Potrebbero piacerti anche

- Sample Size for Analytical Surveys, Using a Pretest-Posttest-Comparison-Group DesignDa EverandSample Size for Analytical Surveys, Using a Pretest-Posttest-Comparison-Group DesignNessuna valutazione finora

- Regression Models for Categorical, Count, and Related Variables: An Applied ApproachDa EverandRegression Models for Categorical, Count, and Related Variables: An Applied ApproachNessuna valutazione finora

- SPSS Data Analysis for Univariate, Bivariate, and Multivariate StatisticsDa EverandSPSS Data Analysis for Univariate, Bivariate, and Multivariate StatisticsNessuna valutazione finora

- Introduction To Non Parametric Methods Through R SoftwareDa EverandIntroduction To Non Parametric Methods Through R SoftwareNessuna valutazione finora

- Introduction to Robust Estimation and Hypothesis TestingDa EverandIntroduction to Robust Estimation and Hypothesis TestingNessuna valutazione finora

- Demystifying SPSS It's Not As Complicated As You Might ThinkDocumento67 pagineDemystifying SPSS It's Not As Complicated As You Might ThinkAbubakar UmarNessuna valutazione finora

- 5 Regression AnalysisDocumento43 pagine5 Regression AnalysisAC BalioNessuna valutazione finora

- Factor Analysis Using Spss PDFDocumento2 pagineFactor Analysis Using Spss PDFSpencerNessuna valutazione finora

- Linear Regression and Its Application to EconomicsDa EverandLinear Regression and Its Application to EconomicsNessuna valutazione finora

- Type I and Type II Errors PDFDocumento5 pagineType I and Type II Errors PDFGulfam AnsariNessuna valutazione finora

- Deduction vs. InductionDocumento15 pagineDeduction vs. InductionYen AduanaNessuna valutazione finora

- Structural Equation ModelDocumento46 pagineStructural Equation ModelSarah GracyntiaNessuna valutazione finora

- Module 5 - Ordinal RegressionDocumento55 pagineModule 5 - Ordinal RegressionMy Hanh DoNessuna valutazione finora

- Florida International University: Course Syllabus Application of Quantitative Methods in Business QMB3200-RVAA-RPC-1125Documento10 pagineFlorida International University: Course Syllabus Application of Quantitative Methods in Business QMB3200-RVAA-RPC-1125Lisa VegasNessuna valutazione finora

- Confirmatory Factor Analysis Using Amos, LISREL, MplusDocumento86 pagineConfirmatory Factor Analysis Using Amos, LISREL, Mpluslaveniam100% (1)

- Binomial Logistic Regression Using SPSSDocumento11 pagineBinomial Logistic Regression Using SPSSKhurram ZahidNessuna valutazione finora

- SPSS for Applied Sciences: Basic Statistical TestingDa EverandSPSS for Applied Sciences: Basic Statistical TestingValutazione: 2.5 su 5 stelle2.5/5 (6)

- Choosing The Correct Statistical Test (CHS 627 - University of Alabama)Documento3 pagineChoosing The Correct Statistical Test (CHS 627 - University of Alabama)futulashNessuna valutazione finora

- Sales Predictive Analytics Standard RequirementsDa EverandSales Predictive Analytics Standard RequirementsNessuna valutazione finora

- Wooldridge 2010Documento42 pagineWooldridge 2010iamsbikasNessuna valutazione finora

- Fundamentals of Applied StatisticsDocumento8 pagineFundamentals of Applied StatisticsAam IRNessuna valutazione finora

- Organizational Objectives: IB Business and ManagementDocumento35 pagineOrganizational Objectives: IB Business and Managementapi-529669983Nessuna valutazione finora

- 2003 Makipaa 1Documento15 pagine2003 Makipaa 1faizal rizkiNessuna valutazione finora

- Multiple Linear Regression in Data MiningDocumento14 pagineMultiple Linear Regression in Data Miningakirank1100% (1)

- Research Methodology 2Documento29 pagineResearch Methodology 2sohaibNessuna valutazione finora

- 5682 - 4433 - Factor & Cluster AnalysisDocumento22 pagine5682 - 4433 - Factor & Cluster AnalysisSubrat NandaNessuna valutazione finora

- A Step-by-Step Approach to Using SAS for Factor Analysis and Structural Equation Modeling, Second EditionDa EverandA Step-by-Step Approach to Using SAS for Factor Analysis and Structural Equation Modeling, Second EditionNessuna valutazione finora

- Business Analytics Using SAS Enterprise Guide and SAS Enterprise Miner: A Beginner's GuideDa EverandBusiness Analytics Using SAS Enterprise Guide and SAS Enterprise Miner: A Beginner's GuideNessuna valutazione finora

- STA780 Wk6 Factor Analysis-SPSSDocumento19 pagineSTA780 Wk6 Factor Analysis-SPSSsyaidatul umairahNessuna valutazione finora

- Conjoint analysis Complete Self-Assessment GuideDa EverandConjoint analysis Complete Self-Assessment GuideNessuna valutazione finora

- Business Process Engineering A Complete Guide - 2020 EditionDa EverandBusiness Process Engineering A Complete Guide - 2020 EditionNessuna valutazione finora

- Opportunity Cost A Complete Guide - 2020 EditionDa EverandOpportunity Cost A Complete Guide - 2020 EditionNessuna valutazione finora

- Statistics and Causality: Methods for Applied Empirical ResearchDa EverandStatistics and Causality: Methods for Applied Empirical ResearchWolfgang WiedermannNessuna valutazione finora

- L5 Logistic Regression (2011)Documento55 pagineL5 Logistic Regression (2011)woihon100% (1)

- Data Analysis Using SpssDocumento2 pagineData Analysis Using SpssAnonymous EE5LPEV7100% (1)

- RM NotesDocumento50 pagineRM NotesManu YuviNessuna valutazione finora

- Chap4 Normality (Data Analysis) FVDocumento72 pagineChap4 Normality (Data Analysis) FVryad fki100% (1)

- Introduction to Statistics Through Resampling Methods and RDa EverandIntroduction to Statistics Through Resampling Methods and RNessuna valutazione finora

- NVivo 2 TutorialsDocumento57 pagineNVivo 2 TutorialsRoberto Fabiano FernandesNessuna valutazione finora

- Session 3 - Logistic RegressionDocumento28 pagineSession 3 - Logistic RegressionNausheen Fatima50% (2)

- Applied Linear Regression Models 4th Ed NoteDocumento46 pagineApplied Linear Regression Models 4th Ed Noteken_ng333Nessuna valutazione finora

- Approaches To The Analysis of Survey Data PDFDocumento28 pagineApproaches To The Analysis of Survey Data PDFTarig GibreelNessuna valutazione finora

- Data Visualization, Volume IIDocumento33 pagineData Visualization, Volume IICharleneKronstedtNessuna valutazione finora

- Correlation and RegressionDocumento31 pagineCorrelation and RegressionDela Cruz GenesisNessuna valutazione finora

- Hypothesis Tests: Irwin/Mcgraw-Hill © Andrew F. Siegel, 1997 and 2000Documento27 pagineHypothesis Tests: Irwin/Mcgraw-Hill © Andrew F. Siegel, 1997 and 2000radislamy-1100% (1)

- Midterm GR5412 2019 PDFDocumento2 pagineMidterm GR5412 2019 PDFtinaNessuna valutazione finora

- Data Analysis Using SPSS: Research Workshop SeriesDocumento86 pagineData Analysis Using SPSS: Research Workshop SeriesMuhammad Asad AliNessuna valutazione finora

- Measuement and ScalingDocumento31 pagineMeasuement and Scalingagga1111Nessuna valutazione finora

- Confirmatory Factor AnalysisDocumento38 pagineConfirmatory Factor AnalysisNaqash JuttNessuna valutazione finora

- Econometrics SolutionsDocumento11 pagineEconometrics SolutionsYehudi BaptNessuna valutazione finora

- B-Govt of India Act (1919)Documento2 pagineB-Govt of India Act (1919)fahadraja78Nessuna valutazione finora

- Islamic Civilization and CultureDocumento10 pagineIslamic Civilization and Culturefahadraja78100% (2)

- Lect-10-Concept of Islam-Diff BW Deen and ReligionDocumento13 pagineLect-10-Concept of Islam-Diff BW Deen and Religionfahadraja78100% (3)

- A-Partition of Bengal (1905) PDFDocumento4 pagineA-Partition of Bengal (1905) PDFfahadraja7870% (10)

- Guess For CSS-2018: News AlertDocumento16 pagineGuess For CSS-2018: News Alertfahadraja78Nessuna valutazione finora

- 7-Simon Commission (1927)Documento2 pagine7-Simon Commission (1927)fahadraja7880% (5)

- 6 - Delhi Muslim Proposal - 1927Documento1 pagina6 - Delhi Muslim Proposal - 1927fahadraja7888% (8)

- Climate Change 11 FactsDocumento4 pagineClimate Change 11 Factsfahadraja78Nessuna valutazione finora

- 7-Simon Commission (1927)Documento2 pagine7-Simon Commission (1927)fahadraja7880% (5)

- 8-All Parties Conference (1928) PDFDocumento5 pagine8-All Parties Conference (1928) PDFfahadraja78Nessuna valutazione finora

- 18th Amendment ResearchDocumento36 pagine18th Amendment ResearchUrdu TranslatorrNessuna valutazione finora

- Khilafat Movement PDFDocumento5 pagineKhilafat Movement PDFfahadraja7888% (8)

- Chatlog Css Online Seminar 2017-11-03 22 - 34Documento5 pagineChatlog Css Online Seminar 2017-11-03 22 - 34fahadraja78Nessuna valutazione finora

- ChatLog English 2017 - 11 - 17 10 - 58Documento4 pagineChatLog English 2017 - 11 - 17 10 - 58fahadraja78Nessuna valutazione finora

- ChatLog English 2017 - 11 - 13 11 - 40Documento2 pagineChatLog English 2017 - 11 - 13 11 - 40fahadraja78Nessuna valutazione finora

- All Siae Skus: SF Product Name SIAE Product Code Descrip:on Availability Product Family Unit LIST Price ($)Documento7 pagineAll Siae Skus: SF Product Name SIAE Product Code Descrip:on Availability Product Family Unit LIST Price ($)Emerson Mayon SanchezNessuna valutazione finora

- Yaskawa V7 ManualsDocumento155 pagineYaskawa V7 ManualsAnonymous GbfoQcCNessuna valutazione finora

- INA Over Drive Pulley SystemDocumento1 paginaINA Over Drive Pulley SystemDaniel JulianNessuna valutazione finora

- DR - Rajinikanth - Pharmaceutical ValidationDocumento54 pagineDR - Rajinikanth - Pharmaceutical Validationمحمد عطاNessuna valutazione finora

- Registration Form - Synergies in Communication - 6th Edition - 2017-Drobot AnaDocumento3 pagineRegistration Form - Synergies in Communication - 6th Edition - 2017-Drobot AnaAna IrinaNessuna valutazione finora

- Milestone BillingDocumento3 pagineMilestone BillingJagadeesh Kumar RayuduNessuna valutazione finora

- Some Solutions To Enderton LogicDocumento16 pagineSome Solutions To Enderton LogicJason100% (1)

- KV4BBSR Notice ContractuaL Interview 2023-24Documento9 pagineKV4BBSR Notice ContractuaL Interview 2023-24SuchitaNessuna valutazione finora

- Rubric For Audio Speech DeliveryDocumento2 pagineRubric For Audio Speech DeliveryMarie Sol PanganNessuna valutazione finora

- AM-FM Reception TipsDocumento3 pagineAM-FM Reception TipsKrishna Ghimire100% (1)

- Introduction To Soft Floor CoveringsDocumento13 pagineIntroduction To Soft Floor CoveringsJothi Vel Murugan83% (6)

- Ce Project 1Documento7 pagineCe Project 1emmaNessuna valutazione finora

- Agriculture Vision 2020Documento10 pagineAgriculture Vision 20202113713 PRIYANKANessuna valutazione finora

- ILI9481 DatasheetDocumento143 pagineILI9481 DatasheetdetonatNessuna valutazione finora

- SPWM Vs SVMDocumento11 pagineSPWM Vs SVMpmbalajibtechNessuna valutazione finora

- Do I Need A 1PPS Box For My Mulitbeam SystemDocumento3 pagineDo I Need A 1PPS Box For My Mulitbeam SystemutkuNessuna valutazione finora

- WDP Process Diagrams v1Documento6 pagineWDP Process Diagrams v1Ryan HengNessuna valutazione finora

- Asian Paints Final v1Documento20 pagineAsian Paints Final v1Mukul MundleNessuna valutazione finora

- Normal Consistency of Hydraulic CementDocumento15 pagineNormal Consistency of Hydraulic CementApril Lyn SantosNessuna valutazione finora

- Diagrama Hilux 1KD-2KD PDFDocumento11 pagineDiagrama Hilux 1KD-2KD PDFJeni100% (1)

- Parts List 38 254 13 95: Helical-Bevel Gear Unit KA47, KH47, KV47, KT47, KA47B, KH47B, KV47BDocumento4 pagineParts List 38 254 13 95: Helical-Bevel Gear Unit KA47, KH47, KV47, KT47, KA47B, KH47B, KV47BEdmundo JavierNessuna valutazione finora

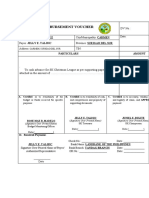

- Disbursement VoucherDocumento7 pagineDisbursement VoucherDan MarkNessuna valutazione finora

- Din 48204Documento3 pagineDin 48204Thanh Dang100% (4)

- ModelsimDocumento47 pagineModelsimKishor KumarNessuna valutazione finora

- TMA GuideDocumento3 pagineTMA GuideHamshavathini YohoratnamNessuna valutazione finora

- Introduction To Templates in C++Documento16 pagineIntroduction To Templates in C++hammarbytpNessuna valutazione finora

- The Ins and Outs Indirect OrvinuDocumento8 pagineThe Ins and Outs Indirect OrvinusatishNessuna valutazione finora

- DocsDocumento4 pagineDocsSwastika SharmaNessuna valutazione finora

- RESUME1Documento2 pagineRESUME1sagar09100% (5)

- Description - GB - 98926286 - Hydro EN-Y 40-250-250 JS-ADL-U3-ADocumento6 pagineDescription - GB - 98926286 - Hydro EN-Y 40-250-250 JS-ADL-U3-AgeorgeNessuna valutazione finora