Potrebbero piacerti anche

- Wholesale Banking A Complete Guide - 2021 EditionDa EverandWholesale Banking A Complete Guide - 2021 EditionNessuna valutazione finora

- Landlord Tax Planning StrategiesDa EverandLandlord Tax Planning StrategiesNessuna valutazione finora

- Erma AND MICR PowerpointDocumento13 pagineErma AND MICR PowerpointJonathan Realis Capilo100% (1)

- Q. 8 Governments BondsDocumento2 pagineQ. 8 Governments BondsMAHENDRA SHIVAJI DHENAKNessuna valutazione finora

- Bank Management CHAP - 01 - 6edDocumento51 pagineBank Management CHAP - 01 - 6edNikhil ChitaliaNessuna valutazione finora

- Banking Operations (MAIN TOPICS)Documento32 pagineBanking Operations (MAIN TOPICS)Saqib ShahzadNessuna valutazione finora

- Capital Raising Regulation D SEC Vladimir IvanovDocumento11 pagineCapital Raising Regulation D SEC Vladimir IvanovCrowdfundInsiderNessuna valutazione finora

- Underwriting of SecuritiesDocumento20 pagineUnderwriting of Securitiesrahul0105100% (1)

- Standard Chartered Wealth Management PackDocumento35 pagineStandard Chartered Wealth Management PackAnura BirdNessuna valutazione finora

- Credit Management NotesDocumento27 pagineCredit Management NotesHannan Ahmad0% (1)

- Definition of 'Credit': Joana Rey P. Palabyab Credit and Collection BSBM - Fm3A Ms. Luisita MarzanDocumento3 pagineDefinition of 'Credit': Joana Rey P. Palabyab Credit and Collection BSBM - Fm3A Ms. Luisita MarzanJoana Rey PalabyabNessuna valutazione finora

- Principles of BankingDocumento25 paginePrinciples of Bankingekta singhNessuna valutazione finora

- (John Tuld) : Professional ExperienceDocumento2 pagine(John Tuld) : Professional Experienceدولت ابد مدت Devlet-i Aliyye-i OsmâniyyeNessuna valutazione finora

- Chapter 1 - Investments: Background and IssuesDocumento61 pagineChapter 1 - Investments: Background and IssuesMadhan RajNessuna valutazione finora

- Factoring in Finance ArrangementsDocumento9 pagineFactoring in Finance Arrangementsduncanmac200777Nessuna valutazione finora

- The Supply of MoneyDocumento6 pagineThe Supply of MoneyRobertKimtaiNessuna valutazione finora

- Monthly Summary of Mortgage Activities For The Period Ending April 2019Documento17 pagineMonthly Summary of Mortgage Activities For The Period Ending April 2019Nico Gillo ObejeroNessuna valutazione finora

- Pipeline Hedging: The New Imperative For The Independent Mortgage Banker.Documento8 paginePipeline Hedging: The New Imperative For The Independent Mortgage Banker.Andrew ArmstrongNessuna valutazione finora

- Banker and CustomerDocumento23 pagineBanker and CustomerAnkan Pattanayak100% (1)

- General Banking TermsDocumento17 pagineGeneral Banking TermsVineeth JoseNessuna valutazione finora

- Starting A Small Scale BusinessDocumento26 pagineStarting A Small Scale BusinessMariam Oluwatoyin CampbellNessuna valutazione finora

- Aliko Dangote: 5 Things You Can Learn From Africa's Richest ManDocumento4 pagineAliko Dangote: 5 Things You Can Learn From Africa's Richest ManikchikovaNessuna valutazione finora

- Bonds: Types, Trading & SettlementDocumento52 pagineBonds: Types, Trading & SettlementraviNessuna valutazione finora

- Mortgage Loan DefinitionDocumento65 pagineMortgage Loan DefinitionAnonymous iyQmvDnHnCNessuna valutazione finora

- 10 FREE FINRA Series 6 Top Off Exam Practice Questions in PDF FormatDocumento3 pagine10 FREE FINRA Series 6 Top Off Exam Practice Questions in PDF FormatEmmanuelDasiNessuna valutazione finora

- Door Step BankingDocumento30 pagineDoor Step Bankingvahid86% (7)

- Cash & Debt FreeDocumento30 pagineCash & Debt FreeReza HaryoNessuna valutazione finora

- Ch21 (Term Loan & Lease)Documento37 pagineCh21 (Term Loan & Lease)মেহেদি তসলিমNessuna valutazione finora

- WCM - Unit 2 Cash ManagementDocumento51 pagineWCM - Unit 2 Cash ManagementkartikNessuna valutazione finora

- Credit Policy PDFDocumento4 pagineCredit Policy PDFMichaelsam100% (1)

- HBS Note On CommercialBankingDocumento16 pagineHBS Note On CommercialBankingJatin SankarNessuna valutazione finora

- Is Shadow Banking Really BankingDocumento16 pagineIs Shadow Banking Really BankingBlackSeaTimesNessuna valutazione finora

- Fixed Income Securities: IntroductionDocumento33 pagineFixed Income Securities: IntroductionYogaPratamaDosen100% (1)

- Investments NotesDocumento3 pagineInvestments Notesapi-288392911Nessuna valutazione finora

- Chapter 11 The Money MarketsDocumento8 pagineChapter 11 The Money Marketslasha KachkachishviliNessuna valutazione finora

- Financial Statment AnalysisDocumento42 pagineFinancial Statment AnalysisfehNessuna valutazione finora

- CRM in Private BanksDocumento27 pagineCRM in Private BanksManuKingKaushik67% (3)

- Lehman On The Brink of BankruptcyDocumento19 pagineLehman On The Brink of Bankruptcyed_nycNessuna valutazione finora

- Rebuilding Operating Model Credit Card CompaniesDocumento4 pagineRebuilding Operating Model Credit Card CompaniesapluNessuna valutazione finora

- Lending Club Retirement GuideDocumento8 pagineLending Club Retirement Guidecera66Nessuna valutazione finora

- Home LoansDocumento56 pagineHome LoansabhiNessuna valutazione finora

- SBA Inspector General Report: Small Business Administration's Implementation of The Paycheck Protection Program RequirementsDocumento40 pagineSBA Inspector General Report: Small Business Administration's Implementation of The Paycheck Protection Program RequirementsMatthew KishNessuna valutazione finora

- Balance Sheet Management - BFMDocumento4 pagineBalance Sheet Management - BFMakvgauravNessuna valutazione finora

- WMDocumento151 pagineWMKomal Bagrodia100% (1)

- Blueprint of Banking SectorDocumento33 pagineBlueprint of Banking SectormayankNessuna valutazione finora

- COVID-19 Federal Assistance Summary of Benefits For Churches and IndividualsDocumento4 pagineCOVID-19 Federal Assistance Summary of Benefits For Churches and IndividualsKirk PetersenNessuna valutazione finora

- 1 - Startup Funding LandscapeDocumento13 pagine1 - Startup Funding LandscapeAlexNessuna valutazione finora

- Personal Finance NotesDocumento5 paginePersonal Finance Notesapi-311953609100% (1)

- Handbook 5.12 Federal Tax Liens HandbookDocumento41 pagineHandbook 5.12 Federal Tax Liens HandbookPaulStaplesNessuna valutazione finora

- Leveraged Buyout (LBO) Private EquityDocumento4 pagineLeveraged Buyout (LBO) Private EquityAmit Kumar RathNessuna valutazione finora

- Types of Financial Instruments of Money MarketDocumento2 pagineTypes of Financial Instruments of Money MarketMian Abdul HaseebNessuna valutazione finora

- Credit Risk Management of United Commercial BDocumento45 pagineCredit Risk Management of United Commercial Bএকজন নিশাচরNessuna valutazione finora

- Private BankingDocumento3 paginePrivate BankingBharat KhiaraNessuna valutazione finora

- Placement Memorandum of CPR Investors, LLC - Final Investor Package (Nov. 27, 2019)Documento225 paginePlacement Memorandum of CPR Investors, LLC - Final Investor Package (Nov. 27, 2019)safe tradeNessuna valutazione finora

- Loan Cheat Sheet by Jocelyn PredovichDocumento1 paginaLoan Cheat Sheet by Jocelyn PredovichJocelyn Javernick PredovichNessuna valutazione finora

- Loans and AdvancesDocumento18 pagineLoans and AdvancesAnupam RoyNessuna valutazione finora

- Buyer CreditDocumento11 pagineBuyer Creditkalik goyalNessuna valutazione finora

- Factors Affecting Capitalization Rate of US Real EstateDocumento36 pagineFactors Affecting Capitalization Rate of US Real Estatevharish88Nessuna valutazione finora

- Presentation On ED Family BusinessDocumento22 paginePresentation On ED Family BusinessGolam Mostofa100% (1)

- Business Tax Credit For Research And Development A Complete Guide - 2020 EditionDa EverandBusiness Tax Credit For Research And Development A Complete Guide - 2020 EditionNessuna valutazione finora

- FCCB 1Documento6 pagineFCCB 1krishr25Nessuna valutazione finora

- Bo Dincer New York Top Trader NYCDocumento1 paginaBo Dincer New York Top Trader NYCBONDTRADER100% (1)

- Cat Bonds DemystifiedDocumento12 pagineCat Bonds DemystifiedJames Shadowen-KurzNessuna valutazione finora

- Top-Ten Rules For Successful Trading - A Pro's Private Collection With George Kleinman PDFDocumento60 pagineTop-Ten Rules For Successful Trading - A Pro's Private Collection With George Kleinman PDFSameer ShindeNessuna valutazione finora

- Barb William and Steven LauDocumento6 pagineBarb William and Steven Lauzaidirock68Nessuna valutazione finora

- Cemeco Vs National LifeDocumento3 pagineCemeco Vs National LifeIanNessuna valutazione finora

- Retirement Option Form: Declaration and Specimen Signature of Accont Holder (S)Documento1 paginaRetirement Option Form: Declaration and Specimen Signature of Accont Holder (S)Salman ArshadNessuna valutazione finora

- Procter and Gamble: Cost of CapitalDocumento64 pagineProcter and Gamble: Cost of CapitalShriniwas NeheteNessuna valutazione finora

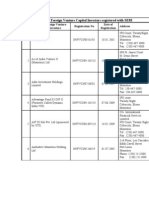

- A-List of Foreign Venture Capital Investors Registered With SEBIDocumento24 pagineA-List of Foreign Venture Capital Investors Registered With SEBIVipul ParekhNessuna valutazione finora

- The Role of Managerial Finance - PearsonDocumento60 pagineThe Role of Managerial Finance - PearsonHerdi SularkoNessuna valutazione finora

- Double Bollinger Band MACD Stochastic Crossover Forex StrategyDocumento7 pagineDouble Bollinger Band MACD Stochastic Crossover Forex Strategyanand_studyNessuna valutazione finora

- Indiabulls and Indian Stock MarketDocumento86 pagineIndiabulls and Indian Stock Marketaayush batraNessuna valutazione finora

- Contract Drafting - Assignment 2Documento2 pagineContract Drafting - Assignment 2verna_goh_shileiNessuna valutazione finora

- BizSim Presentation Template 2016Documento8 pagineBizSim Presentation Template 2016Benzamin DangNessuna valutazione finora

- Analysis Size PremiumDocumento4 pagineAnalysis Size PremiumAntonio Moreno SantelizNessuna valutazione finora

- Term Paper of MGT 517Documento13 pagineTerm Paper of MGT 517VIPULGARG47Nessuna valutazione finora

- Fiduciary Duties and BrokersDocumento21 pagineFiduciary Duties and BrokersmeanhappydwarfNessuna valutazione finora

- Time Tested Classic Trading Rules For The Modern Trader To FollowDocumento19 pagineTime Tested Classic Trading Rules For The Modern Trader To FollowArt James100% (1)

- Level I Mock Exam Morning Versionb Questions 2014 PDFDocumento31 pagineLevel I Mock Exam Morning Versionb Questions 2014 PDFkren24Nessuna valutazione finora

- CmaDocumento22 pagineCmaAhmed Mostafa ElmowafyNessuna valutazione finora

- Market MasteryDocumento79 pagineMarket MasteryFrancis Ejike100% (3)

- Capital Budgeting Practices in Developing CountriesDocumento19 pagineCapital Budgeting Practices in Developing CountriescomaixanhNessuna valutazione finora

- Financial Due DiligenceDocumento6 pagineFinancial Due DiligencePatrick CheungNessuna valutazione finora

- Warren Buffett 1997 BRK Annual Report To ShareholdersDocumento20 pagineWarren Buffett 1997 BRK Annual Report To ShareholdersBrian McMorrisNessuna valutazione finora

- StudentDocumento33 pagineStudentKevin Che100% (2)

- Dabur Case Study: Marketing ManagementDocumento24 pagineDabur Case Study: Marketing ManagementabhishekniiftNessuna valutazione finora

- ch01 The Role of Financial ManagementDocumento25 paginech01 The Role of Financial ManagementBagusranu Wahyudi Putra100% (1)

- Mckinsey Appraisal - AppraisalDocumento8 pagineMckinsey Appraisal - Appraisalalex.nogueira396Nessuna valutazione finora

- Home Office IntegDocumento9 pagineHome Office IntegReshielyn Vee Entrampas LopezNessuna valutazione finora

- FI 515 Week 1 QuizDocumento4 pagineFI 515 Week 1 QuizBella DavidovaNessuna valutazione finora