Potrebbero piacerti anche

- Code of Ethics Bureau Veritas 2008Documento15 pagineCode of Ethics Bureau Veritas 2008Rizal FalevyNessuna valutazione finora

- EarningsperShare Finacc5Documento3 pagineEarningsperShare Finacc5Miladanica Barcelona BarracaNessuna valutazione finora

- Account ClassificationDocumento2 pagineAccount ClassificationMary96% (23)

- Chapter 22 - Retained EarningsDocumento35 pagineChapter 22 - Retained Earningswala akong pake sayoNessuna valutazione finora

- Book1 Group Act5110Documento9 pagineBook1 Group Act5110SAMNessuna valutazione finora

- CHAPTER 12 - Interim Financial ReportingDocumento47 pagineCHAPTER 12 - Interim Financial ReportingChristian Gatchalian100% (1)

- Basic Eps Praac Valix 2018pdf DDDocumento20 pagineBasic Eps Praac Valix 2018pdf DDCaptain ObviousNessuna valutazione finora

- Acctg 2 QuizDocumento4 pagineAcctg 2 QuizAshNor RandyNessuna valutazione finora

- Activity 1 - FS Analysis AnswerDocumento6 pagineActivity 1 - FS Analysis AnswerMelvert Alvarez MacaranasNessuna valutazione finora

- F-92 Asset Retirement With CustomerDocumento9 pagineF-92 Asset Retirement With CustomerOkikiri Omeiza RabiuNessuna valutazione finora

- EO No. 008 2018 REORGANIZATION OF BPOC 2Documento2 pagineEO No. 008 2018 REORGANIZATION OF BPOC 2Christian Gatchalian100% (5)

- Errors and Irregularities in The Transaction CycleDocumento22 pagineErrors and Irregularities in The Transaction CycleVatchdemonNessuna valutazione finora

- EO No. 008 2018 REORGANIZATION OF BPOC 2Documento2 pagineEO No. 008 2018 REORGANIZATION OF BPOC 2Christian Gatchalian50% (4)

- Role To T-Code MappingDocumento1.331 pagineRole To T-Code MappingAbdelhamid HarakatNessuna valutazione finora

- CHAPTER 11 - Changes in Accounting Policy, Prior Period ErrorsDocumento24 pagineCHAPTER 11 - Changes in Accounting Policy, Prior Period ErrorsChristian GatchalianNessuna valutazione finora

- Assignment Questions - Suggested Answers (M13-6, M13-7, E6-3, E6-18, E6-21, E6-24, P6-3, P6-7)Documento8 pagineAssignment Questions - Suggested Answers (M13-6, M13-7, E6-3, E6-18, E6-21, E6-24, P6-3, P6-7)Ivy KwokNessuna valutazione finora

- CHAPTER 25 - SMEs Financial StatementsDocumento43 pagineCHAPTER 25 - SMEs Financial StatementsChristian Gatchalian100% (2)

- EO No. 005 2018 REORGANIZATION BDRRMC COMPOSITIONDocumento4 pagineEO No. 005 2018 REORGANIZATION BDRRMC COMPOSITIONChristian Gatchalian100% (13)

- EO No. 005 2018 REORGANIZATION BDRRMC COMPOSITIONDocumento4 pagineEO No. 005 2018 REORGANIZATION BDRRMC COMPOSITIONChristian Gatchalian75% (4)

- Case Study: Accounting Information SystemDocumento9 pagineCase Study: Accounting Information SystemAlliah SomidoNessuna valutazione finora

- Petite Company Reported The Following Current Assets On December 31Documento1 paginaPetite Company Reported The Following Current Assets On December 31Katrina Dela CruzNessuna valutazione finora

- Public Accountancy PracticeDocumento69 paginePublic Accountancy Practicelov3m3100% (2)

- 5134649879operating Segment FinalDocumento8 pagine5134649879operating Segment FinalGlen JavellanaNessuna valutazione finora

- Dari GoogleDocumento6 pagineDari Googleabc defNessuna valutazione finora

- Lesson 6 Business TaxesDocumento9 pagineLesson 6 Business TaxesReino CabitacNessuna valutazione finora

- Saint Joseph College of Sindangan Incorporated College of AccountancyDocumento18 pagineSaint Joseph College of Sindangan Incorporated College of AccountancyRendall Craig Refugio0% (1)

- Mga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Documento12 pagineMga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Hannah Jane UmbayNessuna valutazione finora

- AssignmentDocumento2 pagineAssignmentLois JoseNessuna valutazione finora

- Statement of Comprehensive Income Part 2Documento8 pagineStatement of Comprehensive Income Part 2AG VenturesNessuna valutazione finora

- Advacc DecDocumento8 pagineAdvacc DecJerico CastilloNessuna valutazione finora

- Chapter 1Documento13 pagineChapter 1Ella Marie WicoNessuna valutazione finora

- Advanced Accounting Part 2 Dayag 2015 Chapter 4 (2022)Documento68 pagineAdvanced Accounting Part 2 Dayag 2015 Chapter 4 (2022)Mazikeen DeckerNessuna valutazione finora

- I Am Sharing 'SIM-ANSWERS - 6th-Exam-Topics - Hyperinflation - PABRES' With YouDocumento9 pagineI Am Sharing 'SIM-ANSWERS - 6th-Exam-Topics - Hyperinflation - PABRES' With YouJeric TorionNessuna valutazione finora

- Let's Analyze: Pacalna, Anifah BDocumento2 pagineLet's Analyze: Pacalna, Anifah BAnifahchannie PacalnaNessuna valutazione finora

- 8 - PFRS 15 Five Step Model PDFDocumento6 pagine8 - PFRS 15 Five Step Model PDFDarlene Faye Cabral RosalesNessuna valutazione finora

- AainvtyDocumento4 pagineAainvtyRodolfo SayangNessuna valutazione finora

- IA3 Chapter 22 29Documento5 pagineIA3 Chapter 22 29ZicoNessuna valutazione finora

- Module 5&6Documento29 pagineModule 5&6Lee DokyeomNessuna valutazione finora

- Homework On Statement of Cash FlowsDocumento2 pagineHomework On Statement of Cash FlowsAmy SpencerNessuna valutazione finora

- Events After The Reporting Period NCA Held For Disposal Discontinued OperationsDocumento2 pagineEvents After The Reporting Period NCA Held For Disposal Discontinued OperationsJeremiah DavidNessuna valutazione finora

- CH 27 FinmanDocumento3 pagineCH 27 FinmanKismith Aile MacedaNessuna valutazione finora

- Consolidated Financial Statements - Acquistion DateDocumento52 pagineConsolidated Financial Statements - Acquistion DateXavier AresNessuna valutazione finora

- Chapter 14 Other SolutionDocumento18 pagineChapter 14 Other SolutionChristine BaguioNessuna valutazione finora

- Coursehero 12Documento2 pagineCoursehero 12nhbNessuna valutazione finora

- Interim Financial Reporting: Problem 45-1: True or FalseDocumento7 pagineInterim Financial Reporting: Problem 45-1: True or FalseMarjorieNessuna valutazione finora

- Chapter 17 AuditingDocumento48 pagineChapter 17 AuditingMisshtaC0% (1)

- Problem 17-1, ContinuedDocumento6 pagineProblem 17-1, ContinuedJohn Carlo D MedallaNessuna valutazione finora

- CVP AnalysisDocumento24 pagineCVP AnalysisKim Cherry BulanNessuna valutazione finora

- Acctg26: Intermediate Accounting 3Documento33 pagineAcctg26: Intermediate Accounting 3Jeane Mae BooNessuna valutazione finora

- AE18.1 Financial Markets and Financial SystemDocumento23 pagineAE18.1 Financial Markets and Financial SystemTrishia Mae OliverosNessuna valutazione finora

- The Purchasing/ Accounts Payable/ Cash Disbursement (P/AP/CD) ProcessDocumento17 pagineThe Purchasing/ Accounts Payable/ Cash Disbursement (P/AP/CD) ProcessJonah Mark Tabuldan DebomaNessuna valutazione finora

- Unmodified ReportDocumento2 pagineUnmodified ReportErica CaliuagNessuna valutazione finora

- Discontinued Operation, Segment and Interim ReportingDocumento22 pagineDiscontinued Operation, Segment and Interim Reportinghis dimples appear, the great lee seo jinNessuna valutazione finora

- Sycip Gorres Velayo & Co.: HistoryDocumento5 pagineSycip Gorres Velayo & Co.: HistoryYonko ManotaNessuna valutazione finora

- FINAMAA Topic 2 Additional ActivityDocumento2 pagineFINAMAA Topic 2 Additional ActivityJeasmine Andrea Diane PayumoNessuna valutazione finora

- Sales Agency AccountingDocumento11 pagineSales Agency AccountingJade MarkNessuna valutazione finora

- Financial-Management 345Documento1 paginaFinancial-Management 345khurramNessuna valutazione finora

- Multiple Choice-ProbDocumento5 pagineMultiple Choice-ProbAngela RuedasNessuna valutazione finora

- C18 - Defined Benefit Plan PDFDocumento23 pagineC18 - Defined Benefit Plan PDFKristine Diane CABAnASNessuna valutazione finora

- 07 Interim Reporting FinalDocumento3 pagine07 Interim Reporting FinalMakoy BixenmanNessuna valutazione finora

- Statement of Comprehensive Income Part 2 StudentDocumento7 pagineStatement of Comprehensive Income Part 2 StudentAG VenturesNessuna valutazione finora

- Far-1 4Documento3 pagineFar-1 4Raymundo Eirah100% (1)

- Acc 310 - M004Documento12 pagineAcc 310 - M004Edward Glenn BaguiNessuna valutazione finora

- Practical Accounting 1 ReviewerDocumento13 paginePractical Accounting 1 ReviewerKimberly RamosNessuna valutazione finora

- Partnership FormationDocumento13 paginePartnership FormationGround ZeroNessuna valutazione finora

- FM 225 Kulang 4Documento4 pagineFM 225 Kulang 4Karen AlonsagayNessuna valutazione finora

- Nature and Background of The Specialized IndustryDocumento3 pagineNature and Background of The Specialized IndustryEly RiveraNessuna valutazione finora

- Quiz - Act 07A: I. Theories: ProblemsDocumento2 pagineQuiz - Act 07A: I. Theories: ProblemsShawn Organo0% (1)

- Name: Jean Rose T. Bustamante Bsma-3: Let's CheckDocumento10 pagineName: Jean Rose T. Bustamante Bsma-3: Let's CheckJean Rose Tabagay BustamanteNessuna valutazione finora

- San Sebastian College Recoletos de Cavite Management Accounting Finals Christopher C. LimDocumento5 pagineSan Sebastian College Recoletos de Cavite Management Accounting Finals Christopher C. LimAllyssa Kassandra LucesNessuna valutazione finora

- QUIZ OPT Part IIDocumento2 pagineQUIZ OPT Part IIJenny Gomez Ibasco0% (2)

- Accounting For Special Transactions and Cost Accounting and ControlDocumento12 pagineAccounting For Special Transactions and Cost Accounting and ControlRNessuna valutazione finora

- Activity 2Documento3 pagineActivity 2LFGS Finals0% (1)

- B215 AC09 Buy First Sell Later - 6th Presentation - 25may2009Documento35 pagineB215 AC09 Buy First Sell Later - 6th Presentation - 25may2009tohqinzhi100% (1)

- ACTIVITY QUESTIONS - RMNGTDocumento7 pagineACTIVITY QUESTIONS - RMNGTChristian GatchalianNessuna valutazione finora

- CHAPTER 24 - SMEs DefinitionDocumento17 pagineCHAPTER 24 - SMEs DefinitionChristian GatchalianNessuna valutazione finora

- Chapter NineDocumento5 pagineChapter NineAdefolajuwon ShoberuNessuna valutazione finora

- Ija Jun 2019Documento140 pagineIja Jun 2019Bitopan DasNessuna valutazione finora

- Aat Willis Ch15Documento27 pagineAat Willis Ch15CJNessuna valutazione finora

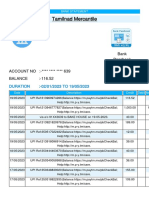

- Tamilnad Mercantile1684550531048Documento25 pagineTamilnad Mercantile1684550531048Miracle KhordsNessuna valutazione finora

- Ind As 101 - First Time Adoption of Indian Accounting StandardsDocumento5 pagineInd As 101 - First Time Adoption of Indian Accounting StandardsRaghavanNessuna valutazione finora

- Bsac 306 - Govacc Seatwork 1 Overview of Govt Acctg-Student Copy - RoldanDocumento6 pagineBsac 306 - Govacc Seatwork 1 Overview of Govt Acctg-Student Copy - RoldanJheraldinemae RoldanNessuna valutazione finora

- China Rail Cons - 2012 Annual Results Announcement PDFDocumento359 pagineChina Rail Cons - 2012 Annual Results Announcement PDFalan888Nessuna valutazione finora

- 2018 Annual Inspections Report enDocumento12 pagine2018 Annual Inspections Report ensekar raniNessuna valutazione finora

- The Impact of International Financial ReportingDocumento16 pagineThe Impact of International Financial ReportingGadaa TDhNessuna valutazione finora

- Module 3-Financial Statement Presentation: Ifrs Foundation-Supporting Material For The Ifrs For Smes StandardDocumento36 pagineModule 3-Financial Statement Presentation: Ifrs Foundation-Supporting Material For The Ifrs For Smes StandardAlexanderJuarezNessuna valutazione finora

- ANOVA Step by StepDocumento258 pagineANOVA Step by StepVinothNessuna valutazione finora

- M&a ValluationDocumento11 pagineM&a ValluationSumeet BhatereNessuna valutazione finora

- FAR 0 ExercisesDocumento2 pagineFAR 0 ExercisesCASANDRA LascoNessuna valutazione finora

- Internal Audit 3rd CADocumento13 pagineInternal Audit 3rd CAVijaya KumarNessuna valutazione finora

- Course Structure: Semester-IDocumento26 pagineCourse Structure: Semester-IPrince KatiyarNessuna valutazione finora

- Agnes Monica Herman - 130318123 - KP C - Tugas Akl 1 Week 8 PDFDocumento1 paginaAgnes Monica Herman - 130318123 - KP C - Tugas Akl 1 Week 8 PDFAgnes HermanNessuna valutazione finora

- Sponsorship 2nd Provincial ABM Quiz Bee For Public Senior High CaviteDocumento12 pagineSponsorship 2nd Provincial ABM Quiz Bee For Public Senior High CaviteDanna ClaireNessuna valutazione finora

- 1 Quiz ChapterDocumento7 pagine1 Quiz ChapterJoebet DebuyanNessuna valutazione finora

- Chapter 2 Accounting ElementsDocumento40 pagineChapter 2 Accounting ElementsVivek GargNessuna valutazione finora

- Apply Your Knowledge: Case Study 1Documento3 pagineApply Your Knowledge: Case Study 1Queen ValleNessuna valutazione finora

- The Audit Process - Final Work Specific ProblemsDocumento3 pagineThe Audit Process - Final Work Specific ProblemsFazlan Muallif ResnuliusNessuna valutazione finora

- Week 12 SolutionsDocumento7 pagineWeek 12 SolutionsLim Chia RuNessuna valutazione finora

- Mandatory IFRS Adoption and The Effects On SMES in Nigeria: A Study of Selected SMEsDocumento5 pagineMandatory IFRS Adoption and The Effects On SMES in Nigeria: A Study of Selected SMEsInternational Journal of Business Marketing and ManagementNessuna valutazione finora