Potrebbero piacerti anche

- What Is A LOT in Forex Trading - Lot Sizes ExplainedDocumento23 pagineWhat Is A LOT in Forex Trading - Lot Sizes Explainedomar lakhrash100% (2)

- C14 Krugman 12e BGuizaniDocumento63 pagineC14 Krugman 12e BGuizani425q4fqgg4Nessuna valutazione finora

- The United Nation Organization - The Committee of 300 - Treasurry Certificate - SfagiDocumento112 pagineThe United Nation Organization - The Committee of 300 - Treasurry Certificate - SfagisfagiNessuna valutazione finora

- The Foreign Exchange MarketDocumento34 pagineThe Foreign Exchange Marketsaurabh.kum100% (9)

- Performance Contracting in KenyaDocumento10 paginePerformance Contracting in Kenyawangaoe100% (9)

- Chapter 4 - Managing in A Global EnvironmentDocumento5 pagineChapter 4 - Managing in A Global Environmentbiancag_91Nessuna valutazione finora

- You Have Completed: Week9 FX MKTDocumento9 pagineYou Have Completed: Week9 FX MKTDerek LowNessuna valutazione finora

- Impossible TrinityDocumento43 pagineImpossible TrinityArnab Kumar SahaNessuna valutazione finora

- Chapter 19 - Advacc Solman Chapter 19 - Advacc SolmanDocumento16 pagineChapter 19 - Advacc Solman Chapter 19 - Advacc SolmanDrew BanlutaNessuna valutazione finora

- FX Risk Management Transaction Exposure: Slide 1Documento55 pagineFX Risk Management Transaction Exposure: Slide 1prakashputtuNessuna valutazione finora

- The International Monetary SystemDocumento27 pagineThe International Monetary SystemRoopesh KumarNessuna valutazione finora

- Ias 20 - Gov't GrantDocumento19 pagineIas 20 - Gov't GrantGail Bermudez100% (1)

- Answers To End of Chapter Questions and Applications: 3. Imperfect MarketsDocumento2 pagineAnswers To End of Chapter Questions and Applications: 3. Imperfect Marketssuhayb_1988Nessuna valutazione finora

- Bangladesh Krishi Bank Overall Performance Recent 5yrs PDFDocumento15 pagineBangladesh Krishi Bank Overall Performance Recent 5yrs PDFAnimesh DharNessuna valutazione finora

- Portfolio ManagementDocumento40 paginePortfolio ManagementSayaliRewaleNessuna valutazione finora

- Various Forces of Change in Business EnviromentDocumento5 pagineVarious Forces of Change in Business Enviromentabhijitbiswas25Nessuna valutazione finora

- 15 International Working Capital Management: Chapter ObjectivesDocumento16 pagine15 International Working Capital Management: Chapter ObjectivesNancy DsouzaNessuna valutazione finora

- GDPDocumento40 pagineGDPSimantoPreeomNessuna valutazione finora

- Nestle-Organizational Behaviour With Refrence To 17 PointsDocumento9 pagineNestle-Organizational Behaviour With Refrence To 17 PointsKhaWaja HamMadNessuna valutazione finora

- Research Paper Time Value of Money 2Documento11 pagineResearch Paper Time Value of Money 2Nhung TaNessuna valutazione finora

- Solved - United Technologies Corporation (UTC), Based in Hartfor...Documento4 pagineSolved - United Technologies Corporation (UTC), Based in Hartfor...Saad ShafiqNessuna valutazione finora

- International Business, AssignmentDocumento16 pagineInternational Business, Assignmentمحمد شاميم100% (1)

- Techniques For Managing ExposureDocumento26 pagineTechniques For Managing Exposureprasanthgeni22100% (1)

- 5.2 Q JPMorgan Chase FXDocumento7 pagine5.2 Q JPMorgan Chase FXSanaFatimaNessuna valutazione finora

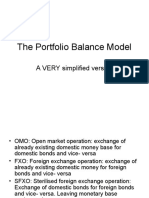

- 9.the Portfolio Balance ModelDocumento40 pagine9.the Portfolio Balance ModelVelichka DimitrovaNessuna valutazione finora

- MBA 113 Financial Management and Corporate Finance Full RetakeDocumento27 pagineMBA 113 Financial Management and Corporate Finance Full RetakeJitendra PatidarNessuna valutazione finora

- AC301 Off Balance Sheet FinancingDocumento25 pagineAC301 Off Balance Sheet Financinghui7411Nessuna valutazione finora

- Accounting Textbook Solutions - 46Documento19 pagineAccounting Textbook Solutions - 46acc-expertNessuna valutazione finora

- BFF5270 Topic 4 Tutorial QuestionsDocumento6 pagineBFF5270 Topic 4 Tutorial QuestionsmattNessuna valutazione finora

- Notes - MARKETING - OF - FINANCIAL SERVICES - 2020Documento69 pagineNotes - MARKETING - OF - FINANCIAL SERVICES - 2020Rozy SinghNessuna valutazione finora

- NN 5 Chap 4 Review of AccountingDocumento10 pagineNN 5 Chap 4 Review of AccountingNguyet NguyenNessuna valutazione finora

- Mcleod Russel India LTD.: CMP: Rs.361Documento2 pagineMcleod Russel India LTD.: CMP: Rs.361dynamic2004Nessuna valutazione finora

- Group 4Documento3 pagineGroup 4Rizma RizwanNessuna valutazione finora

- Fin410 Repot Final File Group 3Documento28 pagineFin410 Repot Final File Group 3Shouvo Kumar Kundu 2012347630Nessuna valutazione finora

- International Marketing & Operations Definition)Documento18 pagineInternational Marketing & Operations Definition)Fasika MeketeNessuna valutazione finora

- International Finance Ass 2Documento5 pagineInternational Finance Ass 2Sugen RajNessuna valutazione finora

- Industrial Relations (HR 404)Documento49 pagineIndustrial Relations (HR 404)Munmun GoswamiNessuna valutazione finora

- Long-Term Financial Planning and GrowthDocumento26 pagineLong-Term Financial Planning and GrowthpushmbaNessuna valutazione finora

- Chp-4 Capital Project FundDocumento8 pagineChp-4 Capital Project FundkasimNessuna valutazione finora

- SDMT - Final Assignment Case Study PDFDocumento3 pagineSDMT - Final Assignment Case Study PDFCR7 الظاهرةNessuna valutazione finora

- Assignment - MQC708Documento16 pagineAssignment - MQC708Eng Abdulkadir MahamedNessuna valutazione finora

- CadburyDocumento37 pagineCadburyjdh_apsNessuna valutazione finora

- Wealth MaximizationDocumento4 pagineWealth MaximizationDeeba MalikNessuna valutazione finora

- Buisness CycleDocumento8 pagineBuisness CycleyagyatiwariNessuna valutazione finora

- Capital StructureDocumento6 pagineCapital StructureHasan Zahoor100% (1)

- Strategic Plan EvaluationDocumento5 pagineStrategic Plan EvaluationCEDRIC JONESNessuna valutazione finora

- JAIBB 97th 2023 105. - Business Communication in Financial Institutions BCFIDocumento2 pagineJAIBB 97th 2023 105. - Business Communication in Financial Institutions BCFIarif rahmanNessuna valutazione finora

- Analysis of Pakistan Cement SectorDocumento43 pagineAnalysis of Pakistan Cement SectorLeena SaleemNessuna valutazione finora

- Recession FinalDocumento40 pagineRecession FinalMehwish JavedNessuna valutazione finora

- 2004 - Webb - An Examination of Socially Responsible Firms' Board Structure. Journal of Management and Governance, 8, 255-277.Documento23 pagine2004 - Webb - An Examination of Socially Responsible Firms' Board Structure. Journal of Management and Governance, 8, 255-277.ahmed sharkasNessuna valutazione finora

- 1.2 Doc-20180120-Wa0002Documento23 pagine1.2 Doc-20180120-Wa0002Prachet KulkarniNessuna valutazione finora

- International Finance ManagementDocumento33 pagineInternational Finance ManagementAkshay SinghNessuna valutazione finora

- Conduct of Monetary Policy Goal and TargetsDocumento12 pagineConduct of Monetary Policy Goal and TargetsSumra KhanNessuna valutazione finora

- Unit 2 Capital StructureDocumento27 pagineUnit 2 Capital StructureNeha RastogiNessuna valutazione finora

- Advisor Recruitment in Icici PrudentialDocumento23 pagineAdvisor Recruitment in Icici PrudentialIsrar MahiNessuna valutazione finora

- Summer Internship ReportDocumento5 pagineSummer Internship ReportBharat NarulaNessuna valutazione finora

- Assignment I Questions Econ. For Acct & Fin. 2023Documento3 pagineAssignment I Questions Econ. For Acct & Fin. 2023Demelash FikaduNessuna valutazione finora

- Asset Backed SecuritiesDocumento179 pagineAsset Backed SecuritiesShivani NidhiNessuna valutazione finora

- International Financial Management AssignmentDocumento12 pagineInternational Financial Management AssignmentMasara OwenNessuna valutazione finora

- Mergers and Acquisitions SolutionsDocumento56 pagineMergers and Acquisitions Solutionstseboblessing7Nessuna valutazione finora

- Colgate Palmolive AnalysisDocumento5 pagineColgate Palmolive AnalysisprincearoraNessuna valutazione finora

- Ch. 02 Types of FinancingDocumento85 pagineCh. 02 Types of FinancingUmesh Raj Pandeya100% (1)

- Advantages and Disadvantages of Marginal CostingDocumento4 pagineAdvantages and Disadvantages of Marginal CostingnileshmsawantNessuna valutazione finora

- Chap-17-Lending Policies and ProceduresDocumento30 pagineChap-17-Lending Policies and ProceduresNazmul H. PalashNessuna valutazione finora

- The Four Walls: Live Like the Wind, Free, Without HindrancesDa EverandThe Four Walls: Live Like the Wind, Free, Without HindrancesValutazione: 5 su 5 stelle5/5 (1)

- Topic 6 Cost of CapitalDocumento61 pagineTopic 6 Cost of CapitalAdam Mo AliNessuna valutazione finora

- Topic 5 Bond ValuationDocumento56 pagineTopic 5 Bond ValuationAdam Mo AliNessuna valutazione finora

- Topic 4 Valuation of SharesDocumento31 pagineTopic 4 Valuation of SharesAdam Mo AliNessuna valutazione finora

- Financial Management MaterialsDocumento39 pagineFinancial Management MaterialsAdam Mo AliNessuna valutazione finora

- To Establish If There Is A Relationship Between Two VariablesDocumento1 paginaTo Establish If There Is A Relationship Between Two VariablesAdam Mo AliNessuna valutazione finora

- Ninjatrader Futures Contract DetailsDocumento3 pagineNinjatrader Futures Contract DetailsmatusalemcassimNessuna valutazione finora

- 2exercise - Understand Exchange RatesDocumento5 pagine2exercise - Understand Exchange RatesCalantha SheryNessuna valutazione finora

- Banking - Homework 1Documento2 pagineBanking - Homework 1Youssef CristoNessuna valutazione finora

- Pros and Cons of Different Exchange Rate SystemsDocumento4 paginePros and Cons of Different Exchange Rate Systemsdanishia09Nessuna valutazione finora

- Revision Notes For Class 12 Macro Economics Chapter 6 - Free PDF DownloadDocumento8 pagineRevision Notes For Class 12 Macro Economics Chapter 6 - Free PDF DownloadVibhuti BatraNessuna valutazione finora

- Presentation On " ": Devi Ahilya Vishwavidyalaya, Indore (A State Govt. Statutory University of M.P.)Documento20 paginePresentation On " ": Devi Ahilya Vishwavidyalaya, Indore (A State Govt. Statutory University of M.P.)Buddhapratap RathoreNessuna valutazione finora

- HKB 18 Manpowerpolicy InwardremittancesDocumento50 pagineHKB 18 Manpowerpolicy InwardremittancesFahimNessuna valutazione finora

- Indian Rupee: People Also AskDocumento1 paginaIndian Rupee: People Also AskAadish ChopraNessuna valutazione finora

- How Much Is Dollar To Naira Today - Google SearchDocumento1 paginaHow Much Is Dollar To Naira Today - Google SearchMondaychukwu101Nessuna valutazione finora

- Theories of Exchange Rate Determination - NotesDocumento12 pagineTheories of Exchange Rate Determination - NotesSewale AbateNessuna valutazione finora

- Ebook (ThekillerTechnuique) RecognizedDocumento27 pagineEbook (ThekillerTechnuique) RecognizedSagar BhandariNessuna valutazione finora

- Lista MCDocumento74 pagineLista MCANA GomesNessuna valutazione finora

- Trade Journal - DitariDocumento43 pagineTrade Journal - DitariNexhat RamadaniNessuna valutazione finora

- MONEYDocumento5 pagineMONEYShazia SadhikaliNessuna valutazione finora

- A) The Following Is The Iphone 7 Price List and The Spot Exchange Rate For Both CountriesDocumento10 pagineA) The Following Is The Iphone 7 Price List and The Spot Exchange Rate For Both CountriesDR LuotanNessuna valutazione finora

- Ninjatrader Forex Spreads Margins PDFDocumento2 pagineNinjatrader Forex Spreads Margins PDFvaldyrheimNessuna valutazione finora

- Sales Invoice RK Associates06 From RK ASSOCIATESDocumento1 paginaSales Invoice RK Associates06 From RK ASSOCIATESsasikumar durairajanNessuna valutazione finora

- Quotation: TO: Mr. Bryan Mayoralgo Municipality of Alicia, IsabelaDocumento4 pagineQuotation: TO: Mr. Bryan Mayoralgo Municipality of Alicia, IsabelaBryan MayoralgoNessuna valutazione finora

- Spread and Spread %Documento2 pagineSpread and Spread %Hola Gamer100% (1)

- Unit 4.6 Exchange RatesDocumento22 pagineUnit 4.6 Exchange RatesdeepneupaneNessuna valutazione finora

- Catalog Mini BussesDocumento1 paginaCatalog Mini BussespancoachesNessuna valutazione finora

- Lessons4Ielts - Reading (2) - Page 106-113Documento8 pagineLessons4Ielts - Reading (2) - Page 106-113Pham VuongNessuna valutazione finora

- Open Economy - Session 9-10Documento8 pagineOpen Economy - Session 9-10Abhyudaya BharadwajNessuna valutazione finora