Potrebbero piacerti anche

- Accounting TheoryDocumento32 pagineAccounting TheoryKanika KathpaliaNessuna valutazione finora

- Accounting TheoryDocumento27 pagineAccounting TheoryRaisa Yuliana FitranieNessuna valutazione finora

- MBA-AFM Theory QBDocumento18 pagineMBA-AFM Theory QBkanikaNessuna valutazione finora

- Acca NotesDocumento100 pagineAcca Notesasifkazmi100% (2)

- 2.basic Rules of AccountingDocumento9 pagine2.basic Rules of AccountingBhuvaneswari karuturiNessuna valutazione finora

- Understanding Financial StatementsDocumento151 pagineUnderstanding Financial StatementsCj Lumoctos100% (1)

- Issues in Financial Reporting Izza Urooj Sap Id 6884 Sir AmanullahDocumento11 pagineIssues in Financial Reporting Izza Urooj Sap Id 6884 Sir AmanullahAli AwanNessuna valutazione finora

- 413 Block1Documento208 pagine413 Block1Subramanyam Devarakonda100% (1)

- 1.01 Understanding Financial StatementDocumento14 pagine1.01 Understanding Financial StatementHardik MistryNessuna valutazione finora

- Course: Financial Accounting & AnalysisDocumento16 pagineCourse: Financial Accounting & Analysiskarunakar vNessuna valutazione finora

- Accounting Notes Essential Features of Accounting PrinciplesDocumento13 pagineAccounting Notes Essential Features of Accounting PrinciplesGM BalochNessuna valutazione finora

- Branches of AccountingDocumento6 pagineBranches of AccountingTrisha RagonotNessuna valutazione finora

- Brave Brands AccountingDocumento6 pagineBrave Brands AccountingNgoni MukukuNessuna valutazione finora

- Accounts SuggestionsDocumento18 pagineAccounts SuggestionsDipon GhoshNessuna valutazione finora

- The Management of The Finances of A Business / Organisation in Order To Achieve Financial ObjectivesDocumento12 pagineThe Management of The Finances of A Business / Organisation in Order To Achieve Financial ObjectivesPrince GoyalNessuna valutazione finora

- F & M AccountingDocumento6 pagineF & M AccountingCherry PieNessuna valutazione finora

- Accounting For ManagementDocumento23 pagineAccounting For Managementgarusha gautamNessuna valutazione finora

- Accounting For Managers Assignment 1 and 2 Answer SheetDocumento12 pagineAccounting For Managers Assignment 1 and 2 Answer SheetarifNessuna valutazione finora

- Fa Unit 1 - Notes - 20200718004241Documento21 pagineFa Unit 1 - Notes - 20200718004241Vignesh CNessuna valutazione finora

- Company Management. The Management Team Needs To Understand TheDocumento3 pagineCompany Management. The Management Team Needs To Understand TheGopali AoshieaneNessuna valutazione finora

- Essentials of Financial Accounting - 1st SEMDocumento10 pagineEssentials of Financial Accounting - 1st SEMParichay PalNessuna valutazione finora

- Acc Assign1Documento24 pagineAcc Assign1chandresh_johnsonNessuna valutazione finora

- BBA203Documento13 pagineBBA203Mrinal KalitaNessuna valutazione finora

- Accounting Final AssignmentDocumento16 pagineAccounting Final AssignmentRoss3568Nessuna valutazione finora

- Accounting Principles Volume 1 Canadian 7th Edition Geygandt Test BankDocumento48 pagineAccounting Principles Volume 1 Canadian 7th Edition Geygandt Test BankJosephWilliamsostmdNessuna valutazione finora

- f1.3 Financial Acoounting CpaDocumento173 paginef1.3 Financial Acoounting CpaCyiza Ben RubenNessuna valutazione finora

- Unit 6 - Accounting Concepts Standards-1Documento20 pagineUnit 6 - Accounting Concepts Standards-1evalynmoyo5Nessuna valutazione finora

- 7.1.1 Record Keeping: It Is Necessary To Have Good Records For Effective Control and For Tax PurposesDocumento9 pagine7.1.1 Record Keeping: It Is Necessary To Have Good Records For Effective Control and For Tax PurposesTarekegnNessuna valutazione finora

- Accounts NotesDocumento12 pagineAccounts NotesRishi KumarNessuna valutazione finora

- Accounting ConceptsDocumento11 pagineAccounting ConceptssyedasadaligardeziNessuna valutazione finora

- Student Name: Mac Guiver Castro Sánchez Student ID: VTI18197 BSBFIM601 Manage FinancesDocumento25 pagineStudent Name: Mac Guiver Castro Sánchez Student ID: VTI18197 BSBFIM601 Manage FinancesPriyanka AggarwalNessuna valutazione finora

- Accounting Period Shareholders DividendsDocumento3 pagineAccounting Period Shareholders DividendsAmaranathreddy YgNessuna valutazione finora

- Creative AccountingDocumento13 pagineCreative AccountingMira CE100% (1)

- Examples of Current Assets IncludeDocumento4 pagineExamples of Current Assets IncludeMujahidNessuna valutazione finora

- Accounts NotesDocumento12 pagineAccounts NotesRishi KumarNessuna valutazione finora

- Lesson-2 Generally Accepted Accounting Principles and Accounting StandardsDocumento10 pagineLesson-2 Generally Accepted Accounting Principles and Accounting StandardsKarthigeyan Balasubramaniam100% (1)

- Fundamentals of Accountancy, Business and Management 1: Module 2"Documento68 pagineFundamentals of Accountancy, Business and Management 1: Module 2"Erica AlbaoNessuna valutazione finora

- Chapter 1: Session 1 Introduction To Financial AccountingDocumento161 pagineChapter 1: Session 1 Introduction To Financial AccountingHarshini Akilandan100% (1)

- Solution Manual For Financial Accounting An Integrated Approach 5th Edition by TrotmanDocumento21 pagineSolution Manual For Financial Accounting An Integrated Approach 5th Edition by Trotmana540142314Nessuna valutazione finora

- Assignment CH-1 Introduction To AccountingDocumento7 pagineAssignment CH-1 Introduction To AccountingHarsh SachdevaNessuna valutazione finora

- Lesson One AccountsDocumento7 pagineLesson One AccountslucyotienoNessuna valutazione finora

- Accounting For Manager Complete NotesDocumento105 pagineAccounting For Manager Complete NotesAARTI100% (2)

- Lecture One Role of Accounting in SocietyDocumento10 pagineLecture One Role of Accounting in SocietyJagadeep Reddy BhumireddyNessuna valutazione finora

- Bcom QbankDocumento13 pagineBcom QbankIshaNessuna valutazione finora

- Chapter 3Documento5 pagineChapter 3Janah MirandaNessuna valutazione finora

- KTTC lý thuyếtDocumento22 pagineKTTC lý thuyếtAnh Tùng VũNessuna valutazione finora

- Task 2Documento18 pagineTask 2Yashmi BhanderiNessuna valutazione finora

- Chapter 5 Principls and ConceptsDocumento10 pagineChapter 5 Principls and ConceptsawlachewNessuna valutazione finora

- Theoretical Framework of AccountingDocumento13 pagineTheoretical Framework of Accountingmarksuudi2000Nessuna valutazione finora

- Unit 2-Accounting Concepts, Principles and ConventionsDocumento20 pagineUnit 2-Accounting Concepts, Principles and Conventionsanamikarajendran441998Nessuna valutazione finora

- Inbound 3522308407029868205Documento18 pagineInbound 3522308407029868205KupalNessuna valutazione finora

- Consolidated Financial StatementsDocumento32 pagineConsolidated Financial StatementsPeetu WadhwaNessuna valutazione finora

- Generally Accepted Accounting Principles (GAAP) Is A Term Used To Refer To The StandardDocumento6 pagineGenerally Accepted Accounting Principles (GAAP) Is A Term Used To Refer To The StandardRahul JainNessuna valutazione finora

- Chapter 1 Accounting ConceptsDocumento6 pagineChapter 1 Accounting ConceptsJamEs Luna MaTudioNessuna valutazione finora

- Lecture 1 Financial AccountingDocumento5 pagineLecture 1 Financial Accountingzubdasyeda8Nessuna valutazione finora

- Notes For Chapter 1 Igcse AccountsDocumento4 pagineNotes For Chapter 1 Igcse Accountsbhumilimbadiya09_216Nessuna valutazione finora

- Accountancy and ManagementDocumento19 pagineAccountancy and ManagementLiwash SaikiaNessuna valutazione finora

- FM SummaryDocumento11 pagineFM Summaryannemijn kraaijkampNessuna valutazione finora

- Financial Accounting For Managers Unit 1 Mba Sem 1Documento13 pagineFinancial Accounting For Managers Unit 1 Mba Sem 1Mohit TripathiNessuna valutazione finora

- A Study On Investment Behavior of Women InvestorsDocumento1 paginaA Study On Investment Behavior of Women InvestorsMegha PatelNessuna valutazione finora

- Course-Outline-Corporate Housekeeping PDFDocumento3 pagineCourse-Outline-Corporate Housekeeping PDFred_inajNessuna valutazione finora

- RatingsScale 2008 PDFDocumento13 pagineRatingsScale 2008 PDFPradeep272Nessuna valutazione finora

- SA Case StudyDocumento6 pagineSA Case StudyKanika MaheshwariNessuna valutazione finora

- GSA TestDocumento14 pagineGSA TestYuvaraj BaghmarNessuna valutazione finora

- Trust LineDocumento106 pagineTrust LineGuman SinghNessuna valutazione finora

- Raise MillionsDocumento148 pagineRaise MillionsMatthew McClendonNessuna valutazione finora

- Stock MKT IndicesDocumento20 pagineStock MKT IndicesDivyesh GandhiNessuna valutazione finora

- Ratio AnalysisDocumento12 pagineRatio AnalysisMrunmayee MirashiNessuna valutazione finora

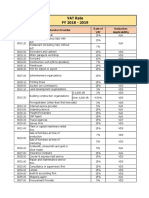

- Bangladesh Tax & VAT Rate 2018-19Documento6 pagineBangladesh Tax & VAT Rate 2018-19IFTEKHAR IFTE83% (24)

- Rfa Business Plan Template v2Documento37 pagineRfa Business Plan Template v2arunimdrNessuna valutazione finora

- 12 Principles of Intelligent InvestorsDocumento27 pagine12 Principles of Intelligent InvestorsJohn KohNessuna valutazione finora

- Commercial Accounmts ManualDocumento137 pagineCommercial Accounmts ManualRK K100% (3)

- 2.jimenez vs. FranciscoDocumento2 pagine2.jimenez vs. FranciscoCJOY FALOGMENessuna valutazione finora

- Data Hackathon: Bc3406 Business Analytics ConsultingDocumento175 pagineData Hackathon: Bc3406 Business Analytics ConsultingjohnconnorNessuna valutazione finora

- An Introduction To Hedge Funds - PaperDocumento32 pagineAn Introduction To Hedge Funds - PaperulrichoNessuna valutazione finora

- Putin's Revenge!Documento3 paginePutin's Revenge!eTradingPicksNessuna valutazione finora

- Chapter 20 - MenbiDocumento41 pagineChapter 20 - MenbiMayadianaSugondo100% (1)

- Midterm Sample Options and DerivativesDocumento2 pagineMidterm Sample Options and DerivativeskevinNessuna valutazione finora

- CURRENT PRICING OF IPOs: Is It Investor-Friendly?Documento53 pagineCURRENT PRICING OF IPOs: Is It Investor-Friendly?Sayam RoyNessuna valutazione finora

- 2021.03.09.2 - Social ResponsibilityDocumento18 pagine2021.03.09.2 - Social ResponsibilityJulia Marie CausonNessuna valutazione finora

- Corporate Finance 9th Edition Ross Test BankDocumento53 pagineCorporate Finance 9th Edition Ross Test Bankarnoldmelanieip30l100% (20)

- BSE TASIS Shariah 50 Index FactsheetDocumento3 pagineBSE TASIS Shariah 50 Index FactsheetkayalonthewebNessuna valutazione finora

- Selby Jennings - Year in Review and 2022 Outlook With Salary Guide (South East Asia)Documento23 pagineSelby Jennings - Year in Review and 2022 Outlook With Salary Guide (South East Asia)BIN LUNessuna valutazione finora

- Aboitiz FinalDocumento22 pagineAboitiz FinalCharmaineCuetoNessuna valutazione finora

- Colege ReportDocumento51 pagineColege ReportVarun WayneNessuna valutazione finora

- My View On Organovo (Over-) ValuationDocumento7 pagineMy View On Organovo (Over-) ValuationUnemonNessuna valutazione finora

- PEIGG Valuation Guidelines - Final Version - 1Documento14 paginePEIGG Valuation Guidelines - Final Version - 1cjende1Nessuna valutazione finora

- Seminar 9 - QuestionsDocumento2 pagineSeminar 9 - QuestionsSlice LeNessuna valutazione finora

- Headlines CollectionDocumento72 pagineHeadlines CollectionAdam TylerNessuna valutazione finora