Potrebbero piacerti anche

- The Art of Persuasion: Cold Calling Home Sellers for Owner Financing OpportunitiesDa EverandThe Art of Persuasion: Cold Calling Home Sellers for Owner Financing OpportunitiesNessuna valutazione finora

- Unleashing Wealth: A Guide to BRRRR Real Estate Investing: Real Estate Investing, #13Da EverandUnleashing Wealth: A Guide to BRRRR Real Estate Investing: Real Estate Investing, #13Nessuna valutazione finora

- Islamic Financial ProductDocumento13 pagineIslamic Financial ProductKelvin Lim Wei QuanNessuna valutazione finora

- Bank Al Habib Car FinanceDocumento9 pagineBank Al Habib Car Financefatima rahimNessuna valutazione finora

- Diminishing Musharakah Presentation 02-06-08Documento32 pagineDiminishing Musharakah Presentation 02-06-08AlHuda Centre of Islamic Banking & Economics (CIBE)Nessuna valutazione finora

- Diminishing Musharakah: Mahmood ShafqatDocumento32 pagineDiminishing Musharakah: Mahmood ShafqatAli KhanNessuna valutazione finora

- Diminishing Musharaka IjarahBasedDocumento22 pagineDiminishing Musharaka IjarahBasedArsalan AqeeqNessuna valutazione finora

- Islamic Financial Accounting Standards To Ijarah by Ahmed AlDocumento23 pagineIslamic Financial Accounting Standards To Ijarah by Ahmed AlAsadZahidNessuna valutazione finora

- Accounting For InvestmentDocumento29 pagineAccounting For InvestmentSyahrul AmirulNessuna valutazione finora

- Financialservices: Kanika BhasinDocumento14 pagineFinancialservices: Kanika BhasinkanikaNessuna valutazione finora

- Merchant BankingDocumento20 pagineMerchant Bankingpranab paulNessuna valutazione finora

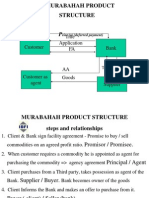

- Murabahah Product Structure: Title Application FADocumento26 pagineMurabahah Product Structure: Title Application FAUmair UddinNessuna valutazione finora

- Venture CapitalDocumento17 pagineVenture CapitalVidhyaBalaNessuna valutazione finora

- ISBF NotesDocumento13 pagineISBF Notesmuneebmateen01Nessuna valutazione finora

- Alinma BankDocumento4 pagineAlinma BankAnonymous bwQj7OgNessuna valutazione finora

- Chp4. Application of Islamic Lease FinancingDocumento35 pagineChp4. Application of Islamic Lease FinancingUsaama AbdilaahiNessuna valutazione finora

- Corporate Banking: Funded Services Lending /advances CB-CHPP07Documento40 pagineCorporate Banking: Funded Services Lending /advances CB-CHPP07Prakash SharmaNessuna valutazione finora

- Diminishing Musharakah ConceptDocumento26 pagineDiminishing Musharakah ConceptHasan Irfan SiddiquiNessuna valutazione finora

- All SlidesDocumento31 pagineAll SlidessinginiwizNessuna valutazione finora

- Lecture6 FinancingPart2Documento29 pagineLecture6 FinancingPart2Ry NielNessuna valutazione finora

- Procedure For Loan For Property Under The Master TitleDocumento17 pagineProcedure For Loan For Property Under The Master TitleKelvin PoptaniNessuna valutazione finora

- Difference and Similarities in Islamic ADocumento16 pagineDifference and Similarities in Islamic ASayed Sharif HashimiNessuna valutazione finora

- Substance Over Form-1Documento20 pagineSubstance Over Form-1Ashura ShaibNessuna valutazione finora

- If-1Documento27 pagineIf-1Asad MemonNessuna valutazione finora

- Introduction To Ijarah: Release DateDocumento21 pagineIntroduction To Ijarah: Release Datewafa shumailNessuna valutazione finora

- Investment Banking, Credit Rating, Leasing: Pradeep Kumar MishraDocumento25 pagineInvestment Banking, Credit Rating, Leasing: Pradeep Kumar Mishrasunit dasNessuna valutazione finora

- Bank Guarantees and Trade FinanceDocumento14 pagineBank Guarantees and Trade Finance1221Nessuna valutazione finora

- Vehicle Financing Products PDFDocumento22 pagineVehicle Financing Products PDFNurulhikmah RoslanNessuna valutazione finora

- Chapter 6 Application of Funds - Financing Facilities and The Underlying Shariah ConceptsDocumento94 pagineChapter 6 Application of Funds - Financing Facilities and The Underlying Shariah Conceptsamirol93Nessuna valutazione finora

- Uses of Bank Funds: The Lending FunctionDocumento21 pagineUses of Bank Funds: The Lending FunctionAKSHAY BHADAURIANessuna valutazione finora

- Valuation of CollateralDocumento24 pagineValuation of CollateralLuningning Carios100% (1)

- Loan SyndicationDocumento30 pagineLoan SyndicationMegha BhatnagarNessuna valutazione finora

- Islamic Sales Contracts StructureDocumento54 pagineIslamic Sales Contracts StructureFaisal Mir100% (1)

- First Slide Mortgage Market Second Slide Mortgage MarketDocumento6 pagineFirst Slide Mortgage Market Second Slide Mortgage MarketArlene GarciaNessuna valutazione finora

- Islamic Banking: Presented by Lakshmi and ShameemDocumento21 pagineIslamic Banking: Presented by Lakshmi and ShameemvidyaposhakNessuna valutazione finora

- Securitisation of Debt AssetsDocumento24 pagineSecuritisation of Debt AssetsANITTA M. AntonyNessuna valutazione finora

- Commercial Banking Lending Policies of BanksDocumento47 pagineCommercial Banking Lending Policies of Banksrahul8909Nessuna valutazione finora

- SYBBA Unit 4Documento40 pagineSYBBA Unit 4idea8433Nessuna valutazione finora

- Investment Banking UnderwritingDocumento25 pagineInvestment Banking UnderwritingGaurav GuptaNessuna valutazione finora

- House FinancingDocumento32 pagineHouse FinancingRowena YenXinNessuna valutazione finora

- SARFESI (Securitisation & Reconstruction and Enforcement of Security Interest)Documento22 pagineSARFESI (Securitisation & Reconstruction and Enforcement of Security Interest)BaazingaFeedsNessuna valutazione finora

- Indian Accounting Standard 23 - Borrowing CostDocumento10 pagineIndian Accounting Standard 23 - Borrowing CostSonali LadiNessuna valutazione finora

- Bank Credit - : Loans & AdvancesDocumento75 pagineBank Credit - : Loans & AdvancesNikhilrajsingh ShekhawatNessuna valutazione finora

- SecuritizationDocumento23 pagineSecuritizationHarshit NagpalNessuna valutazione finora

- FSA 4 Financing ActivitiesDocumento51 pagineFSA 4 Financing Activitiessubhrodeep chowdhuryNessuna valutazione finora

- FM LeasingDocumento15 pagineFM Leasingritam chakrabortyNessuna valutazione finora

- Dr. S.G. Rama Rao: Financial ServicesDocumento20 pagineDr. S.G. Rama Rao: Financial ServicesthensureshNessuna valutazione finora

- Chapter4. BankingDocumento38 pagineChapter4. BankingdhitalkhushiNessuna valutazione finora

- Borrowing Causes For Customers and Related Financing ProductsDocumento18 pagineBorrowing Causes For Customers and Related Financing Productssam30121989Nessuna valutazione finora

- Sarfaesi ActDocumento7 pagineSarfaesi ActBhakti Bhushan MishraNessuna valutazione finora

- Diminishing Musharakah - MBL - PpsDocumento17 pagineDiminishing Musharakah - MBL - Ppsgul_e_sabaNessuna valutazione finora

- Chapter 6 - Islamic Home LoansDocumento7 pagineChapter 6 - Islamic Home LoansVIDHYA A P PANIRSELVAM UnknownNessuna valutazione finora

- Corporate Banking Activities: Chapter Three DTG 3483Documento26 pagineCorporate Banking Activities: Chapter Three DTG 3483Nini MohamedNessuna valutazione finora

- Meezan Bank PresentationDocumento17 pagineMeezan Bank PresentationHussnain RazaNessuna valutazione finora

- Credit Mgt. - WEBILT - DeckDocumento287 pagineCredit Mgt. - WEBILT - Decksimran kaur100% (1)

- Final FMDocumento57 pagineFinal FMRuchi GandhiNessuna valutazione finora

- Financial Accounting and Reporting - InvestmentsDocumento10 pagineFinancial Accounting and Reporting - InvestmentsLuisitoNessuna valutazione finora

- Diminishing Musharakah MBLDocumento17 pagineDiminishing Musharakah MBLUbaid ArifNessuna valutazione finora

- Who Am I KiddingDocumento2 pagineWho Am I KiddingFarrah EmmylyaNessuna valutazione finora

- Reporting and Analysing LiabilitiesDocumento52 pagineReporting and Analysing LiabilitiesSuptoNessuna valutazione finora

- CUET 2022 General Test 6th October Shift 1Documento23 pagineCUET 2022 General Test 6th October Shift 1Dhruv BhardwajNessuna valutazione finora

- Forces L2 Measuring Forces WSDocumento4 pagineForces L2 Measuring Forces WSAarav KapoorNessuna valutazione finora

- Vintage Airplane - May 1982Documento24 pagineVintage Airplane - May 1982Aviation/Space History LibraryNessuna valutazione finora

- Pontevedra 1 Ok Action PlanDocumento5 paginePontevedra 1 Ok Action PlanGemma Carnecer Mongcal50% (2)

- SKF Shaft Alignment Tool TKSA 41Documento2 pagineSKF Shaft Alignment Tool TKSA 41Dwiki RamadhaniNessuna valutazione finora

- R15 Understanding Business CyclesDocumento33 pagineR15 Understanding Business CyclesUmar FarooqNessuna valutazione finora

- Mahatma Gandhi University: Priyadarshini Hills, Kottayam-686560Documento136 pagineMahatma Gandhi University: Priyadarshini Hills, Kottayam-686560Rashmee DwivediNessuna valutazione finora

- Thermodynamic c106Documento120 pagineThermodynamic c106Драгослав БјелицаNessuna valutazione finora

- Chapter 13Documento15 pagineChapter 13anormal08Nessuna valutazione finora

- Thesis On Retail Management of The Brand 'Sleepwell'Documento62 pagineThesis On Retail Management of The Brand 'Sleepwell'Sajid Lodha100% (1)

- Chunking Chunking Chunking: Stator Service IssuesDocumento1 paginaChunking Chunking Chunking: Stator Service IssuesGina Vanessa Quintero CruzNessuna valutazione finora

- Individual Daily Log and Accomplishment Report: Date and Actual Time Logs Actual AccomplishmentsDocumento3 pagineIndividual Daily Log and Accomplishment Report: Date and Actual Time Logs Actual AccomplishmentsMarian SalazarNessuna valutazione finora

- DLI Watchman®: Vibration Screening Tool BenefitsDocumento2 pagineDLI Watchman®: Vibration Screening Tool Benefitssinner86Nessuna valutazione finora

- Ged 102 Mathematics in The Modern WorldDocumento84 pagineGed 102 Mathematics in The Modern WorldKier FormelozaNessuna valutazione finora

- Ransomware: Prevention and Response ChecklistDocumento5 pagineRansomware: Prevention and Response Checklistcapodelcapo100% (1)

- Instruction Manual 115cx ENGLISHDocumento72 pagineInstruction Manual 115cx ENGLISHRomanPiscraftMosqueteerNessuna valutazione finora

- Barista Skills Foundation Curriculum enDocumento4 pagineBarista Skills Foundation Curriculum enCezara CarteșNessuna valutazione finora

- Level Swiches Data SheetDocumento4 pagineLevel Swiches Data SheetROGELIO QUIJANONessuna valutazione finora

- Ariba Collaborative Sourcing ProfessionalDocumento2 pagineAriba Collaborative Sourcing Professionalericofx530Nessuna valutazione finora

- Nse 2Documento5 pagineNse 2dhaval gohelNessuna valutazione finora

- What Are The Advantages and Disadvantages of UsingDocumento4 pagineWhat Are The Advantages and Disadvantages of UsingJofet Mendiola88% (8)

- Gmail - ICICI BANK I PROCESS HIRING FOR BACKEND - OPERATION PDFDocumento2 pagineGmail - ICICI BANK I PROCESS HIRING FOR BACKEND - OPERATION PDFDeepankar ChoudhuryNessuna valutazione finora

- Property House Invests $1b in UAE Realty - TBW May 25 - Corporate FocusDocumento1 paginaProperty House Invests $1b in UAE Realty - TBW May 25 - Corporate FocusjiminabottleNessuna valutazione finora

- CL200 PLCDocumento158 pagineCL200 PLCJavierRuizThorrensNessuna valutazione finora

- Process Description of Function For Every Unit OperationDocumento3 pagineProcess Description of Function For Every Unit OperationMauliduni M. AuniNessuna valutazione finora

- Mangement of Shipping CompaniesDocumento20 pagineMangement of Shipping CompaniesSatyam MishraNessuna valutazione finora

- BKNC3 - Activity 1 - Review ExamDocumento3 pagineBKNC3 - Activity 1 - Review ExamDhel Cahilig0% (1)

- Roland Fantom s88Documento51 pagineRoland Fantom s88harryoliff2672100% (1)

- Yarn HairinessDocumento9 pagineYarn HairinessGhandi AhmadNessuna valutazione finora

- Bin Adam Group of CompaniesDocumento8 pagineBin Adam Group of CompaniesSheema AhmadNessuna valutazione finora