Potrebbero piacerti anche

- Digital Marketing Planning, Budgeting, ForecastingDocumento51 pagineDigital Marketing Planning, Budgeting, ForecastingJinny AsyiqinNessuna valutazione finora

- Managerial AccountingDocumento149 pagineManagerial AccountingLeojelaineIgcoyNessuna valutazione finora

- Business PlanDocumento29 pagineBusiness PlanHarsh Gupta100% (1)

- Bomber JacketDocumento3 pagineBomber JacketLaura Carrascosa FusterNessuna valutazione finora

- Work StudyDocumento218 pagineWork Studycitizen_anuNessuna valutazione finora

- 65 ActsDocumento178 pagine65 ActsComprachosNessuna valutazione finora

- Case Study (Co2 Flooding)Documento10 pagineCase Study (Co2 Flooding)Jessica KingNessuna valutazione finora

- Estimating and CostingDocumento135 pagineEstimating and CostingShamim AkhtarNessuna valutazione finora

- ProductivityDocumento138 pagineProductivityRui OasayNessuna valutazione finora

- Feasibility-Travel AgencyDocumento35 pagineFeasibility-Travel AgencyJelly Anne79% (14)

- Wip PDFDocumento29 pagineWip PDFEruNessuna valutazione finora

- BRASS Introduction 2012Documento23 pagineBRASS Introduction 20121234scr5678Nessuna valutazione finora

- Third Quarter Pre-Test Mathematics 7 Directions: RDocumento4 pagineThird Quarter Pre-Test Mathematics 7 Directions: RAhron RivasNessuna valutazione finora

- South Valley University Faculty of Science Geology Department Dr. Mohamed Youssef AliDocumento29 pagineSouth Valley University Faculty of Science Geology Department Dr. Mohamed Youssef AliHari Dante Cry100% (1)

- Fibre Science and TechnologyDocumento142 pagineFibre Science and TechnologyPARAMASIVAM SNessuna valutazione finora

- Planning Business VentureDocumento10 paginePlanning Business VentureOm PrasadNessuna valutazione finora

- Export Oriented Units and KaizenDocumento15 pagineExport Oriented Units and Kaizenharini1995Nessuna valutazione finora

- Entrep Chapter 6, 4MSDocumento15 pagineEntrep Chapter 6, 4MSJacel GadonNessuna valutazione finora

- Productivity: Productivity Is An Average Measure ofDocumento35 pagineProductivity: Productivity Is An Average Measure ofshivani.cs1995Nessuna valutazione finora

- Bill Rate:: ChargeabilityDocumento9 pagineBill Rate:: ChargeabilityNivesh Anand AroraNessuna valutazione finora

- EXIM POLICY 2009-2014: Also Called Foreign Trade Policy 2009-2014Documento11 pagineEXIM POLICY 2009-2014: Also Called Foreign Trade Policy 2009-2014Shrikant KulkarniNessuna valutazione finora

- Microeconomics: Module 7: Production and CostsDocumento31 pagineMicroeconomics: Module 7: Production and CostsErica Auriell FadilaNessuna valutazione finora

- Instructor: Ovais VOHRA Ovaisvohra@aydin - Edu.tr Note 08 2021Documento28 pagineInstructor: Ovais VOHRA Ovaisvohra@aydin - Edu.tr Note 08 2021iremNessuna valutazione finora

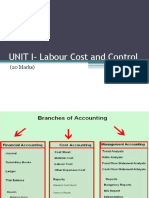

- Labour Cost and ControlDocumento65 pagineLabour Cost and Controlaishwarya raikarNessuna valutazione finora

- Purchase of Capital GoodsDocumento17 paginePurchase of Capital Goodsaarti HingeNessuna valutazione finora

- Topic 7Documento23 pagineTopic 7AB RomillaNessuna valutazione finora

- Small Scale Industrial Undertakings NewDocumento29 pagineSmall Scale Industrial Undertakings NewMohit AgrawalNessuna valutazione finora

- Unit 5 Business PlanDocumento27 pagineUnit 5 Business PlanaKSHAT sHARMANessuna valutazione finora

- PT 3 AccountingDocumento19 paginePT 3 AccountingYzzabel Denise L. TolentinoNessuna valutazione finora

- Small Scale Industries (Ssi) - ShortDocumento22 pagineSmall Scale Industries (Ssi) - ShortAadil KakarNessuna valutazione finora

- Production and Cost Analysis of Beverage IndustryDocumento12 pagineProduction and Cost Analysis of Beverage IndustryGautam BindlishNessuna valutazione finora

- Cost AcctngDocumento22 pagineCost AcctngJINKY TOLENTINONessuna valutazione finora

- Sitxfin004 VactsDocumento34 pagineSitxfin004 VactsNaween WageeshaNessuna valutazione finora

- Financial RequirementDocumento12 pagineFinancial RequirementK Pavan KumarNessuna valutazione finora

- Prac Docs CMG Section 1Documento32 paginePrac Docs CMG Section 1Tadala Paul MaluwaNessuna valutazione finora

- Eou ManualDocumento3 pagineEou ManualastuteNessuna valutazione finora

- MNC and OutsourcingDocumento52 pagineMNC and OutsourcingsudeendraNessuna valutazione finora

- Business Plan Preparation: Entrepreneurship DevelopmentDocumento17 pagineBusiness Plan Preparation: Entrepreneurship DevelopmentAbijith K SNessuna valutazione finora

- Export Assistance, Import Facility, Tax Concessions and Duty DrawbacksDocumento67 pagineExport Assistance, Import Facility, Tax Concessions and Duty Drawbacksmayankgoyal333Nessuna valutazione finora

- Da-3 VaibhavDocumento6 pagineDa-3 VaibhavVAIBHAV BARDHANNessuna valutazione finora

- Chapter 7: Controlling Expense: 7.1. The Budget ProcessDocumento49 pagineChapter 7: Controlling Expense: 7.1. The Budget ProcessmosisawoldeNessuna valutazione finora

- Site IonDocumento19 pagineSite IonRamesh ChoudharyNessuna valutazione finora

- Session 8 Calulating COST 2Documento33 pagineSession 8 Calulating COST 2AlokKumarNessuna valutazione finora

- Export IncentivesDocumento42 pagineExport Incentivespriya2210Nessuna valutazione finora

- Technical Studies 2019-1 V2Documento4 pagineTechnical Studies 2019-1 V2J DNessuna valutazione finora

- On Presston Engineering CorporationDocumento21 pagineOn Presston Engineering CorporationPreethi Pavana100% (1)

- Chapter 2Documento22 pagineChapter 2mohamed adanNessuna valutazione finora

- Mod 4Documento39 pagineMod 4Muhd Shabeeb ANessuna valutazione finora

- Cost A C NotesDocumento41 pagineCost A C NotesM sai chandra Shiva kumarNessuna valutazione finora

- Perform Financial CalculationsDocumento46 paginePerform Financial Calculationsnigus89% (9)

- EXIM Policy & Capital Account ConvertibilityDocumento21 pagineEXIM Policy & Capital Account Convertibilityankurgarg86Nessuna valutazione finora

- Operating Budgets: Bridging Planning and ControlDocumento10 pagineOperating Budgets: Bridging Planning and ControlalomeloNessuna valutazione finora

- Budgetary Control: Resource PersonDocumento72 pagineBudgetary Control: Resource PersonjainmohitpvtltdNessuna valutazione finora

- CL3 Business EnvironmentDocumento32 pagineCL3 Business EnvironmentAshwin RNessuna valutazione finora

- International Business 3Documento45 pagineInternational Business 3Ken TuazonNessuna valutazione finora

- International Financial Management 1219993582593066 8Documento41 pagineInternational Financial Management 1219993582593066 8sachinNessuna valutazione finora

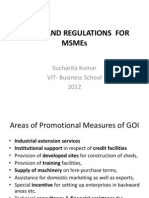

- Policy and Regulations For MsmesDocumento13 paginePolicy and Regulations For MsmesNithin KannanNessuna valutazione finora

- Portfolio Activity Unit 5 University of The PeopleDocumento5 paginePortfolio Activity Unit 5 University of The Peoplechristian allosNessuna valutazione finora

- Unit 4Documento65 pagineUnit 4Rohit Kumar MahatoNessuna valutazione finora

- Unit 4 5 Cse332Documento91 pagineUnit 4 5 Cse332Dharmendra TripathiNessuna valutazione finora

- 11 Production Cost Short-RunDocumento42 pagine11 Production Cost Short-RunHemachandra M mm21b029Nessuna valutazione finora

- Cost ConceptsDocumento16 pagineCost ConceptsValarmathy SankaralingamNessuna valutazione finora

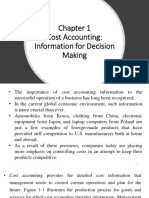

- Chapter 1Documento44 pagineChapter 1fyfyg411Nessuna valutazione finora

- Leveraging on India: Best Practices Related to Manufacturing, Engineering, and ItDa EverandLeveraging on India: Best Practices Related to Manufacturing, Engineering, and ItNessuna valutazione finora

- Unit - 2 Policies - Importance, Types and Policy FormulationDocumento16 pagineUnit - 2 Policies - Importance, Types and Policy FormulationPARAMASIVAM SNessuna valutazione finora

- Unit - 1 Evolution of Management ThoughtDocumento76 pagineUnit - 1 Evolution of Management ThoughtPARAMASIVAM SNessuna valutazione finora

- Unit - 2 Forecasting and Decision MakingDocumento35 pagineUnit - 2 Forecasting and Decision MakingPARAMASIVAM SNessuna valutazione finora

- Mechanics of Textile Machinery ContentDocumento59 pagineMechanics of Textile Machinery ContentPARAMASIVAM SNessuna valutazione finora

- Care Labelling of ApprelsDocumento3 pagineCare Labelling of ApprelsPARAMASIVAM SNessuna valutazione finora

- Facilities Available For ExportersDocumento21 pagineFacilities Available For ExportersPARAMASIVAM SNessuna valutazione finora

- Manual de Electronica HardbookDocumento970 pagineManual de Electronica HardbookninoferNessuna valutazione finora

- E Numbers Are Number Codes ForDocumento3 pagineE Numbers Are Number Codes ForaradhyaNessuna valutazione finora

- NDT Matrix 12-99-90-1710 - Rev.2 PDFDocumento2 pagineNDT Matrix 12-99-90-1710 - Rev.2 PDFEPC NCCNessuna valutazione finora

- Air System Sizing Summary For NIVEL PB - Zona 1Documento1 paginaAir System Sizing Summary For NIVEL PB - Zona 1Roger PandoNessuna valutazione finora

- Greek ArchitectureDocumento16 pagineGreek ArchitectureXlyth RodriguezNessuna valutazione finora

- Mid Lesson 1 Ethics & Moral PhiloDocumento13 pagineMid Lesson 1 Ethics & Moral PhiloKate EvangelistaNessuna valutazione finora

- Thesis Brand BlanketDocumento4 pagineThesis Brand BlanketKayla Smith100% (2)

- Need For Advanced Suspension SystemsDocumento10 pagineNeed For Advanced Suspension SystemsIQPC GmbHNessuna valutazione finora

- Unemployment in IndiaDocumento9 pagineUnemployment in IndiaKhushiNessuna valutazione finora

- ForewordDocumento96 pagineForewordkkcmNessuna valutazione finora

- Initiation in Pre-Tantrasamuccaya Kerala Tantric Literature PDFDocumento24 pagineInitiation in Pre-Tantrasamuccaya Kerala Tantric Literature PDFVenkateswaran NarayananNessuna valutazione finora

- Knowledge /28 Application / 22 Thinking / 12 Communication / 9Documento8 pagineKnowledge /28 Application / 22 Thinking / 12 Communication / 9NmNessuna valutazione finora

- American Pile Driving Equipment Equipment CatalogDocumento25 pagineAmerican Pile Driving Equipment Equipment CatalogW Morales100% (1)

- PT4115EDocumento18 paginePT4115Edragom2Nessuna valutazione finora

- Course On Quantum ComputingDocumento235 pagineCourse On Quantum ComputingAram ShojaeiNessuna valutazione finora

- Solids Separation Study Guide: Wisconsin Department of Natural Resources Wastewater Operator CertificationDocumento44 pagineSolids Separation Study Guide: Wisconsin Department of Natural Resources Wastewater Operator CertificationkharismaaakNessuna valutazione finora

- The Gingerbread Man-1 EnglishareDocumento40 pagineThe Gingerbread Man-1 EnglishareamayalibelulaNessuna valutazione finora

- 11 - Morphology AlgorithmsDocumento60 pagine11 - Morphology AlgorithmsFahad MattooNessuna valutazione finora

- Pelton2014 Para-Equilibrium Phase DiagramsDocumento7 paginePelton2014 Para-Equilibrium Phase DiagramsAbraham Becerra AranedaNessuna valutazione finora

- TXN Alarms 18022014Documento12 pagineTXN Alarms 18022014Sid GrgNessuna valutazione finora

- 4th Semester Electrical Engg.Documento19 pagine4th Semester Electrical Engg.Bhojpuri entertainmentNessuna valutazione finora

- Anchor Chart-Describing Words-Descriptive Details of Setting and Character PDFDocumento2 pagineAnchor Chart-Describing Words-Descriptive Details of Setting and Character PDFdellindiaNessuna valutazione finora

- 114 The Letter S: M 'TafontDocumento9 pagine114 The Letter S: M 'TafontHarry TLNessuna valutazione finora

- Qa/Qc Mechanical Monthly Progress Report For June 2015: Area/System Description Status RemarksDocumento1 paginaQa/Qc Mechanical Monthly Progress Report For June 2015: Area/System Description Status RemarksRen SalazarNessuna valutazione finora