Potrebbero piacerti anche

- California Apostille Authentication FormDocumento1 paginaCalifornia Apostille Authentication FormCalifornia Apostille0% (8)

- Adjusting Entries - Sample Problem With AnswerDocumento19 pagineAdjusting Entries - Sample Problem With AnswerMaDine 19100% (3)

- Sol. Man. - Chapter 8 - Adjusting EntriesDocumento11 pagineSol. Man. - Chapter 8 - Adjusting EntriesPerdito John Vin100% (3)

- Collateral Debt ObligationsDocumento7 pagineCollateral Debt Obligationsashwani08Nessuna valutazione finora

- Loans Receivable Practice (Review)Documento6 pagineLoans Receivable Practice (Review)Deviline MichelleNessuna valutazione finora

- Week 7-9Documento28 pagineWeek 7-9Sohaib IrfanNessuna valutazione finora

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionDa EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNessuna valutazione finora

- Ch.2 - Basic Concept of MacroeconomicsDocumento24 pagineCh.2 - Basic Concept of MacroeconomicsMayank MallNessuna valutazione finora

- Defining Leg Vs Base Candle: Leg-Base Isolation Method For Buy Zones and Sell ZonesDocumento7 pagineDefining Leg Vs Base Candle: Leg-Base Isolation Method For Buy Zones and Sell Zonesrnumesh1Nessuna valutazione finora

- Sol. Man. - Chapter 8 - Adjusting Entries PDFDocumento11 pagineSol. Man. - Chapter 8 - Adjusting Entries PDFPerdito John VinNessuna valutazione finora

- Midterm Exam-Adjusting EntriesDocumento5 pagineMidterm Exam-Adjusting EntriesHassanhor Guro BacolodNessuna valutazione finora

- INTERMEDIATE ACCOUNTING 1 ReviewDocumento57 pagineINTERMEDIATE ACCOUNTING 1 ReviewStefanie Fermin100% (1)

- Provisions, Contingencies and Other Liabilities ProblemsDocumento7 pagineProvisions, Contingencies and Other Liabilities ProblemsGiander100% (1)

- Introduction: Inventory of Learner'S Biography Purposive CommunicationDocumento3 pagineIntroduction: Inventory of Learner'S Biography Purposive CommunicationHesham Am-Li100% (1)

- Activity 7 Adjusting Entries and Accounting PolicyDocumento6 pagineActivity 7 Adjusting Entries and Accounting PolicyBlesh Macusi67% (3)

- Adjusting Entries: Impairment Loss of ReceivablesDocumento16 pagineAdjusting Entries: Impairment Loss of ReceivablesL Onifur100% (1)

- Far ReviewerDocumento9 pagineFar ReviewerKathlen PilarNessuna valutazione finora

- AdjustmentsDocumento18 pagineAdjustmentsIca MontanoNessuna valutazione finora

- Performed 5000 Worth of Service For A Customer On Account: AccrualDocumento10 paginePerformed 5000 Worth of Service For A Customer On Account: AccrualShin Shan JeonNessuna valutazione finora

- Adjusting EntriesDocumento14 pagineAdjusting Entriesmhrzyn27Nessuna valutazione finora

- DDA 1 Niaga C Materials - 4th MeetingDocumento32 pagineDDA 1 Niaga C Materials - 4th MeetingZenalina Hadi PutriNessuna valutazione finora

- Assignment#1Documento4 pagineAssignment#1Kristine Esplana ToraldeNessuna valutazione finora

- (Module 4) ProblemsDocumento6 pagine(Module 4) ProblemsYanie Dela Cruz100% (1)

- Adjustment Process NotesDocumento4 pagineAdjustment Process NotesMa. Clovel MosasoNessuna valutazione finora

- Adjustment Process NotesDocumento6 pagineAdjustment Process NotesNicole ElaineNessuna valutazione finora

- IA2 Quiz1 (ANTIDO)Documento4 pagineIA2 Quiz1 (ANTIDO)Claire Magbunag AntidoNessuna valutazione finora

- Adjusting Entries Discussion and SolutionDocumento6 pagineAdjusting Entries Discussion and SolutionGarp BarrocaNessuna valutazione finora

- Adjusting Entry1 - AnswerDocumento9 pagineAdjusting Entry1 - AnswerReighjon Ashley C. Tolentino100% (1)

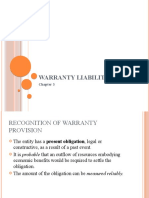

- Ch3Warranty LiabilityDocumento24 pagineCh3Warranty LiabilityCrysta LeeNessuna valutazione finora

- Lagrimas, Sarah Nicole S. - Provisions, Contingencies & Other Liabilities PDFDocumento3 pagineLagrimas, Sarah Nicole S. - Provisions, Contingencies & Other Liabilities PDFSarah Nicole S. LagrimasNessuna valutazione finora

- Mod3 Part 3Documento12 pagineMod3 Part 3viaishere4uNessuna valutazione finora

- Frias Activity 6Documento6 pagineFrias Activity 6Lars FriasNessuna valutazione finora

- Toaz - Info Adjusting Journal Entries Exercises3xlsx PRDocumento22 pagineToaz - Info Adjusting Journal Entries Exercises3xlsx PRpau mejaresNessuna valutazione finora

- University of Luzon College of Accountancy Adjusting EntriesDocumento91 pagineUniversity of Luzon College of Accountancy Adjusting EntriestaurusNessuna valutazione finora

- Adjusting Entry - AnswerDocumento8 pagineAdjusting Entry - AnswerReighjon Ashley C. TolentinoNessuna valutazione finora

- Answer Key - Quizzer On AJEDocumento2 pagineAnswer Key - Quizzer On AJEClarissa De GuzmanNessuna valutazione finora

- Chapter 1 - Contingent LiabilitiesDocumento6 pagineChapter 1 - Contingent LiabilitiesJoshua AbanalesNessuna valutazione finora

- CH 3 Vol 1 AnswersDocumento17 pagineCH 3 Vol 1 Answersjayjay112275% (4)

- Sheet (4) First Year PDFDocumento9 pagineSheet (4) First Year PDFmagdy kamelNessuna valutazione finora

- Inventories (PROBLEM 10-6) : Allyna Rose V. Ojera BSA-2ADocumento18 pagineInventories (PROBLEM 10-6) : Allyna Rose V. Ojera BSA-2AOJERA, Allyna Rose V. BSA-1BNessuna valutazione finora

- Assignment AnswerDocumento7 pagineAssignment AnswerTemesgenNessuna valutazione finora

- Model Ans - Sas - I April 2018Documento68 pagineModel Ans - Sas - I April 2018প্রীতম সেনNessuna valutazione finora

- Advanced 1Documento90 pagineAdvanced 1NhicoleChoiNessuna valutazione finora

- Sol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aDocumento7 pagineSol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aYamateNessuna valutazione finora

- 10 Date Debit Credit Adjusting Entries ParticularsDocumento1 pagina10 Date Debit Credit Adjusting Entries ParticularsJean Dela CruzNessuna valutazione finora

- Discussion Problems and SolutionsDocumento33 pagineDiscussion Problems and SolutionsBella De LiañoNessuna valutazione finora

- A - MC 10 - Stu (Answer)Documento2 pagineA - MC 10 - Stu (Answer)syafiqahzinNessuna valutazione finora

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDocumento7 pagineSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

- 1 2021 FAR FinalsDocumento6 pagine1 2021 FAR FinalsZatsumono YamamotoNessuna valutazione finora

- Practice Set Review - Current LiabilitiesDocumento12 paginePractice Set Review - Current LiabilitiesKayla MirandaNessuna valutazione finora

- Ch2Premium LiabilityDocumento20 pagineCh2Premium LiabilityCrysta Lee100% (1)

- Reyes Solution Adjusting EntryDocumento4 pagineReyes Solution Adjusting EntryJustine ReyesNessuna valutazione finora

- AUDCIS Problems PrelimDocumento16 pagineAUDCIS Problems PrelimLian GarlNessuna valutazione finora

- Q.3-Question and SolutionDocumento4 pagineQ.3-Question and SolutionFIROZ KHANNessuna valutazione finora

- 4.2 Answers and Solutions - Assignment On Materials and LaborDocumento8 pagine4.2 Answers and Solutions - Assignment On Materials and LaborRoselyn LumbaoNessuna valutazione finora

- ADJUSTING ENTRIES NotesDocumento6 pagineADJUSTING ENTRIES NotesDE GUZMAN Cristian MarlonNessuna valutazione finora

- Intacc 3 Ans To Chap 1 ProbsDocumento4 pagineIntacc 3 Ans To Chap 1 ProbsMhico MateoNessuna valutazione finora

- Aud - PracDocumento2 pagineAud - PracSadist AngelNessuna valutazione finora

- Chapter - 6 Accounting Equations-FinalDocumento12 pagineChapter - 6 Accounting Equations-FinalKyra ManchandaNessuna valutazione finora

- Test 1 (2019672728) (NBF2D)Documento5 pagineTest 1 (2019672728) (NBF2D)Masnur Aina Md RajehNessuna valutazione finora

- Jawaban Lab Pengantar AkuntansiDocumento71 pagineJawaban Lab Pengantar AkuntansiWida Nurul AeniNessuna valutazione finora

- 2.1, 2.2, 2.3, 2.4, 2.9, 2.10, 2.12 KTQTDocumento6 pagine2.1, 2.2, 2.3, 2.4, 2.9, 2.10, 2.12 KTQTThùy LinhhNessuna valutazione finora

- Adjusting-Entries ConceptDocumento7 pagineAdjusting-Entries ConceptLori100% (1)

- Module 2 - Merchandising Concern-Completing The Accounting CycleDocumento26 pagineModule 2 - Merchandising Concern-Completing The Accounting Cycledimolangalam5Nessuna valutazione finora

- FSA ExercisesDocumento23 pagineFSA ExercisesBel NochuNessuna valutazione finora

- Accounting For A Service Business: Review ProblemsDocumento23 pagineAccounting For A Service Business: Review ProblemsHesham Am-LiNessuna valutazione finora

- Merchandising ADocumento2 pagineMerchandising AHesham Am-LiNessuna valutazione finora

- From Speech Community (SC) To Shared Patterns and Codes: Purposive Communication General Education TrainingDocumento18 pagineFrom Speech Community (SC) To Shared Patterns and Codes: Purposive Communication General Education TrainingHesham Am-LiNessuna valutazione finora

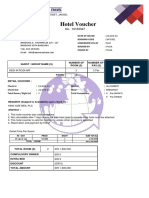

- Hotel Voucher: in - Out Price Night Sub TotalDocumento1 paginaHotel Voucher: in - Out Price Night Sub Totaldedi enggoNessuna valutazione finora

- Production CostsDocumento68 pagineProduction CostsResearch BoyNessuna valutazione finora

- CM Hoskins & Co., Inc. Vs Cir GR No L-24059 November 28, 1969Documento4 pagineCM Hoskins & Co., Inc. Vs Cir GR No L-24059 November 28, 1969Marianne Shen PetillaNessuna valutazione finora

- Chapter 17 IAS 36 Impairment of AssetsDocumento13 pagineChapter 17 IAS 36 Impairment of AssetsKelvin Chu JYNessuna valutazione finora

- Price ListDocumento1 paginaPrice ListDavid MaskellNessuna valutazione finora

- Baked Goods in The Philippines PDFDocumento11 pagineBaked Goods in The Philippines PDFAngelo FerrerNessuna valutazione finora

- FIN7520 Notes On Chapter 14 and 15 Bond Prices and YieldsDocumento8 pagineFIN7520 Notes On Chapter 14 and 15 Bond Prices and YieldsMichael PironeNessuna valutazione finora

- Mg6863 Engineering Economics Viii Yr 8th SemDocumento57 pagineMg6863 Engineering Economics Viii Yr 8th SemshubhamNessuna valutazione finora

- Macroeconomics Study GuideDocumento60 pagineMacroeconomics Study Guidewilder_hart100% (1)

- CH 25Documento32 pagineCH 25Mohammed Al DhaheriNessuna valutazione finora

- Project ReportDocumento83 pagineProject Reportizharul2004Nessuna valutazione finora

- June 2022 (IAL) QPDocumento32 pagineJune 2022 (IAL) QPsubachaluNessuna valutazione finora

- Munehisa Homma - The Father of Price Action TradingDocumento6 pagineMunehisa Homma - The Father of Price Action TradingJohan HallatuNessuna valutazione finora

- Swot Analsis of 7upDocumento17 pagineSwot Analsis of 7upChirag Arora33% (3)

- Invoice OD219618879639285000 PDFDocumento1 paginaInvoice OD219618879639285000 PDFSUBHADIP DASNessuna valutazione finora

- Shoreline Fire Impact FeesDocumento3 pagineShoreline Fire Impact FeesThe UrbanistNessuna valutazione finora

- Comprehensive Fixed Asset Problem Darby Sporting Goods Inc Has PDFDocumento1 paginaComprehensive Fixed Asset Problem Darby Sporting Goods Inc Has PDFAnbu jaromiaNessuna valutazione finora

- Chapter FiveDocumento37 pagineChapter FiveLakachew GetasewNessuna valutazione finora

- BarruecopardoDocumento6 pagineBarruecopardopedro_cabezas_2Nessuna valutazione finora

- Principles of Economics Asia Pacific 7th Edition Gans Test BankDocumento26 paginePrinciples of Economics Asia Pacific 7th Edition Gans Test Bankbeckhamkhanhrkjxsk100% (27)

- Malaysia Current Inflation SituationDocumento10 pagineMalaysia Current Inflation SituationIdris_Ahad_2009100% (2)

- Mirc ElectronicsDocumento9 pagineMirc Electronicsanand310Nessuna valutazione finora

- G.R. No. 117009. October 11, 1995. Security Bank & Trust Company and Rosito C. MANHIT, Petitioners, vs. COURT OF APPEALS and YSMAEL C. FERRER, RespondentsDocumento7 pagineG.R. No. 117009. October 11, 1995. Security Bank & Trust Company and Rosito C. MANHIT, Petitioners, vs. COURT OF APPEALS and YSMAEL C. FERRER, RespondentsChristineNessuna valutazione finora

- Southwest Airlines MingchiDocumento18 pagineSouthwest Airlines MingchiRishabh BhardwajNessuna valutazione finora

- Aptitude StigenDocumento3 pagineAptitude StigenMonisha VishwanathNessuna valutazione finora