA3Documento178 pagineIshares Portfolio Analytics Coskew and CoKurt VBA3Peter Urbani100% (1)

- Partial Correlation Network Graph VBA (DJINDI)Documento463 paginePartial Correlation Network Graph VBA (DJINDI)Peter UrbaniNessuna valutazione finora

- Do You Have To Be Abnormal To Beat The MarketDocumento3 pagineDo You Have To Be Abnormal To Beat The MarketPeter UrbaniNessuna valutazione finora

- Random Forest in Excel and VBADocumento24 pagineRandom Forest in Excel and VBAPeter UrbaniNessuna valutazione finora

- Cholesky Versus SVDDocumento4 pagineCholesky Versus SVDPeter UrbaniNessuna valutazione finora

- Singular Spectrum Analysis Demo With VBADocumento12 pagineSingular Spectrum Analysis Demo With VBAPeter UrbaniNessuna valutazione finora

- Opalesque NewManagers July 2012Documento45 pagineOpalesque NewManagers July 2012Peter UrbaniNessuna valutazione finora

- Intra-Horizon VaR and Expected Shortfall Spreadsheet With VBADocumento7 pagineIntra-Horizon VaR and Expected Shortfall Spreadsheet With VBAPeter Urbani0% (1)

- Opalesque New Managers May 2012Documento51 pagineOpalesque New Managers May 2012Peter Urbani0% (1)

- Risk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Documento11 pagineRisk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Peter UrbaniNessuna valutazione finora

- Opalesque New Managers March 2012Documento37 pagineOpalesque New Managers March 2012Peter UrbaniNessuna valutazione finora

- Four Moment Risk Decomposition No VBADocumento13 pagineFour Moment Risk Decomposition No VBAPeter UrbaniNessuna valutazione finora

- How Well Does Your Hedge Fund HedgeDocumento2 pagineHow Well Does Your Hedge Fund HedgePeter UrbaniNessuna valutazione finora

- TLS Orthogonal Regression VBADocumento16 pagineTLS Orthogonal Regression VBAPeter Urbani0% (1)

- Opalesque New Managers May 2012Documento51 pagineOpalesque New Managers May 2012Peter Urbani0% (1)

- Liqudity VaR With Correct Time Scaling of Higher MomentsDocumento113 pagineLiqudity VaR With Correct Time Scaling of Higher MomentsPeter UrbaniNessuna valutazione finora

- Incremental and Marginal VaR Plus Infiniti 4 Moment Version No VBADocumento14 pagineIncremental and Marginal VaR Plus Infiniti 4 Moment Version No VBAPeter UrbaniNessuna valutazione finora

- Infiniti Capital Four Moment Risk DecompositionDocumento19 pagineInfiniti Capital Four Moment Risk DecompositionPeter UrbaniNessuna valutazione finora

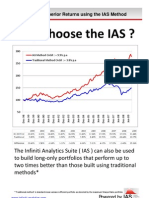

- Why Choose The IASDocumento6 pagineWhy Choose The IASPeter UrbaniNessuna valutazione finora

- Midterm Exam - Answer Key: Professor Salyer, Economics 135, Spring 2009Documento2 pagineMidterm Exam - Answer Key: Professor Salyer, Economics 135, Spring 2009kasimNessuna valutazione finora

- MiniCase Assignment 9 PDFDocumento19 pagineMiniCase Assignment 9 PDF2013study100% (1)

- KANANIIND 29062022112051 KILClosurewindowDocumento1 paginaKANANIIND 29062022112051 KILClosurewindowBharat MahanNessuna valutazione finora

- Factors Affecting Cost of CapitalDocumento40 pagineFactors Affecting Cost of CapitalKartik AroraNessuna valutazione finora

- Icfai2008 - 1307514033 Security AnalysisDocumento17 pagineIcfai2008 - 1307514033 Security AnalysisJatin GoyalNessuna valutazione finora

- Investment Management Analysis: Your Company NameDocumento70 pagineInvestment Management Analysis: Your Company NameJojoMagnoNessuna valutazione finora

- NHMFCDocumento20 pagineNHMFCJohn Emanuel Alcantara100% (1)

- Corporate Governance AnnexDocumento1 paginaCorporate Governance AnnexJumoke FadareNessuna valutazione finora

- Report On Venture Capital in IndiaDocumento60 pagineReport On Venture Capital in IndiaShubham More CenationNessuna valutazione finora

- ValuationDocumento85 pagineValuationsamNessuna valutazione finora

- Opening Day Balance SheetDocumento2 pagineOpening Day Balance Sheetapi-3809857Nessuna valutazione finora

- Michel Aglietta, Antoine Reberioux - Corporate Governance Adrift - A Critique of Shareholder Value (Saint-Gobain Centre For Economic Studies) (2005)Documento321 pagineMichel Aglietta, Antoine Reberioux - Corporate Governance Adrift - A Critique of Shareholder Value (Saint-Gobain Centre For Economic Studies) (2005)Ricardo ValenzuelaNessuna valutazione finora

- Fooled by RandomnessDocumento3 pagineFooled by RandomnessHarshdeep SinghNessuna valutazione finora

- Afm (Acca)Documento13 pagineAfm (Acca)Anmol SahajwaniNessuna valutazione finora

- 2 Business Law, 63 - 81Documento18 pagine2 Business Law, 63 - 81s4sahithNessuna valutazione finora

- A Catalyst For Growth in Africa: Access Bank PLCDocumento160 pagineA Catalyst For Growth in Africa: Access Bank PLCBenedict TawiahNessuna valutazione finora

- Xii B.studies CH-10 Financial Market PDFDocumento5 pagineXii B.studies CH-10 Financial Market PDFRockyNessuna valutazione finora

- ICICI Direct - Research ReportDocumento4 pagineICICI Direct - Research ReportMudit KediaNessuna valutazione finora

- Axis Bank Report.Documento11 pagineAxis Bank Report.Rajat NidoniNessuna valutazione finora

- Harvard Case Study Toy WorldDocumento19 pagineHarvard Case Study Toy WorldHomework Ping100% (1)

- Technical InfosysDocumento13 pagineTechnical InfosysPrakhar RatheeNessuna valutazione finora

- 1 Which of The Following Best Describes International FinancialDocumento2 pagine1 Which of The Following Best Describes International FinancialM Bilal SaleemNessuna valutazione finora

- FIDO's Budget Planner: Start HereDocumento2 pagineFIDO's Budget Planner: Start HereJose MagcalasNessuna valutazione finora

- GP Investments: Annual ReportDocumento54 pagineGP Investments: Annual ReportLicaBorgesNessuna valutazione finora

- Assessment of Future Exchange Rate MovementsDocumento3 pagineAssessment of Future Exchange Rate MovementsNafiz Zaman100% (1)

- Welcome .: Presented by Tatenda MazuruseDocumento21 pagineWelcome .: Presented by Tatenda Mazurusetatenda mazuruseNessuna valutazione finora

- Bank Practice and Procedures (Acfn2113) : Prepared By: Tewodros EDocumento37 pagineBank Practice and Procedures (Acfn2113) : Prepared By: Tewodros Eመስቀል ኃይላችን ነውNessuna valutazione finora

- Math and The Stock MarketDocumento3 pagineMath and The Stock MarketKim Nicole ObelNessuna valutazione finora

- Summary Hybrid Financing (18!11!2021)Documento5 pagineSummary Hybrid Financing (18!11!2021)Shafa ENessuna valutazione finora

- Clearing Services For Global MarketsDocumento570 pagineClearing Services For Global MarketsXozi Duhok100% (1)