Potrebbero piacerti anche

- Essentials of An Insurance ContractDocumento7 pagineEssentials of An Insurance ContractSameer JoshiNessuna valutazione finora

- LIC Composition POWER FUNCTIONDocumento5 pagineLIC Composition POWER FUNCTIONishwar50% (2)

- Paying BankerDocumento18 paginePaying Bankersagarg94gmailcom90% (10)

- Utmost Good FaithDocumento43 pagineUtmost Good FaithHarsh SharmaNessuna valutazione finora

- General Provisions About BaggageDocumento10 pagineGeneral Provisions About BaggageSunil VishwakarmaNessuna valutazione finora

- Importance of Life InsuranceDocumento18 pagineImportance of Life InsuranceAsim KunduNessuna valutazione finora

- Strike Lock OutDocumento23 pagineStrike Lock OutMishika PanditaNessuna valutazione finora

- Raghavan Committee - Competition LawDocumento3 pagineRaghavan Committee - Competition Lawsaakshi singhNessuna valutazione finora

- Key features of the IRDA Act 1999 including foreign investment limitsDocumento2 pagineKey features of the IRDA Act 1999 including foreign investment limitsRHEANessuna valutazione finora

- Competition Law - Sample QuestionsDocumento1 paginaCompetition Law - Sample QuestionsRouñåk GuptäNessuna valutazione finora

- IRDADocumento9 pagineIRDAprerna1891Nessuna valutazione finora

- Company Law-Kinds of MeetingDocumento8 pagineCompany Law-Kinds of MeetingIrfan Baari100% (1)

- Chapter - 2 Concept, Nature and Scope of Insurance Concept of InsuranceDocumento13 pagineChapter - 2 Concept, Nature and Scope of Insurance Concept of InsuranceAdv Vaishali GuptaNessuna valutazione finora

- Is Company A CitizenDocumento11 pagineIs Company A CitizenRitika Ritz0% (1)

- Insurance Law - Theft and BurglaryDocumento13 pagineInsurance Law - Theft and BurglaryDarshil Parikh100% (1)

- Limitation in Taking CognizanceDocumento10 pagineLimitation in Taking CognizanceAbhishek Tiwari100% (1)

- Employers Liability For CompensationDocumento9 pagineEmployers Liability For CompensationManoj GandhiNessuna valutazione finora

- What Is Public Liability Insurance??Documento20 pagineWhat Is Public Liability Insurance??Neetish Kumar Handa91% (32)

- Banking Law: Notes OnDocumento134 pagineBanking Law: Notes OnLittz MandumpalaNessuna valutazione finora

- Securities Contracts Regulation Act 1956Documento32 pagineSecurities Contracts Regulation Act 1956prasadzinjurdeNessuna valutazione finora

- Difference Between Companies Act 2013 Vs Companies Act 1956Documento2 pagineDifference Between Companies Act 2013 Vs Companies Act 1956Vikas KumarNessuna valutazione finora

- 1.definition of A Company and Its CharecteriosticsDocumento11 pagine1.definition of A Company and Its Charecteriosticssunitmishra2007Nessuna valutazione finora

- Settlement of Claim and Payment of MoneyDocumento9 pagineSettlement of Claim and Payment of MoneyVarnika TayaNessuna valutazione finora

- Nationalisation of Insurance BusinessDocumento12 pagineNationalisation of Insurance BusinessSanjay Ram Diwakar50% (2)

- Regulation of Certifying AuthoritiesDocumento19 pagineRegulation of Certifying Authoritiesakkig1100% (6)

- Contract of BailmentDocumento12 pagineContract of BailmentAyush GaurNessuna valutazione finora

- Unit IV Fire InsuranceDocumento7 pagineUnit IV Fire InsuranceEswaran LakshmananNessuna valutazione finora

- Evolution of Insurance in IndiaDocumento6 pagineEvolution of Insurance in IndiaDeepak Kumar Singh100% (1)

- Cii CodeDocumento6 pagineCii Codetanmayjoshi969315100% (1)

- Agreements of Persons Disqualified by LawDocumento23 pagineAgreements of Persons Disqualified by LawAvnet KaurNessuna valutazione finora

- Authorities Under IT ActDocumento5 pagineAuthorities Under IT ActJug-Mug CaféNessuna valutazione finora

- Banking Ombudsman Scheme in India: A Brief AnalysisDocumento18 pagineBanking Ombudsman Scheme in India: A Brief AnalysisVicky DNessuna valutazione finora

- Model Law on E-Commerce Guides Global Digital TradeDocumento5 pagineModel Law on E-Commerce Guides Global Digital TradeJapneet KaurNessuna valutazione finora

- 04 Powers of OfficersDocumento3 pagine04 Powers of OfficersAnantHimanshuEkka100% (1)

- Insurance Regulatory Authority Act ExplainedDocumento6 pagineInsurance Regulatory Authority Act ExplainedTitus ClementNessuna valutazione finora

- Borrowing Power of Company PDFDocumento12 pagineBorrowing Power of Company PDFmanishaamba7547Nessuna valutazione finora

- Salient Features of The Insurance Act, 1938Documento3 pagineSalient Features of The Insurance Act, 1938Sriniwas ThakurNessuna valutazione finora

- Unit 2 - Appeal and RevisionDocumento12 pagineUnit 2 - Appeal and RevisionRakhi Dhamija50% (2)

- No Better Title ExceptionDocumento17 pagineNo Better Title ExceptionRashiGosain67% (3)

- Difference Between Interpretation and ConstructionDocumento15 pagineDifference Between Interpretation and Constructionsonali supriyaNessuna valutazione finora

- Motor Insurance in India FDDocumento16 pagineMotor Insurance in India FDSushil JindalNessuna valutazione finora

- THE CHARGE (Sec 211 To Sec 224) : ShardaDocumento20 pagineTHE CHARGE (Sec 211 To Sec 224) : ShardaRohit GargNessuna valutazione finora

- Balram Prasad Vs Kunal SahaDocumento3 pagineBalram Prasad Vs Kunal SahaATHENAS100% (2)

- Competition Commission of India (CCI)Documento27 pagineCompetition Commission of India (CCI)Supriya Pawar100% (1)

- Payment of BonusDocumento46 paginePayment of BonusAnkur AroraNessuna valutazione finora

- IRDADocumento21 pagineIRDAknicknic100% (1)

- IRDA by The DudesDocumento13 pagineIRDA by The DudesAbhimanyu MaheshwariNessuna valutazione finora

- Income Exempt From TaxDocumento20 pagineIncome Exempt From TaxSaad AliNessuna valutazione finora

- Alteration of RiskDocumento3 pagineAlteration of RiskJayjeet Bhattacharjee100% (1)

- Implied authority of partners and third partiesDocumento2 pagineImplied authority of partners and third partiesJay Patel100% (1)

- Law Quasi Contracts FinalDocumento11 pagineLaw Quasi Contracts FinalHarsh YadavNessuna valutazione finora

- Difference Between Sale Agreement and Agreement to SellDocumento2 pagineDifference Between Sale Agreement and Agreement to SellHarneet KaurNessuna valutazione finora

- Understanding Income from House PropertyDocumento19 pagineUnderstanding Income from House PropertyAmrit Tejani100% (1)

- Sarfaesi ActDocumento8 pagineSarfaesi Actvrkesavan100% (2)

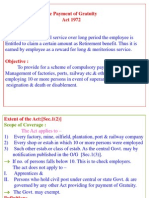

- The Payment of Gratuity Act 1972Documento8 pagineThe Payment of Gratuity Act 1972Binny SinghNessuna valutazione finora

- Life Insurance:: Concept, Nature and ScopeDocumento38 pagineLife Insurance:: Concept, Nature and ScopeAkshay BhasinNessuna valutazione finora

- Insurance Reviewer1555555Documento29 pagineInsurance Reviewer1555555Rudy G. Alvarez Jr.Nessuna valutazione finora

- Lecture On Insurance LawDocumento8 pagineLecture On Insurance LawGianaNessuna valutazione finora

- 9252 - Insurance Law - R.A. No. 2427Documento4 pagine9252 - Insurance Law - R.A. No. 2427dahpne saquianNessuna valutazione finora

- insurance-law_compressDocumento4 pagineinsurance-law_compressrieann leonNessuna valutazione finora

- Absolute Grounds For Refusal of Trade Mark 2 (Word)Documento11 pagineAbsolute Grounds For Refusal of Trade Mark 2 (Word)Harsh SharmaNessuna valutazione finora

- Conventions File IprDocumento26 pagineConventions File IprHarsh SharmaNessuna valutazione finora

- Paper II - 04 - Contemporary Legal DevelopmentsDocumento17 paginePaper II - 04 - Contemporary Legal DevelopmentsHarsh SharmaNessuna valutazione finora

- Economic Significance of Competition LawDocumento38 pagineEconomic Significance of Competition LawHarsh SharmaNessuna valutazione finora

- Unit - II Intellectual Property Rights in CyberspaceDocumento39 pagineUnit - II Intellectual Property Rights in CyberspaceHarsh SharmaNessuna valutazione finora

- Unit - III Information Technology Act, 2000 Cyber Law in IndiaDocumento147 pagineUnit - III Information Technology Act, 2000 Cyber Law in IndiaHarsh SharmaNessuna valutazione finora

- Absolute and Relative Grounds For Refusal of RegistrationDocumento14 pagineAbsolute and Relative Grounds For Refusal of RegistrationHarsh SharmaNessuna valutazione finora

- Unit - I Intro. To Cyber Laws and Cyber Space - AllDocumento110 pagineUnit - I Intro. To Cyber Laws and Cyber Space - AllHarsh SharmaNessuna valutazione finora

- Competition Act, 2002Documento80 pagineCompetition Act, 2002Harsh SharmaNessuna valutazione finora

- Competition Commission of IndiaDocumento42 pagineCompetition Commission of IndiaHarsh SharmaNessuna valutazione finora

- Competition Code and WTO Meaning of Certain TermsDocumento53 pagineCompetition Code and WTO Meaning of Certain TermsHarsh SharmaNessuna valutazione finora

- Competition and IPRDocumento52 pagineCompetition and IPRHarsh SharmaNessuna valutazione finora

- Competition Law - Lecture 1Documento8 pagineCompetition Law - Lecture 1Harsh SharmaNessuna valutazione finora

- The ICANN Uniform Domain Name Dispute Resolution PolicyDocumento12 pagineThe ICANN Uniform Domain Name Dispute Resolution PolicyHarsh SharmaNessuna valutazione finora

- Kendriya Vidyalaya CRPF, Gandhinagar Firm Registration Form For 2018-19 Registration Firms/agencies For Supply/ServiceDocumento1 paginaKendriya Vidyalaya CRPF, Gandhinagar Firm Registration Form For 2018-19 Registration Firms/agencies For Supply/ServiceHarsh SharmaNessuna valutazione finora

- Chapter 2 PDFDocumento12 pagineChapter 2 PDFHarsh SharmaNessuna valutazione finora

- Essentials of Valid Insurance ContractDocumento8 pagineEssentials of Valid Insurance ContractHarsh SharmaNessuna valutazione finora

- Health Law-Course Module-2019-20Documento5 pagineHealth Law-Course Module-2019-20Harsh SharmaNessuna valutazione finora

- Chapter 5 PDFDocumento7 pagineChapter 5 PDFHarsh SharmaNessuna valutazione finora

- Chapter 6Documento6 pagineChapter 6Harsh SharmaNessuna valutazione finora

- Assignment 64-65Documento15 pagineAssignment 64-65Harsh SharmaNessuna valutazione finora

- Chapter 8Documento6 pagineChapter 8Harsh SharmaNessuna valutazione finora

- UNIT4, Point DDocumento10 pagineUNIT4, Point DHarsh SharmaNessuna valutazione finora

- Chapter 2 PDFDocumento12 pagineChapter 2 PDFHarsh SharmaNessuna valutazione finora

- Chapter 7 PDFDocumento8 pagineChapter 7 PDFHarsh SharmaNessuna valutazione finora

- UNIT4, Point GDocumento13 pagineUNIT4, Point GHarsh SharmaNessuna valutazione finora

- Disability Certificates in India - A Challenge To Health PrivacyDocumento6 pagineDisability Certificates in India - A Challenge To Health PrivacyHarsh SharmaNessuna valutazione finora

- PATIENT RIGHTS TITLEDocumento41 paginePATIENT RIGHTS TITLEHarsh Sharma100% (1)

- UNIT4, Point HDocumento10 pagineUNIT4, Point HHarsh SharmaNessuna valutazione finora

- Gujarat Law Society GLS Law College, Ahmedabad Integrated Five-Year B.A. LL.B. ProgrammeDocumento4 pagineGujarat Law Society GLS Law College, Ahmedabad Integrated Five-Year B.A. LL.B. ProgrammeHarsh SharmaNessuna valutazione finora

- NMTDocumento174 pagineNMTsfirleyNessuna valutazione finora

- Adoption Registration Form PDFDocumento2 pagineAdoption Registration Form PDFhemant mehta100% (2)

- Deletion of Records From National Police Systems (Guidance) v2.0Documento49 pagineDeletion of Records From National Police Systems (Guidance) v2.0bouje72Nessuna valutazione finora

- DISBARRED ATTORNEYDocumento9 pagineDISBARRED ATTORNEYFrances MarieNessuna valutazione finora

- Harboring Trial PDF, Bonnie and Clyde.Documento71 pagineHarboring Trial PDF, Bonnie and Clyde.Charles FlynnNessuna valutazione finora

- 6300 & SGB InformationDocumento6 pagine6300 & SGB InformationPio Rodolfo0% (1)

- Sample ComplaintDocumento6 pagineSample ComplaintRoberto Testa73% (11)

- Kmu Vs ErmitaDocumento1 paginaKmu Vs ErmitaClifford TubanaNessuna valutazione finora

- Mat V PPDocumento5 pagineMat V PPMohamad MursalinNessuna valutazione finora

- APSPDCL/APEPDCL Grievance MechanismsDocumento2 pagineAPSPDCL/APEPDCL Grievance MechanismsSatyanarayanaChandakaNessuna valutazione finora

- Pomperada v. Jochico y Pama, B.M. No. 68 (Resolution), (November 21, 1984), 218 PHIL 289-297Documento15 paginePomperada v. Jochico y Pama, B.M. No. 68 (Resolution), (November 21, 1984), 218 PHIL 289-297Kristina B DiamanteNessuna valutazione finora

- Jesse D. LANGDON and Eureka Vacuum Breaker Corporation, Appellants, v. SALTSER & WEINSIER, INC., Appellee, Sloan Valve Company, Intervener-AppelleeDocumento4 pagineJesse D. LANGDON and Eureka Vacuum Breaker Corporation, Appellants, v. SALTSER & WEINSIER, INC., Appellee, Sloan Valve Company, Intervener-AppelleeScribd Government DocsNessuna valutazione finora

- 8prosecution - RevisedDocumento7 pagine8prosecution - Reviseddwight yuNessuna valutazione finora

- Ortigas Co. Vs Judge HerreraDocumento6 pagineOrtigas Co. Vs Judge HerreraadeleNessuna valutazione finora

- Bus-Org Cases-31 To 40Documento7 pagineBus-Org Cases-31 To 40Dashy CatsNessuna valutazione finora

- Mines Board Erred in Invalidating Mining AgreementDocumento7 pagineMines Board Erred in Invalidating Mining AgreementQuennie Mae ZalavarriaNessuna valutazione finora

- Land Acquisition Act 1984Documento25 pagineLand Acquisition Act 1984vipvikramNessuna valutazione finora

- Persons - 45 Katipunan V TenorioDocumento6 paginePersons - 45 Katipunan V TenorioYu Babylan100% (1)

- IACP PerpectivesDocumento2 pagineIACP PerpectivesdaggerpressNessuna valutazione finora

- 54 Soriano Vs Laguardia DigestDocumento12 pagine54 Soriano Vs Laguardia DigestKirby Jaguio LegaspiNessuna valutazione finora

- Court of Appeals Decision on Homicide Case AffirmedDocumento11 pagineCourt of Appeals Decision on Homicide Case AffirmedCel C. CaintaNessuna valutazione finora

- Public International Law GNDocumento62 paginePublic International Law GNMaria Athena Borja83% (6)

- Petitioner Vs Vs Respondent: Third DivisionDocumento14 paginePetitioner Vs Vs Respondent: Third DivisionEduard RiparipNessuna valutazione finora

- PRA City of Oakland 5-22-15 PDFDocumento4 paginePRA City of Oakland 5-22-15 PDFRecordTrac - City of OaklandNessuna valutazione finora

- Faculty of Law Report on Contempt of CourtDocumento64 pagineFaculty of Law Report on Contempt of CourtIzaan RizviNessuna valutazione finora

- Ja Anne GazaDocumento8 pagineJa Anne GazaRhows BuergoNessuna valutazione finora

- People vs. AlondeDocumento1 paginaPeople vs. AlondeRobNessuna valutazione finora

- Case Digest 2Documento3 pagineCase Digest 2JocelynyemvelosoNessuna valutazione finora

- Acknowledgement & JuratDocumento1 paginaAcknowledgement & Juratvdal100% (4)

- Contracts 1Documento23 pagineContracts 1Mani RajNessuna valutazione finora