Potrebbero piacerti anche

- Options As A Strategic Investment 4th Edition Study Guide Lawrence G McmillanDocumento2 pagineOptions As A Strategic Investment 4th Edition Study Guide Lawrence G McmillanTemple0% (2)

- Prerev FOREX 2019Documento8 paginePrerev FOREX 2019RojParcon50% (4)

- Airbnb IPODocumento64 pagineAirbnb IPOVianna NgNessuna valutazione finora

- Quiz: FC - ENG - L6-SET 2: Question ResultsDocumento4 pagineQuiz: FC - ENG - L6-SET 2: Question ResultsMingNessuna valutazione finora

- 2012 IOMA Derivatives Market Survey PDFDocumento61 pagine2012 IOMA Derivatives Market Survey PDFMiguel S OrdoñezNessuna valutazione finora

- Bac 309Documento63 pagineBac 309WINFRED KYALONessuna valutazione finora

- Intro To DerivativesDocumento25 pagineIntro To DerivativesrossNessuna valutazione finora

- Ifm Cia 1Documento9 pagineIfm Cia 1Ari HaranNessuna valutazione finora

- Csmo Project ReportDocumento14 pagineCsmo Project ReportAnirudh BhardwajNessuna valutazione finora

- Investments MergedDocumento121 pagineInvestments MergedRavi JayanthNessuna valutazione finora

- Study On Financial Position and Cash Management of Malco LTDDocumento59 pagineStudy On Financial Position and Cash Management of Malco LTDSyed FarhanNessuna valutazione finora

- Module 1 FDDDocumento44 pagineModule 1 FDDLolsNessuna valutazione finora

- Iii FdiDocumento18 pagineIii FdiShivika kaushikNessuna valutazione finora

- Session 1 - Securities Market and Trading MechanismDocumento17 pagineSession 1 - Securities Market and Trading MechanismRavi JayanthNessuna valutazione finora

- The Performance of Cooperative Banking in India.: EconomicsDocumento3 pagineThe Performance of Cooperative Banking in India.: EconomicsmovinNessuna valutazione finora

- MTM ProblemDocumento15 pagineMTM Problemmohammed zaidNessuna valutazione finora

- Analysis of ITC Stocks Against BSEDocumento13 pagineAnalysis of ITC Stocks Against BSEAnupam GautamNessuna valutazione finora

- Role of FII in INDIAN Capital Market: Presented By: Sanketh Shetty HarishDocumento35 pagineRole of FII in INDIAN Capital Market: Presented By: Sanketh Shetty HarishHarish ShettyNessuna valutazione finora

- Studying The Leading Methodology of Customs Audit Based On The Experience of Developed Western Countries and Also, Possibilities of Their Implementation in UzbekistanDocumento11 pagineStudying The Leading Methodology of Customs Audit Based On The Experience of Developed Western Countries and Also, Possibilities of Their Implementation in Uzbekistanarief yusufNessuna valutazione finora

- PROBLEMS ch06DdDocumento158 paginePROBLEMS ch06DdThoiqNessuna valutazione finora

- Article 5 'Under - Utilisation of Foreign Aid in India'Documento17 pagineArticle 5 'Under - Utilisation of Foreign Aid in India'ksphullNessuna valutazione finora

- Introduction To Nepali Stock Market Final FinalDocumento75 pagineIntroduction To Nepali Stock Market Final FinalAadarsh AkshyataNessuna valutazione finora

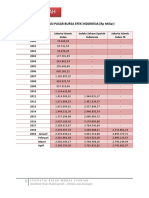

- Saham Syariah: Kapitalisasi Pasar Bursa Efek Indonesia (RP Miliar)Documento2 pagineSaham Syariah: Kapitalisasi Pasar Bursa Efek Indonesia (RP Miliar)randigotama joviNessuna valutazione finora

- Public Sector Undertaking Bond MarketsDocumento4 paginePublic Sector Undertaking Bond MarketsMihir SansareNessuna valutazione finora

- Analysis of Telecom Sector - Indian Capital MarketDocumento16 pagineAnalysis of Telecom Sector - Indian Capital MarketJigar RathodNessuna valutazione finora

- March 2022Documento7 pagineMarch 2022Saiful IslamNessuna valutazione finora

- EXIMPolicyand Foreign Tradeof Indiain Post Reform Era AutosavedDocumento5 pagineEXIMPolicyand Foreign Tradeof Indiain Post Reform Era Autosavedricha sethiaNessuna valutazione finora

- Miggros - CaseDocumento4 pagineMiggros - CasefineksusgroupNessuna valutazione finora

- RussiaDocumento18 pagineRussiaBiplob nathNessuna valutazione finora

- MFIS Draft 1Documento116 pagineMFIS Draft 1ayush singlaNessuna valutazione finora

- National Stock Exchange: Research ReportDocumento21 pagineNational Stock Exchange: Research ReportPramod KamathNessuna valutazione finora

- FALLSEM2017-18 - BMT1018 - TH - SJT626 - VL2017181002984 - Reference Material IDocumento27 pagineFALLSEM2017-18 - BMT1018 - TH - SJT626 - VL2017181002984 - Reference Material IPulkit JainNessuna valutazione finora

- Annual Report - 2010Documento121 pagineAnnual Report - 2010Ayush JainNessuna valutazione finora

- Summer TrainingDocumento30 pagineSummer TrainingFakeha BegumNessuna valutazione finora

- Priyanka Matrial 2Documento198 paginePriyanka Matrial 2riddhiNessuna valutazione finora

- An Overview of The Indian Financial System in The Post-1950 PeriodDocumento25 pagineAn Overview of The Indian Financial System in The Post-1950 PeriodPalNessuna valutazione finora

- Road Accident Trends in Bangladesh: A Comprehensive Study: December 2011Documento11 pagineRoad Accident Trends in Bangladesh: A Comprehensive Study: December 2011MD SIAMNessuna valutazione finora

- Assignment On "Trends, Obstacles & Remedies of Foreign Investment"Documento18 pagineAssignment On "Trends, Obstacles & Remedies of Foreign Investment"RonyNessuna valutazione finora

- Edelweiss Fund Tracker - 31 May 2010Documento309 pagineEdelweiss Fund Tracker - 31 May 2010rpk1974Nessuna valutazione finora

- "Increase in Inflation Has Impacted The Real Return On Securities. in Some Cases, Real Returns HaveDocumento5 pagine"Increase in Inflation Has Impacted The Real Return On Securities. in Some Cases, Real Returns Havenithish ballalNessuna valutazione finora

- 5 Dec 16Documento3 pagine5 Dec 16asifNessuna valutazione finora

- Impact of Fiis On Stock Market Instability: 6.1 BackgroundDocumento14 pagineImpact of Fiis On Stock Market Instability: 6.1 BackgroundVaishali ShuklaNessuna valutazione finora

- Tojqi Paper Technical Efficiency Affecting Factors in Indian Banking Sector An Empirical AnalysisDocumento18 pagineTojqi Paper Technical Efficiency Affecting Factors in Indian Banking Sector An Empirical AnalysisDr Bhadrappa HaralayyaNessuna valutazione finora

- Fundamental Analysis Case Study of ICICI BankDocumento61 pagineFundamental Analysis Case Study of ICICI BankNirojini Bhat BhanNessuna valutazione finora

- Mini Project On NseDocumento19 pagineMini Project On Nsecharan tejaNessuna valutazione finora

- Export Import Condition of BangladeshDocumento20 pagineExport Import Condition of BangladeshMonirul MonirNessuna valutazione finora

- Smart InvestmentDocumento72 pagineSmart InvestmentGourab ChakrabortyNessuna valutazione finora

- Ahmad 31Documento21 pagineAhmad 31ahmadalmagharezNessuna valutazione finora

- PA2 - Wk6Documento13 paginePA2 - Wk6Ranjan KoiralaNessuna valutazione finora

- Module III: Derivatives: Chapter 3: Exchange Traded Currency Derivatives in IndiaDocumento8 pagineModule III: Derivatives: Chapter 3: Exchange Traded Currency Derivatives in Indiasantucan1Nessuna valutazione finora

- Tables Bond MarketDocumento4 pagineTables Bond MarketIshwar ChhedaNessuna valutazione finora

- Leec1er PDFDocumento9 pagineLeec1er PDFShubham RankaNessuna valutazione finora

- Holding Equity OpenDocumento36 pagineHolding Equity Opengame treeNessuna valutazione finora

- Clerical Pre Promotion - Final - TraineesDocumento358 pagineClerical Pre Promotion - Final - Traineesgolden79034Nessuna valutazione finora

- Relationship Between FDI and GDP of India: DatasetDocumento2 pagineRelationship Between FDI and GDP of India: DatasetHarveyNessuna valutazione finora

- Small Scale Industries by Anas AhamadDocumento17 pagineSmall Scale Industries by Anas AhamadMd Anas Ahmed AnasNessuna valutazione finora

- Quant ESG Equity Fund Sep 2022Documento9 pagineQuant ESG Equity Fund Sep 2022vnrNessuna valutazione finora

- Quant Mid Cap Fund Sep 2022Documento9 pagineQuant Mid Cap Fund Sep 2022vnrNessuna valutazione finora

- Portfolio Management at PromarketDocumento7 paginePortfolio Management at PromarketVarun AgrawalNessuna valutazione finora

- 562 Ijar-16777Documento5 pagine562 Ijar-16777Utkarsh BajpaiNessuna valutazione finora

- Miniproject Report: HDFC Bank & Kotak Mahindra BankDocumento34 pagineMiniproject Report: HDFC Bank & Kotak Mahindra BankAishwarya MenonNessuna valutazione finora

- Stats Data FDIDocumento7 pagineStats Data FDISanchit BudhirajaNessuna valutazione finora

- AppendixDocumento18 pagineAppendixwai phyoNessuna valutazione finora

- Mishkin Fmi09 PPT 20Documento56 pagineMishkin Fmi09 PPT 20lashia.williams69Nessuna valutazione finora

- NPASDocumento2 pagineNPASMaiyakabetaNessuna valutazione finora

- Securities Operations: A Guide to Trade and Position ManagementDa EverandSecurities Operations: A Guide to Trade and Position ManagementValutazione: 4 su 5 stelle4/5 (3)

- Buyside Risk Management SystemsDocumento16 pagineBuyside Risk Management SystemsjosephmeawadNessuna valutazione finora

- Oakdale Resources Limited and Its Controlled Entities Acn Annual ReportDocumento72 pagineOakdale Resources Limited and Its Controlled Entities Acn Annual ReportAlexNessuna valutazione finora

- An Example of The Difference-Merck and River BlindnessDocumento7 pagineAn Example of The Difference-Merck and River BlindnessMarilou Olaguir SañoNessuna valutazione finora

- Transtutors005 ch11 QuestionsDocumento25 pagineTranstutors005 ch11 QuestionsAstha GoplaniNessuna valutazione finora

- Sampoorna-Jeevan-Brochure 141119 v04 PDFDocumento24 pagineSampoorna-Jeevan-Brochure 141119 v04 PDFSTAR COMPUTERSNessuna valutazione finora

- Tally Accounting Package: Unit - 1Documento19 pagineTally Accounting Package: Unit - 1NagabhushanaNessuna valutazione finora

- 805 Financial Market Management SQPDocumento5 pagine805 Financial Market Management SQPajaydohre893Nessuna valutazione finora

- Equatorial Realty Vs Mayfair TheaterDocumento2 pagineEquatorial Realty Vs Mayfair TheaterSaji JimenoNessuna valutazione finora

- BI9009108 ApplicationFormDocumento9 pagineBI9009108 ApplicationFormSandip chourasiyaNessuna valutazione finora

- Work 3Documento114 pagineWork 3damienancoNessuna valutazione finora

- Investment Needs Analysis DraftDocumento62 pagineInvestment Needs Analysis DraftjdonNessuna valutazione finora

- Builder in Good FaithDocumento2 pagineBuilder in Good FaithpdalingayNessuna valutazione finora

- 2019-21 IInd Year Course Syllabus PDFDocumento136 pagine2019-21 IInd Year Course Syllabus PDFpushpdeepNessuna valutazione finora

- Gannon Compilation 2005 2022Documento2.726 pagineGannon Compilation 2005 2022bfbggNessuna valutazione finora

- IDFC FIRST Covered Call Option Strategy 09079021Documento3 pagineIDFC FIRST Covered Call Option Strategy 09079021forgi mistyNessuna valutazione finora

- Precedent Transactions - TemplateDocumento14 paginePrecedent Transactions - TemplateStanley ChengNessuna valutazione finora

- Part 1. Company Analysis - CSP's 5 C's of MarketingDocumento7 paginePart 1. Company Analysis - CSP's 5 C's of MarketingMajo Bulnes'Nessuna valutazione finora

- Bba Notes 6Documento53 pagineBba Notes 6RAJATNessuna valutazione finora

- Selling The WheelDocumento14 pagineSelling The WheelMihai GeambasuNessuna valutazione finora

- Ppt. 1Documento28 paginePpt. 1sadNessuna valutazione finora

- SSRN Id2209089Documento16 pagineSSRN Id2209089rovirysNessuna valutazione finora

- HMCost2e PPT Ch10Documento25 pagineHMCost2e PPT Ch10Rohit GuptaNessuna valutazione finora

- Options Training Course GuideDocumento80 pagineOptions Training Course Guidelenry101Nessuna valutazione finora

- Nism 8 Equity Derivatives Last Day Revision Test 1Documento54 pagineNism 8 Equity Derivatives Last Day Revision Test 1Nandi Grand86% (7)