Potrebbero piacerti anche

- Laporan Keuangan Dan PajakDocumento39 pagineLaporan Keuangan Dan PajakFerry JohNessuna valutazione finora

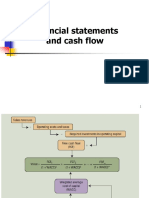

- Chapter 2: Financial Statements and Cash Flow AnalysisDocumento43 pagineChapter 2: Financial Statements and Cash Flow AnalysisshimulNessuna valutazione finora

- Financial Statements, Cash Flow, and TaxesDocumento27 pagineFinancial Statements, Cash Flow, and Taxeszohaib25Nessuna valutazione finora

- Ch02 ShowDocumento44 pagineCh02 ShowardiNessuna valutazione finora

- Financial Statements, Cash Flow, and TaxesDocumento44 pagineFinancial Statements, Cash Flow, and TaxesMahmoud Abdullah100% (1)

- Financial Statements, Cash Flow, and TaxesDocumento45 pagineFinancial Statements, Cash Flow, and TaxesFridolin Belnovando Abditomo PrakosoNessuna valutazione finora

- CH 02 - Financial Stmts Cash Flow and TaxesDocumento32 pagineCH 02 - Financial Stmts Cash Flow and TaxesSyed Mohib Hassan100% (1)

- How Financial Statements Help Evaluate Business Performance and Increase ValueDocumento61 pagineHow Financial Statements Help Evaluate Business Performance and Increase ValueNelson Ivan Acosta100% (1)

- Chapter 03Documento29 pagineChapter 03andi.w.rahardjoNessuna valutazione finora

- Financial Reports Explained: Balance Sheets, Income Statements & Cash FlowDocumento30 pagineFinancial Reports Explained: Balance Sheets, Income Statements & Cash FlowAffan AhmedNessuna valutazione finora

- Financial Statements, Cash Flow, and TaxesDocumento36 pagineFinancial Statements, Cash Flow, and TaxesHussainNessuna valutazione finora

- Financial Statements Reveal Company's Declining Cash FlowsDocumento19 pagineFinancial Statements Reveal Company's Declining Cash FlowsAiqa AliNessuna valutazione finora

- Accounting For Financial ManagementDocumento42 pagineAccounting For Financial ManagementTIDURLANessuna valutazione finora

- Clase 1 Casos en Finanzas UDDDocumento35 pagineClase 1 Casos en Finanzas UDDJuan Gallegos M.Nessuna valutazione finora

- Investment VI FINC 404 Company ValuationDocumento52 pagineInvestment VI FINC 404 Company ValuationMohamed MadyNessuna valutazione finora

- Financial Statements, Cash Flow, and TaxesDocumento8 pagineFinancial Statements, Cash Flow, and TaxesRaihan Eibna RezaNessuna valutazione finora

- Ventura, Mary Mickaella R Chapter 4 - MinicaseDocumento5 pagineVentura, Mary Mickaella R Chapter 4 - MinicaseMary Ventura100% (1)

- FINANCIAL ANALYSIS OF S&S AIRDocumento4 pagineFINANCIAL ANALYSIS OF S&S AIRSarwanti PurwandariNessuna valutazione finora

- CH4 MinicaseDocumento4 pagineCH4 Minicasemervin coquillaNessuna valutazione finora

- Course Code: Fn-550Documento25 pagineCourse Code: Fn-550shoaibraza110Nessuna valutazione finora

- Solution Manual For Fundamentals of Corporate Finance Canadian Canadian 8Th Edition by Ross Isbn 0071051600 9780071051606 Full Chapter PDFDocumento35 pagineSolution Manual For Fundamentals of Corporate Finance Canadian Canadian 8Th Edition by Ross Isbn 0071051600 9780071051606 Full Chapter PDFnancy.rodriguez985100% (10)

- Concepts Review and Critical Thinking Questions 4Documento6 pagineConcepts Review and Critical Thinking Questions 4fnrbhcNessuna valutazione finora

- Contemporary Financial Management 10th Edition Moyer Solutions Manual 1Documento15 pagineContemporary Financial Management 10th Edition Moyer Solutions Manual 1carlo100% (38)

- Solution Manual For Fundamentals of Corporate Finance 10Th Edition by Ross Westerfield Jordan Isbn 0078034639 9780078034633 Full Chapter PDFDocumento33 pagineSolution Manual For Fundamentals of Corporate Finance 10Th Edition by Ross Westerfield Jordan Isbn 0078034639 9780078034633 Full Chapter PDFjudy.pierce330100% (12)

- EFM2e, CH 02, SlidesDocumento19 pagineEFM2e, CH 02, SlidesEricLiangtoNessuna valutazione finora

- BT-Chap 2Documento11 pagineBT-Chap 2Diệu Quỳnh100% (1)

- Financial Statements, Cash Flow, and TaxesDocumento44 pagineFinancial Statements, Cash Flow, and TaxesreNessuna valutazione finora

- Accounting For Financial ManagementDocumento54 pagineAccounting For Financial ManagementEric RomeroNessuna valutazione finora

- Pert. Ke 3. Analisa Kinerja KeuanganDocumento25 paginePert. Ke 3. Analisa Kinerja KeuanganYULIANTONessuna valutazione finora

- Understanding Financial StatementsDocumento46 pagineUnderstanding Financial StatementsgulafshanNessuna valutazione finora

- Untitled DocumentDocumento6 pagineUntitled DocumentAman SinghNessuna valutazione finora

- Financial Statements, Cash Flow and TaxesDocumento44 pagineFinancial Statements, Cash Flow and TaxesAli JumaniNessuna valutazione finora

- CF MBA S23 Ch2 (B2) QsDocumento6 pagineCF MBA S23 Ch2 (B2) QsWaris 3478-FBAS/BSCS/F16Nessuna valutazione finora

- Case 1Documento5 pagineCase 1noor memekNessuna valutazione finora

- Analysis of Financial Statements RatiosDocumento9 pagineAnalysis of Financial Statements RatiosViren DeshpandeNessuna valutazione finora

- FIN220 Tutorial Chapter 2Documento37 pagineFIN220 Tutorial Chapter 2saifNessuna valutazione finora

- Chapter 03 PenDocumento27 pagineChapter 03 PenJeffreyDavidNessuna valutazione finora

- Case 1 New Signal Cable CompanyDocumento6 pagineCase 1 New Signal Cable Companymilk teaNessuna valutazione finora

- Financial Planning and Forecasting Financial StatementsDocumento70 pagineFinancial Planning and Forecasting Financial StatementsAziz Hotelwala100% (1)

- Corporate Finance 3rd Edition Graham Solution ManualDocumento15 pagineCorporate Finance 3rd Edition Graham Solution ManualMark PanchitoNessuna valutazione finora

- Financial Statements, Cash Flow, and TaxesDocumento8 pagineFinancial Statements, Cash Flow, and TaxesAdwa Al-NaimNessuna valutazione finora

- Answers: Operating Income Changes in Net Operating AssetsDocumento6 pagineAnswers: Operating Income Changes in Net Operating AssetsNawarathna KumariNessuna valutazione finora

- Financial Statements, Cash Flow, and TaxesDocumento29 pagineFinancial Statements, Cash Flow, and TaxesHooriaKhanNessuna valutazione finora

- Case Solutions CH (1-8) II PDFDocumento21 pagineCase Solutions CH (1-8) II PDFMajed MansourNessuna valutazione finora

- Financial Management Accounting InsightsDocumento11 pagineFinancial Management Accounting InsightsHannahPojaFeria50% (2)

- 1st Case Study - Financial Statement AnalysisDocumento6 pagine1st Case Study - Financial Statement AnalysisKimberly SoqueNessuna valutazione finora

- MBA CorporateDocumento4 pagineMBA CorporateJohn BiliNessuna valutazione finora

- Solution Manual For Fundamentals of Corporate Finance Canadian 9th Edition by Ross ISBN 1259087581 9781259087585Documento36 pagineSolution Manual For Fundamentals of Corporate Finance Canadian 9th Edition by Ross ISBN 1259087581 9781259087585lauriedavisqdnxfetycj100% (24)

- Financial Statements, Cash Flow, and TaxesDocumento23 pagineFinancial Statements, Cash Flow, and TaxesSaad KhanNessuna valutazione finora

- Accounting Statements, Taxes, and Cash Flow: Answers To Concepts Review and Critical Thinking Questions 1Documento15 pagineAccounting Statements, Taxes, and Cash Flow: Answers To Concepts Review and Critical Thinking Questions 1RabinNessuna valutazione finora

- Chapter 2Documento40 pagineChapter 2Nisreen Al-shareNessuna valutazione finora

- Mini CaseDocumento7 pagineMini CaseHarrisha Arumugam0% (1)

- Solution Manual For Fundamentals of Corporate Finance Canadian Canadian 8th Edition by Ross ISBN 0071051600 9780071051606Documento36 pagineSolution Manual For Fundamentals of Corporate Finance Canadian Canadian 8th Edition by Ross ISBN 0071051600 9780071051606lauriedavisqdnxfetycj100% (27)

- Practice Solution 2Documento4 paginePractice Solution 2Luigi NocitaNessuna valutazione finora

- Answer KeyDocumento52 pagineAnswer KeyDevonNessuna valutazione finora

- HorngrenIMA14eSM ch16Documento53 pagineHorngrenIMA14eSM ch16Piyal HossainNessuna valutazione finora

- Solution For The Analysis and Use of Financial Statements White G ch03Documento48 pagineSolution For The Analysis and Use of Financial Statements White G ch03twinkle goyalNessuna valutazione finora

- Finance for IT Decision Makers: A practical handbookDa EverandFinance for IT Decision Makers: A practical handbookNessuna valutazione finora

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineDa EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNessuna valutazione finora

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryDa EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNessuna valutazione finora

- Afrina Deswita PDFDocumento1 paginaAfrina Deswita PDFpurnamaNessuna valutazione finora

- Afrina DeswitaDocumento1 paginaAfrina DeswitapurnamaNessuna valutazione finora

- Agency Theory ExplainedDocumento20 pagineAgency Theory Explainedfredy hary purwantoNessuna valutazione finora

- Agency Theory ExplainedDocumento20 pagineAgency Theory Explainedfredy hary purwantoNessuna valutazione finora

- Agency Theory ExplainedDocumento20 pagineAgency Theory Explainedfredy hary purwantoNessuna valutazione finora

- DIY Investor's Guide to Profitable PortfoliosDocumento66 pagineDIY Investor's Guide to Profitable Portfoliosdabster7000Nessuna valutazione finora

- Intermediate Accounting: Statement of Cash FlowsDocumento70 pagineIntermediate Accounting: Statement of Cash Flows12C1 LớpNessuna valutazione finora

- Classification and Types of CorporationsDocumento22 pagineClassification and Types of Corporationsevlyn aplacaNessuna valutazione finora

- Raymond Corporate GovernanceDocumento10 pagineRaymond Corporate GovernanceFoRam KapzNessuna valutazione finora

- Basics of InvestmentDocumento19 pagineBasics of InvestmentJohn DawsonNessuna valutazione finora

- Valuation of Inventories: Dangal QuestionsDocumento28 pagineValuation of Inventories: Dangal Questionsmonudeep aggarwalNessuna valutazione finora

- The Cost of CapitalDocumento23 pagineThe Cost of CapitalMuhammad AmmadNessuna valutazione finora

- How Does PC Impact On Firm PDFDocumento3 pagineHow Does PC Impact On Firm PDFRabia NajafNessuna valutazione finora

- ContinueDocumento2 pagineContinueLove RaiNessuna valutazione finora

- Inventory Management TechniquesDocumento11 pagineInventory Management TechniquesSamarth PachhapurNessuna valutazione finora

- SC upholds nullity of mortgage without HLURB approvalDocumento44 pagineSC upholds nullity of mortgage without HLURB approvalLouie100% (3)

- Money MarketDocumento19 pagineMoney Marketramesh.kNessuna valutazione finora

- Understanding Derivatives RisksDocumento18 pagineUnderstanding Derivatives RisksMayank ChaturvediNessuna valutazione finora

- CEMCO Holdings Vs National Life Insurance CoDocumento1 paginaCEMCO Holdings Vs National Life Insurance CoCE SherNessuna valutazione finora

- CV English NVDDocumento5 pagineCV English NVDapi-19969643Nessuna valutazione finora

- FM 09-10 Financial Statement AnalysisDocumento4 pagineFM 09-10 Financial Statement AnalysisRohit GuptaNessuna valutazione finora

- UntitledDocumento6 pagineUntitledMuhammad AbdullahNessuna valutazione finora

- ResearchServices BrochureDocumento14 pagineResearchServices BrochureSaeedArshadiNessuna valutazione finora

- NipponIndia ETF 5 Year GiltDocumento28 pagineNipponIndia ETF 5 Year GiltshashanksaranNessuna valutazione finora

- George Angell, Barry Haigh-West of Wall Street - Understanding The Futures Market, Trading Strategies, Winning The Game-Longman Financial Service (1987)Documento220 pagineGeorge Angell, Barry Haigh-West of Wall Street - Understanding The Futures Market, Trading Strategies, Winning The Game-Longman Financial Service (1987)Yago Oliveira100% (1)

- HNGIL CorpPresentation12Documento28 pagineHNGIL CorpPresentation12Nazlı KarabıyıkoğluNessuna valutazione finora

- Return and Risk From All Investment DecisionsDocumento4 pagineReturn and Risk From All Investment DecisionsAchmad ArdanuNessuna valutazione finora

- Appraoches To Valuation 1Documento67 pagineAppraoches To Valuation 1tj00007Nessuna valutazione finora

- 1: Introduction To Financial MarketsDocumento18 pagine1: Introduction To Financial Marketsshiko tharwatNessuna valutazione finora

- Accountability, Responsibility and Corporate GovernanceDocumento64 pagineAccountability, Responsibility and Corporate GovernanceNeha VermaNessuna valutazione finora

- ExpediaDocumento48 pagineExpediaDonaNessuna valutazione finora

- Employee Motivation Techniques at AnmazonDocumento8 pagineEmployee Motivation Techniques at Anmazonitzgauravsingh7Nessuna valutazione finora

- CE40 - E01 Assignment 1 - Interest and Economic EquivalenceDocumento2 pagineCE40 - E01 Assignment 1 - Interest and Economic EquivalenceAlexandra BanteguiNessuna valutazione finora

- Annual Report 2019 PT Berlina TBKDocumento292 pagineAnnual Report 2019 PT Berlina TBKSella YunitaNessuna valutazione finora

- The Ultimate Guide: Plan BDocumento21 pagineThe Ultimate Guide: Plan BIbukunNessuna valutazione finora