Potrebbero piacerti anche

- IC 92 Multiple Question BankDocumento54 pagineIC 92 Multiple Question BankTRANSFORMERLOGICS90% (10)

- M9notes PDFDocumento131 pagineM9notes PDFMandy WongNessuna valutazione finora

- CHAPTER 14 Bailment PledgeDocumento13 pagineCHAPTER 14 Bailment PledgeRajesh BazadNessuna valutazione finora

- Bonds PayableDocumento34 pagineBonds PayableArgem Jay PorioNessuna valutazione finora

- Banker Customer Relationship To Be Revised 7Documento19 pagineBanker Customer Relationship To Be Revised 7Anonymous bf1cFDuepPNessuna valutazione finora

- Banker Customer RelationshipDocumento30 pagineBanker Customer RelationshipnupurNessuna valutazione finora

- Drafting PDFDocumento11 pagineDrafting PDFsouvikNessuna valutazione finora

- Letter of CreditDocumento3 pagineLetter of CreditRakesh_Kumar_A_8181Nessuna valutazione finora

- Taxation - Business and ProfessionDocumento45 pagineTaxation - Business and ProfessionSanah Bijlani67% (3)

- Liquidation of CompaniesDocumento34 pagineLiquidation of CompaniesShakthi p raiNessuna valutazione finora

- Income Tax Law IntroductionDocumento31 pagineIncome Tax Law Introductionsourav kumar rayNessuna valutazione finora

- Banking Law Assignment - ViswanathanDocumento6 pagineBanking Law Assignment - ViswanathanViswa NathanNessuna valutazione finora

- Relationship Between Banker and CustomerDocumento9 pagineRelationship Between Banker and CustomerLaw LawyersNessuna valutazione finora

- Indian Business LawDocumento335 pagineIndian Business Lawmanishkul-Nessuna valutazione finora

- SBI Account Opening Form Without Cut Mark 02.08.2018Documento20 pagineSBI Account Opening Form Without Cut Mark 02.08.2018Shishir Kant SinghNessuna valutazione finora

- Banking and Insurance ElementsDocumento11 pagineBanking and Insurance ElementsNisarg ShahNessuna valutazione finora

- Consumer Protection CouncilsDocumento18 pagineConsumer Protection CouncilsyuktaNessuna valutazione finora

- LC FinalDocumento42 pagineLC FinalPraveen NairNessuna valutazione finora

- Insurance Act, 1938Documento101 pagineInsurance Act, 1938dodoNessuna valutazione finora

- Currency ConvertibilityDocumento37 pagineCurrency Convertibilitylavkush_khannaNessuna valutazione finora

- Kanga & Palkhivala IT Act 10th Ed Vol I CH 4 Part IDocumento119 pagineKanga & Palkhivala IT Act 10th Ed Vol I CH 4 Part IlokeshNessuna valutazione finora

- FDI in Indian Banking SectorDocumento38 pagineFDI in Indian Banking SectorSumedhAmaneNessuna valutazione finora

- Introduction to Corporate AdministrationDocumento14 pagineIntroduction to Corporate AdministrationHosahalli Narayana Murthy PrasannaNessuna valutazione finora

- Income From Other SourcesDocumento9 pagineIncome From Other Sourcesrajsab20061093Nessuna valutazione finora

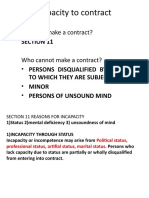

- Capacity To ContractDocumento16 pagineCapacity To Contractamrutha chiranjeeviNessuna valutazione finora

- Banking Law Final DraftDocumento13 pagineBanking Law Final DraftAkash JainNessuna valutazione finora

- Condition and WarrantyDocumento3 pagineCondition and Warrantyjerry zaidiNessuna valutazione finora

- 34 Taxation in IndiaDocumento8 pagine34 Taxation in IndiaSharma AiplNessuna valutazione finora

- Banking-Theory-Law and PracticeDocumento258 pagineBanking-Theory-Law and PracticeRahul Sharma100% (1)

- Duties of Banker Towards His CoustomerDocumento24 pagineDuties of Banker Towards His CoustomerAakashsharma0% (2)

- International BankingDocumento46 pagineInternational BankingSandesh Bhat100% (1)

- Tata Code of ConductDocumento11 pagineTata Code of ConductShabir ShafkatNessuna valutazione finora

- Bill DiscountingDocumento21 pagineBill DiscountingsrinaathmNessuna valutazione finora

- Bill DiscountingDocumento69 pagineBill DiscountingDhanesh BabarNessuna valutazione finora

- Duties and Liabilities of DirectorsDocumento12 pagineDuties and Liabilities of DirectorsSamiksha Pawar100% (1)

- Classification of Taxable Income Under Various Heads and Computation of Taxable IncomeDocumento4 pagineClassification of Taxable Income Under Various Heads and Computation of Taxable IncomeAnkit Kr MishraNessuna valutazione finora

- Baf Sem 5Documento8 pagineBaf Sem 5api-292680897Nessuna valutazione finora

- IntershipDocumento65 pagineIntershipainashaikhNessuna valutazione finora

- Role of Banking Sector in IndiaDocumento75 pagineRole of Banking Sector in IndiaOna JacintoNessuna valutazione finora

- 0102164625advance FEMA RBI Queries PDFDocumento28 pagine0102164625advance FEMA RBI Queries PDFChintz MehtaNessuna valutazione finora

- Whether Automatic Vending Machines Make OffersDocumento10 pagineWhether Automatic Vending Machines Make OffersHarshit JainNessuna valutazione finora

- Co-operative Society Guide for StudentsDocumento40 pagineCo-operative Society Guide for StudentsBhavyaNessuna valutazione finora

- SEBI (Disclosure & Investor Protection) Guideline, 2000Documento16 pagineSEBI (Disclosure & Investor Protection) Guideline, 2000Ankit Kumar (B.A. LLB 16)Nessuna valutazione finora

- Banking Ombudsman: Meaning, Functions and WorkingDocumento5 pagineBanking Ombudsman: Meaning, Functions and WorkingSapphire Sharma0% (1)

- CONtractsDocumento8 pagineCONtractsmanjeet kumarNessuna valutazione finora

- IRS Pub 2194 - Disaster Relief Tax AddendumDocumento136 pagineIRS Pub 2194 - Disaster Relief Tax AddendumdonlucekNessuna valutazione finora

- ProspectusDocumento26 pagineProspectusLogesh JanagarajNessuna valutazione finora

- Indemnity Bond ExplainedDocumento4 pagineIndemnity Bond ExplainedAksa Rasool100% (1)

- Idbi SeminarDocumento17 pagineIdbi SeminarnancyagarwalNessuna valutazione finora

- Taxation of Salaried EmployeesDocumento39 pagineTaxation of Salaried Employeessailolla30Nessuna valutazione finora

- Mercantile Law NotesDocumento21 pagineMercantile Law NotesPriyanka BarikNessuna valutazione finora

- Memorandum and Articles Are Public DocumentsDocumento1 paginaMemorandum and Articles Are Public DocumentsAsma Masood67% (3)

- Promisory Note: Unit - 2 BY Prof. Thaseen Sultana GFGC Frazer Town, BangaloreDocumento12 paginePromisory Note: Unit - 2 BY Prof. Thaseen Sultana GFGC Frazer Town, BangaloreThaseen SultanaNessuna valutazione finora

- Harshad Mehta ScamDocumento17 pagineHarshad Mehta ScamJaywanti Akshra GurbaniNessuna valutazione finora

- Memorandum of AssociationDocumento19 pagineMemorandum of AssociationVishal0% (1)

- Scenario of Foreign Banks in IndiaDocumento62 pagineScenario of Foreign Banks in IndiaYesha Khona100% (1)

- Company Law Registration and IncorporationDocumento10 pagineCompany Law Registration and IncorporationAyush BansalNessuna valutazione finora

- Banker - Customer RelationshipDocumento18 pagineBanker - Customer Relationshipjoel minaniNessuna valutazione finora

- Financial System Reforms GuideDocumento16 pagineFinancial System Reforms GuideSAUGATA KUMAR DASNessuna valutazione finora

- Rbi Impact On Indian EconomyDocumento15 pagineRbi Impact On Indian EconomyJP MusicNessuna valutazione finora

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Da EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Nessuna valutazione finora

- Going for Broke: Insolvency Tools to Support Cross-Border Asset Recovery in Corruption CasesDa EverandGoing for Broke: Insolvency Tools to Support Cross-Border Asset Recovery in Corruption CasesNessuna valutazione finora

- 14-05-12 R MailDocumento2 pagine14-05-12 R MailUmer ChaudharyNessuna valutazione finora

- Delivery FormatDocumento1 paginaDelivery FormatUmer ChaudharyNessuna valutazione finora

- Table # 4.2-ADocumento1 paginaTable # 4.2-AUmer ChaudharyNessuna valutazione finora

- Cash Flow Statement For BahriaDocumento14 pagineCash Flow Statement For BahriaUmer ChaudharyNessuna valutazione finora

- Delivery FormatDocumento1 paginaDelivery FormatUmer ChaudharyNessuna valutazione finora

- Trend Analysis: Sales Cost of Goods Sold Gross Profit Distribution Cost Admin Expenses Other Operating ExpensesDocumento4 pagineTrend Analysis: Sales Cost of Goods Sold Gross Profit Distribution Cost Admin Expenses Other Operating ExpensesUmer ChaudharyNessuna valutazione finora

- Nishat Mills Limited..Rati Analysis.Documento7 pagineNishat Mills Limited..Rati Analysis.Umer ChaudharyNessuna valutazione finora

- Trend Analysis: Sales Cost of Goods Sold Gross Profit Distribution Cost Admin Expenses Other Operating ExpensesDocumento4 pagineTrend Analysis: Sales Cost of Goods Sold Gross Profit Distribution Cost Admin Expenses Other Operating ExpensesUmer ChaudharyNessuna valutazione finora

- Chapter 20. Capital Structure DecisionDocumento14 pagineChapter 20. Capital Structure Decisionmy backup1Nessuna valutazione finora

- CA Foundation Accounts Theory Question Bank Dec 2021 Attempt NotesDocumento142 pagineCA Foundation Accounts Theory Question Bank Dec 2021 Attempt NotesRakesh Roshan100% (1)

- Personal Balance Sheet 03Documento5 paginePersonal Balance Sheet 03Hanna mariel Del MundoNessuna valutazione finora

- Tax Invoice for 1oz Gold Coin 2021 Kangaroo PurchaseDocumento1 paginaTax Invoice for 1oz Gold Coin 2021 Kangaroo PurchaseGoran KovacevicNessuna valutazione finora

- Table Key: How To Use This Document?Documento28 pagineTable Key: How To Use This Document?subsmagicNessuna valutazione finora

- Credit Cards SO API September 2015Documento367 pagineCredit Cards SO API September 2015Shailesh ShuklaNessuna valutazione finora

- IAS 30 Disclosures in The Financial Statements of Banks and Similar Financial InstitutionsDocumento8 pagineIAS 30 Disclosures in The Financial Statements of Banks and Similar Financial InstitutionsZienab Mosabbeh100% (1)

- Quiz Laguitao FinancialMarket BSA501Documento3 pagineQuiz Laguitao FinancialMarket BSA501Catherine LaguitaoNessuna valutazione finora

- Intermidiate FA I ChapterDocumento12 pagineIntermidiate FA I Chapteryiberta69Nessuna valutazione finora

- Esp BussinessDocumento8 pagineEsp BussinessDewi RoosnitasariNessuna valutazione finora

- Insurance Law in India Question and AnswerDocumento15 pagineInsurance Law in India Question and AnswerMaitrayee NandyNessuna valutazione finora

- Guidance Note On Bank Audit 2023 16.03.2023 PDFDocumento812 pagineGuidance Note On Bank Audit 2023 16.03.2023 PDFSrini100% (1)

- Output DocumentDocumento1.474 pagineOutput DocumentKuladeep Naidu PatibandlaNessuna valutazione finora

- Bill - 2014 01 01Documento4 pagineBill - 2014 01 01Nor Hidayah0% (1)

- Margarita S. Monilla - Resume PDFDocumento2 pagineMargarita S. Monilla - Resume PDFFBG- KinNessuna valutazione finora

- 431 FinalDocumento6 pagine431 FinalfNessuna valutazione finora

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento48 pagineDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceRohit raagNessuna valutazione finora

- Blank Cash Flow Template ExcelDocumento5 pagineBlank Cash Flow Template ExcelPro ResourcesNessuna valutazione finora

- Oci TheoriesDocumento5 pagineOci TheoriesArriety KimNessuna valutazione finora

- A STUDY ON ReviewDocumento28 pagineA STUDY ON Reviewaurorashiva1Nessuna valutazione finora

- Financial Accounting and Reporting (Chapter 14-16)Documento51 pagineFinancial Accounting and Reporting (Chapter 14-16)Jenny Ygrubay100% (1)

- Historical Income Statement and Balance Sheets For Vitex Corp. Income Statement ($ Million)Documento4 pagineHistorical Income Statement and Balance Sheets For Vitex Corp. Income Statement ($ Million)ShilpaNessuna valutazione finora

- CHP - 9 - Industrial Securities MarketDocumento10 pagineCHP - 9 - Industrial Securities MarketNandini JaganNessuna valutazione finora

- Resumos - APFDocumento23 pagineResumos - APFMariana GomesNessuna valutazione finora

- Colin - BookDocumento15 pagineColin - BookrizwanNessuna valutazione finora

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento10 pagineStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceYeshwanth SunkaraNessuna valutazione finora

- Oct+31,+2022 2Documento7 pagineOct+31,+2022 2nyNessuna valutazione finora