Potrebbero piacerti anche

- Chapter02 AnglesDocumento40 pagineChapter02 Angleslen16328100% (1)

- Introduction To Taxation: (Taxes, Tax Laws and Tax Administration) by Daryl T. Evardone, CPADocumento35 pagineIntroduction To Taxation: (Taxes, Tax Laws and Tax Administration) by Daryl T. Evardone, CPAKyla Marie HubieraNessuna valutazione finora

- Preliminary Exam in Cost Accounting and ControlDocumento5 paginePreliminary Exam in Cost Accounting and ControlMohammadNessuna valutazione finora

- GenBio2 3Q Module1Documento8 pagineGenBio2 3Q Module1MohammadNessuna valutazione finora

- Taxation in The Philippine SDocumento22 pagineTaxation in The Philippine SBJ Ambat100% (1)

- Cosmology NotesDocumento22 pagineCosmology NotesSaint Benedict Center100% (1)

- Gen. Principles of TaxationDocumento22 pagineGen. Principles of TaxationPageduesca RouelNessuna valutazione finora

- Advanced Finite Element Model of Tsing Ma Bridge For Structural Health MonitoringDocumento32 pagineAdvanced Finite Element Model of Tsing Ma Bridge For Structural Health MonitoringZhang ChaodongNessuna valutazione finora

- Day 3 Lecture SlidesDocumento25 pagineDay 3 Lecture SlidesyebegashetNessuna valutazione finora

- Basics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.Da EverandBasics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.Nessuna valutazione finora

- Income Taxation CHAPTER 1Documento31 pagineIncome Taxation CHAPTER 1Armalyn CangqueNessuna valutazione finora

- SSPC - Guia 12Documento6 pagineSSPC - Guia 12José Alvaro Herrera Ramos50% (2)

- A Step by Step Approach To The Modeling of Chemical Engineering Processes, Using Excel For Simulation (2018)Documento182 pagineA Step by Step Approach To The Modeling of Chemical Engineering Processes, Using Excel For Simulation (2018)Anonymous NxpnI6jC100% (7)

- The Utopia of The Zero-OptionDocumento25 pagineThe Utopia of The Zero-Optiontamarapro50% (2)

- General Principles of Taxation: Tax 111 - Income Taxation Ferdinand C. Importado Cpa, MbaDocumento22 pagineGeneral Principles of Taxation: Tax 111 - Income Taxation Ferdinand C. Importado Cpa, Mbaangelo_maranan100% (1)

- Topic-1-An Overview of TaxationDocumento29 pagineTopic-1-An Overview of TaxationJaved AnwarNessuna valutazione finora

- Topic-1-An Overview of TaxationDocumento29 pagineTopic-1-An Overview of TaxationJaved AnwarNessuna valutazione finora

- What Is 'Taxation': Estate Taxes TaxesDocumento2 pagineWhat Is 'Taxation': Estate Taxes TaxesRandy DonatoNessuna valutazione finora

- Income Taxation 1Documento86 pagineIncome Taxation 1guerradhonaelizaNessuna valutazione finora

- Chapter 1 Introduction To TaxationDocumento21 pagineChapter 1 Introduction To TaxationErica FlorentinoNessuna valutazione finora

- Principles of TaxationDocumento51 paginePrinciples of TaxationAlvigrace PuguonNessuna valutazione finora

- Taxation: Basic Concepts and PrinciplesDocumento47 pagineTaxation: Basic Concepts and PrinciplesMaybelleNessuna valutazione finora

- Lesson 14 ABM161 Taxation For FinalsDocumento41 pagineLesson 14 ABM161 Taxation For FinalsNorhaliza D. SaripNessuna valutazione finora

- Lecture-1-An Overview of TaxationDocumento14 pagineLecture-1-An Overview of TaxationJaved AnwarNessuna valutazione finora

- Module 3 General Principles of TaxationDocumento80 pagineModule 3 General Principles of TaxationFlameNessuna valutazione finora

- BA122 SummaryDocumento6 pagineBA122 SummaryJaiavave LinogonNessuna valutazione finora

- Unit-I Taxation by Prof. Anbalagan ChinniahDocumento23 pagineUnit-I Taxation by Prof. Anbalagan ChinniahProf. Dr. Anbalagan ChinniahNessuna valutazione finora

- CLWTAXN General Principles of Taxation Part OneDocumento46 pagineCLWTAXN General Principles of Taxation Part Oneclassic swagNessuna valutazione finora

- Acfrogc9mb7nlbmkbcfuonpkva Vyrnoeit6djnpfc7lg6tcqzyu5ol816zlfbcl1raopr4fsadz2whfjxvv9nnopz-Lpheunvkzhneewx05ytz Fube13x36w Uybxnqntbje9wv-VkaanvllqmDocumento48 pagineAcfrogc9mb7nlbmkbcfuonpkva Vyrnoeit6djnpfc7lg6tcqzyu5ol816zlfbcl1raopr4fsadz2whfjxvv9nnopz-Lpheunvkzhneewx05ytz Fube13x36w Uybxnqntbje9wv-VkaanvllqmCrystal MaeNessuna valutazione finora

- Topic 3 Canons of TaxationDocumento20 pagineTopic 3 Canons of TaxationJaved AnwarNessuna valutazione finora

- Part I. Chapter 1 Fundamental PrinciplesDocumento39 paginePart I. Chapter 1 Fundamental PrinciplesCatherine GomezNessuna valutazione finora

- Quick Review On General Principles of TaxationDocumento15 pagineQuick Review On General Principles of TaxationJamesNessuna valutazione finora

- Government Without Any Expectation of Direct Return in Benefit ". Ability To Pay. Taxed in The Same Way Without Any DiscriminationDocumento42 pagineGovernment Without Any Expectation of Direct Return in Benefit ". Ability To Pay. Taxed in The Same Way Without Any DiscriminationyebegashetNessuna valutazione finora

- Introduction: Taxation: Anika Rafah Lecturer North South UniversityDocumento15 pagineIntroduction: Taxation: Anika Rafah Lecturer North South UniversityJarÎnAnJumChôwdhuryNessuna valutazione finora

- Taxation Chapter 1.1 - DDocumento13 pagineTaxation Chapter 1.1 - DLelouch LevyNessuna valutazione finora

- ACC2054 Malaysian Taxation System (Mar 2013) Lecture 1Documento13 pagineACC2054 Malaysian Taxation System (Mar 2013) Lecture 1Selva Bavani SelwaduraiNessuna valutazione finora

- 1 Microsoft PowerPoint PresentationDocumento22 pagine1 Microsoft PowerPoint PresentationHASNAT SABIRNessuna valutazione finora

- ACC717 Topic 1.TAXATIONDocumento29 pagineACC717 Topic 1.TAXATIONJason MaelumaNessuna valutazione finora

- General Principles On Taxation-2015Documento40 pagineGeneral Principles On Taxation-2015Henry M. Macatuno Jr.Nessuna valutazione finora

- Taxation General PrinciplesDocumento28 pagineTaxation General PrinciplesIzaNessuna valutazione finora

- Topic 1-Income Taxation With ExplanationDocumento50 pagineTopic 1-Income Taxation With ExplanationJewel ClairNessuna valutazione finora

- TaxationDocumento18 pagineTaxationMatthew MadriagaNessuna valutazione finora

- Week1-Local TaxationDocumento20 pagineWeek1-Local TaxationShanique WilliamsNessuna valutazione finora

- Sources of Revenues of Local Government Units Sources of Revenues of Local Government UnitsDocumento73 pagineSources of Revenues of Local Government Units Sources of Revenues of Local Government Unitsaige mascodNessuna valutazione finora

- 3 Chapter03Documento79 pagine3 Chapter03Kalkidan ZerihunNessuna valutazione finora

- Lecture Notes - PEconomics IIDocumento112 pagineLecture Notes - PEconomics IIAmelia BaileyNessuna valutazione finora

- Taxation PDFDocumento55 pagineTaxation PDFFatimaNessuna valutazione finora

- Lecture 2 - Taxation and Public SpendingDocumento34 pagineLecture 2 - Taxation and Public SpendingAmelia BaileyNessuna valutazione finora

- Lec 9 Fiscal Policy TaxationDocumento36 pagineLec 9 Fiscal Policy Taxationdua tanveerNessuna valutazione finora

- Taxation LawDocumento106 pagineTaxation Lawjohnanthony201Nessuna valutazione finora

- Taxation: General PrinciplesDocumento30 pagineTaxation: General PrinciplesJao FloresNessuna valutazione finora

- Tax Planning and Management TaxDocumento5 pagineTax Planning and Management TaxHarsha HarshaNessuna valutazione finora

- Chapter - Two: Meaning and Characteristics of TaxationDocumento61 pagineChapter - Two: Meaning and Characteristics of TaxationYoseph KassaNessuna valutazione finora

- LEAP Acc110 Income Taxation CREATE Module 1 and 2Documento12 pagineLEAP Acc110 Income Taxation CREATE Module 1 and 2Ella Blanca BuyaNessuna valutazione finora

- General Principles of TaxationDocumento26 pagineGeneral Principles of TaxationjoetapsNessuna valutazione finora

- Bintaxa ReadingsDocumento9 pagineBintaxa ReadingsAlex GonzalesNessuna valutazione finora

- Taxation TheoryDocumento32 pagineTaxation TheoryKaycia HyltonNessuna valutazione finora

- Theory and Basis of TaxationDocumento8 pagineTheory and Basis of TaxationGreggy BoyNessuna valutazione finora

- Taxation LawsDocumento15 pagineTaxation LawsVikas RockNessuna valutazione finora

- Chapter Three: General Overview of TaxationDocumento68 pagineChapter Three: General Overview of TaxationWagner AdugnaNessuna valutazione finora

- MEC 52 Notes Chapters 1 To 3Documento10 pagineMEC 52 Notes Chapters 1 To 3Princess Niña Layne SususcoNessuna valutazione finora

- Public Finance CH 2Documento30 paginePublic Finance CH 2kussia toramaNessuna valutazione finora

- Chapter One: Introduction To TaxationDocumento46 pagineChapter One: Introduction To Taxationembiale ayaluNessuna valutazione finora

- General Principles - Concept, Nature, and CharacteristicsDocumento17 pagineGeneral Principles - Concept, Nature, and CharacteristicsRico AbbiegailNessuna valutazione finora

- IntroductionDocumento30 pagineIntroductionSeifu BekeleNessuna valutazione finora

- Fundamental S of Taxati OnDocumento14 pagineFundamental S of Taxati OnMyka FranciscoNessuna valutazione finora

- RPH M4 Lesson 4 Canvas NotesDocumento2 pagineRPH M4 Lesson 4 Canvas NotesJELA MAE RIOSANessuna valutazione finora

- General Principles of TaxationDocumento50 pagineGeneral Principles of TaxationJessa PerdigonNessuna valutazione finora

- TAX - 601 - Individuals - Abapo, Mary Jhudiel G.Documento53 pagineTAX - 601 - Individuals - Abapo, Mary Jhudiel G.Mohammad100% (1)

- Tabulation Guidelines 1Documento4 pagineTabulation Guidelines 1MohammadNessuna valutazione finora

- 5 Form MembershipDocumento1 pagina5 Form MembershipMohammadNessuna valutazione finora

- Tabulation Guidelines 1Documento4 pagineTabulation Guidelines 1MohammadNessuna valutazione finora

- TAX 1801 Basic Principles - Hadji Usop, Norhanisah B PDFDocumento26 pagineTAX 1801 Basic Principles - Hadji Usop, Norhanisah B PDFMohammadNessuna valutazione finora

- Banga Executive Summary 2018 PDFDocumento5 pagineBanga Executive Summary 2018 PDFMohammadNessuna valutazione finora

- System Theory 1Documento9 pagineSystem Theory 1MohammadNessuna valutazione finora

- Chapter 3 - The Government Accounting ProcessDocumento14 pagineChapter 3 - The Government Accounting ProcessMohammadNessuna valutazione finora

- CHAPTER 4 - Revenues and Other ReceiptsDocumento26 pagineCHAPTER 4 - Revenues and Other ReceiptsMohammadNessuna valutazione finora

- Extemporaneous SpeechDocumento2 pagineExtemporaneous SpeechMohammadNessuna valutazione finora

- History of The United StatesDocumento5 pagineHistory of The United StatesMohammadNessuna valutazione finora

- OrMan Chapter 5Documento36 pagineOrMan Chapter 5MohammadNessuna valutazione finora

- Pacalna - ApplicationDocumento3 paginePacalna - ApplicationMohammadNessuna valutazione finora

- NAME: - SECTION: - : THIRD QUARTER - Learning ModuleDocumento4 pagineNAME: - SECTION: - : THIRD QUARTER - Learning ModuleMohammadNessuna valutazione finora

- CHAPTER 5 - DisbursementDocumento25 pagineCHAPTER 5 - DisbursementMohammadNessuna valutazione finora

- D. All of The Above: A. Progressive TaxDocumento6 pagineD. All of The Above: A. Progressive TaxMohammadNessuna valutazione finora

- MoneyDocumento23 pagineMoneyMohammadNessuna valutazione finora

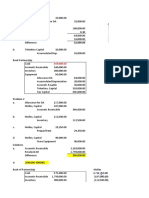

- Partnership Operations (Solutions)Documento4 paginePartnership Operations (Solutions)MohammadNessuna valutazione finora

- Partnership Formation - SolutionsDocumento5 paginePartnership Formation - SolutionsMohammadNessuna valutazione finora

- Rule-Based Reasoning Relies On The Use of Syllogisms, or Arguments Based On Formal Logic. ADocumento1 paginaRule-Based Reasoning Relies On The Use of Syllogisms, or Arguments Based On Formal Logic. AMohammadNessuna valutazione finora

- Multiple Choice THEORY: Choose The Letter of The Correct AnswerDocumento4 pagineMultiple Choice THEORY: Choose The Letter of The Correct AnswerMohammadNessuna valutazione finora

- Act102 Assessment2Documento4 pagineAct102 Assessment2MohammadNessuna valutazione finora

- Filipina ("Philippine National March"), Is The: FilipinasDocumento1 paginaFilipina ("Philippine National March"), Is The: FilipinasMohammadNessuna valutazione finora

- Public Corporation CasesDocumento41 paginePublic Corporation CasesMohammadNessuna valutazione finora

- Income Tax On IndividualsDocumento25 pagineIncome Tax On IndividualsMohammadNessuna valutazione finora

- What Is Transportation Engineering? Divided Into Four PartsDocumento8 pagineWhat Is Transportation Engineering? Divided Into Four PartsMohammadNessuna valutazione finora

- PCL CasesDocumento19 paginePCL CasesMohammadNessuna valutazione finora

- Four-Fold Test Economic Reality Test Two-Tiered Test (Or Multi-Factor Test)Documento18 pagineFour-Fold Test Economic Reality Test Two-Tiered Test (Or Multi-Factor Test)MohammadNessuna valutazione finora

- Physical Education: Learning Activity SheetDocumento13 paginePhysical Education: Learning Activity SheetRhea Jane B. CatalanNessuna valutazione finora

- NyirabahireS Chapter5 PDFDocumento7 pagineNyirabahireS Chapter5 PDFAndrew AsimNessuna valutazione finora

- AVERY, Adoratio PurpuraeDocumento16 pagineAVERY, Adoratio PurpuraeDejan MitreaNessuna valutazione finora

- Midterm Examination: General MathematicsDocumento5 pagineMidterm Examination: General MathematicsJenalyn CardanoNessuna valutazione finora

- The Divine Liturgy Syro Malankara ChurchDocumento4 pagineThe Divine Liturgy Syro Malankara ChurchGian Marco TallutoNessuna valutazione finora

- Selvanathan-7e 17Documento92 pagineSelvanathan-7e 17Linh ChiNessuna valutazione finora

- b8c2 PDFDocumento193 pagineb8c2 PDFRhIdho POetraNessuna valutazione finora

- Meralco v. CastilloDocumento2 pagineMeralco v. CastilloJoven CamusNessuna valutazione finora

- Bhagavad Gita Ch.1 Shlok 4++Documento1 paginaBhagavad Gita Ch.1 Shlok 4++goldenlion1Nessuna valutazione finora

- (OCM) Chapter 1 Principles of ManagementDocumento23 pagine(OCM) Chapter 1 Principles of ManagementMehfooz PathanNessuna valutazione finora

- ESSAYDocumento1 paginaESSAYJunalie GregoreNessuna valutazione finora

- 3 Murex HIV Ag Ab CombinationDocumento7 pagine3 Murex HIV Ag Ab CombinationElias Dii Rivas GarvanNessuna valutazione finora

- Sir Rizwan Ghani AssignmentDocumento5 pagineSir Rizwan Ghani AssignmentSara SyedNessuna valutazione finora

- Bar Graphs and HistogramsDocumento9 pagineBar Graphs and HistogramsLeon FouroneNessuna valutazione finora

- Notes 1Documento30 pagineNotes 1Antal TóthNessuna valutazione finora

- 10 1108 - JKM 01 2020 0064Documento23 pagine10 1108 - JKM 01 2020 0064BBA THESISNessuna valutazione finora

- (2016) The Role of Requirements in The Success or Failure of Software Projects-DikonversiDocumento11 pagine(2016) The Role of Requirements in The Success or Failure of Software Projects-DikonversiFajar HatmalNessuna valutazione finora

- 007-Student Council NominationDocumento2 pagine007-Student Council NominationrimsnibmNessuna valutazione finora

- 6 Ci Sinif Word Definition 6Documento2 pagine6 Ci Sinif Word Definition 6poladovaaysen11Nessuna valutazione finora

- Astro ExamDocumento7 pagineAstro ExamRitu DuaNessuna valutazione finora

- Don'T Forget To Edit: Input Data Sheet For E-Class RecordDocumento12 pagineDon'T Forget To Edit: Input Data Sheet For E-Class RecordCherry Lyn BelgiraNessuna valutazione finora

- SMF Update Barang 05 Desember 2022Documento58 pagineSMF Update Barang 05 Desember 2022Apotek Ibnu RusydNessuna valutazione finora

- Skills For Developing Yourself As A LeaderDocumento26 pagineSkills For Developing Yourself As A LeaderhIgh QuaLIty SVTNessuna valutazione finora

- Who Di 31-4 Atc-DddDocumento6 pagineWho Di 31-4 Atc-DddHenderika Lado MauNessuna valutazione finora