Potrebbero piacerti anche

- Universities as Complex Enterprises: How Academia Works, Why It Works These Ways, and Where the University Enterprise Is HeadedDa EverandUniversities as Complex Enterprises: How Academia Works, Why It Works These Ways, and Where the University Enterprise Is HeadedNessuna valutazione finora

- Chap 013Documento37 pagineChap 013Anuka123Nessuna valutazione finora

- Fundamentals of Corporate Finance: Introduction To Risk, Return, and The Opportunity Cost of CapitalDocumento21 pagineFundamentals of Corporate Finance: Introduction To Risk, Return, and The Opportunity Cost of CapitalMuh BilalNessuna valutazione finora

- Financial Risk ManagementDocumento88 pagineFinancial Risk ManagementErika Mie UlatNessuna valutazione finora

- Financial Risk ManagementDocumento88 pagineFinancial Risk ManagementRichard Dan Ilao ReyesNessuna valutazione finora

- FIN2424 - BFN2034 Chapter 5 Risk and ReturnsDocumento42 pagineFIN2424 - BFN2034 Chapter 5 Risk and ReturnsPratap RavichandranNessuna valutazione finora

- Session 6 (Part 1) : Return and Risk: The Capital Asset Pricing Model (CAPM)Documento49 pagineSession 6 (Part 1) : Return and Risk: The Capital Asset Pricing Model (CAPM)Vương VõNessuna valutazione finora

- Seminar 04Documento15 pagineSeminar 04api-3695734Nessuna valutazione finora

- Financial Management Principles and Applications 13Th Edition Titman Solutions Manual Full Chapter PDFDocumento36 pagineFinancial Management Principles and Applications 13Th Edition Titman Solutions Manual Full Chapter PDFchristopher.ridgeway589100% (10)

- 13 Risk and ReturnDocumento45 pagine13 Risk and ReturnVân TrangNessuna valutazione finora

- Return, Risk, and The Security Market LineDocumento62 pagineReturn, Risk, and The Security Market LineTushar AroraNessuna valutazione finora

- Risk and ReturnDocumento31 pagineRisk and ReturnBon GirlNessuna valutazione finora

- RWJ - FCF11e - Chap - 13-Risk, Return & SMLDocumento45 pagineRWJ - FCF11e - Chap - 13-Risk, Return & SMLCẩm TiênNessuna valutazione finora

- RWJLT FCF 2nd Ed CH 13Documento46 pagineRWJLT FCF 2nd Ed CH 13Maria NatalinaNessuna valutazione finora

- Return, Risk, and The Capital Asset Pricing ModelDocumento41 pagineReturn, Risk, and The Capital Asset Pricing Model楊承諭Nessuna valutazione finora

- Bodie Essentials of Investments 11e Chapter05 AccessibleDocumento41 pagineBodie Essentials of Investments 11e Chapter05 Accessiblea188740Nessuna valutazione finora

- Lec12 Discount RatesDocumento31 pagineLec12 Discount RatesAnonymous 9nn66QowZ5Nessuna valutazione finora

- Return, Risk, and The Security Market LineDocumento45 pagineReturn, Risk, and The Security Market Lineotaku himeNessuna valutazione finora

- How To Calculate Present Values: Principles of Corporate FinanceDocumento42 pagineHow To Calculate Present Values: Principles of Corporate Financesachin199021Nessuna valutazione finora

- 11ed FIN 421 PP - CH005Documento87 pagine11ed FIN 421 PP - CH005Anonymous ZWWRotNessuna valutazione finora

- Capital Asset Pricing ModelDocumento25 pagineCapital Asset Pricing ModelShah KamalNessuna valutazione finora

- FBL5Documento12 pagineFBL5FaleeNessuna valutazione finora

- Ch. 5Documento20 pagineCh. 5Shovan ChowdhuryNessuna valutazione finora

- Chapter 13 (Spring 2017)Documento40 pagineChapter 13 (Spring 2017)Vinny Mustika SariNessuna valutazione finora

- EFM2e, CH 07, Slides-1Documento51 pagineEFM2e, CH 07, Slides-1Maria DevinaNessuna valutazione finora

- Essentials of Investments 9th Edition Bodie Solutions ManualDocumento14 pagineEssentials of Investments 9th Edition Bodie Solutions ManualsamanthaadamsgofinbesmrNessuna valutazione finora

- Corporate Finance 11th Edition Ross Solutions ManualDocumento17 pagineCorporate Finance 11th Edition Ross Solutions Manualformatbalanoidyxl100% (33)

- FFM15, CH 08 (Risk), Chapter Model, 2-08-18Documento11 pagineFFM15, CH 08 (Risk), Chapter Model, 2-08-18Hà Phương PhạmNessuna valutazione finora

- Risk and Return - Lu-6Documento54 pagineRisk and Return - Lu-6Mega capitalmarket100% (1)

- Jane Smith ADocumento4 pagineJane Smith AdreamvikramNessuna valutazione finora

- How To Calculate PV - FV - Annuity - PerpetuityDocumento41 pagineHow To Calculate PV - FV - Annuity - PerpetuityHassane AmadouNessuna valutazione finora

- 5 Return & RiskDocumento23 pagine5 Return & RiskOmar Faruk 2235292660Nessuna valutazione finora

- Risk and Return: Centre For Financial Management, BangaloreDocumento29 pagineRisk and Return: Centre For Financial Management, BangalorekirishnakanthNessuna valutazione finora

- Essentials of Investments: Efficient DiversificationDocumento38 pagineEssentials of Investments: Efficient DiversificationShezan BakirNessuna valutazione finora

- Risk and Return: RETURN: If You Buy An Asset of Any Sort, Your Gain (Or Loss) From That Investment Is Called TheDocumento15 pagineRisk and Return: RETURN: If You Buy An Asset of Any Sort, Your Gain (Or Loss) From That Investment Is Called TheFear Part 2Nessuna valutazione finora

- M5 - Risk and ReturnDocumento76 pagineM5 - Risk and ReturnZergaia WPNessuna valutazione finora

- CF 10e Chapter 11 Excel Master StudentDocumento32 pagineCF 10e Chapter 11 Excel Master StudentWalter CostaNessuna valutazione finora

- Continuation To StocksDocumento53 pagineContinuation To StocksTahaNessuna valutazione finora

- The Time Value of Money: Fundamentals of Corporate FinanceDocumento36 pagineThe Time Value of Money: Fundamentals of Corporate FinanceMuh BilalNessuna valutazione finora

- Interest Rate Risk IDocumento17 pagineInterest Rate Risk Ianon_215805Nessuna valutazione finora

- FM - Risk and Rates of ReturnDocumento10 pagineFM - Risk and Rates of ReturnMaxine SantosNessuna valutazione finora

- Finance BIS & FMI SheetDocumento13 pagineFinance BIS & FMI SheetSouliman MuhammadNessuna valutazione finora

- Lecture 4 Return and RiskDocumento50 pagineLecture 4 Return and RiskMuhammad YahyaNessuna valutazione finora

- Essentials of Investments 10th Edition Bodie Solutions Manual DownloadDocumento14 pagineEssentials of Investments 10th Edition Bodie Solutions Manual DownloadJennifer Walker100% (21)

- Chapter 5 SolutionsDocumento16 pagineChapter 5 Solutionshassan.murad60% (5)

- 2 Asset-Pricing-PrerequisitesDocumento7 pagine2 Asset-Pricing-Prerequisitesrichard.hugsNessuna valutazione finora

- Week 5 - Efficient DiversificationDocumento40 pagineWeek 5 - Efficient DiversificationshanikaNessuna valutazione finora

- Investment Analysis and Portfolio Management: Practice 5Documento10 pagineInvestment Analysis and Portfolio Management: Practice 5jovvy24Nessuna valutazione finora

- Solutions For Credit RiskDocumento3 pagineSolutions For Credit RiskTuan Tran VanNessuna valutazione finora

- Moat Analysis Xyz 1 Xyz 2 Xyz 3 Xyz 4 Xyz 5 Xyz 6: QualitativeDocumento24 pagineMoat Analysis Xyz 1 Xyz 2 Xyz 3 Xyz 4 Xyz 5 Xyz 6: QualitativeRaghuNessuna valutazione finora

- Week4 Slides Correlation+and+DiversificationDocumento25 pagineWeek4 Slides Correlation+and+DiversificationKinnata NikkoNessuna valutazione finora

- Last Time We Thought About Combining A Risky Portfolio With A Riskless AssetDocumento42 pagineLast Time We Thought About Combining A Risky Portfolio With A Riskless AssetBiren PatelNessuna valutazione finora

- Chapter Six Risk and ReturnDocumento46 pagineChapter Six Risk and ReturnLetaNessuna valutazione finora

- Unit 3: Risk, Return, and Capital Asset Pricing Model (CAPMDocumento30 pagineUnit 3: Risk, Return, and Capital Asset Pricing Model (CAPMCyrine Miwa RodriguezNessuna valutazione finora

- Investments, 8 Edition: Learning About Return and Risk From The Historical RecordDocumento23 pagineInvestments, 8 Edition: Learning About Return and Risk From The Historical RecordFadhel AlsadahNessuna valutazione finora

- C2 M2 Diversification PortfolioRiskDocumento13 pagineC2 M2 Diversification PortfolioRisktfdsgNessuna valutazione finora

- Risk and ReturnDocumento7 pagineRisk and Returnsofia garcinesNessuna valutazione finora

- Risk and Return PDFDocumento40 pagineRisk and Return PDFKavindu SankalpaNessuna valutazione finora

- Six Skills Effective Managers Must MasterDocumento6 pagineSix Skills Effective Managers Must MasterVeeramani ArumugamNessuna valutazione finora

- Risk and Return: Instructor: Ajab Khan BurkiDocumento56 pagineRisk and Return: Instructor: Ajab Khan BurkiGaurav KarkiNessuna valutazione finora

- Assignmentdissolution Retirement WithdrawalDocumento6 pagineAssignmentdissolution Retirement Withdrawalnelle de leonNessuna valutazione finora

- Threshold 1 Big BangDocumento18 pagineThreshold 1 Big Bangnelle de leonNessuna valutazione finora

- Definition of Money MarketsDocumento21 pagineDefinition of Money Marketsnelle de leonNessuna valutazione finora

- FinMar 14Documento4 pagineFinMar 14nelle de leonNessuna valutazione finora

- Two Poles of TheologyDocumento1 paginaTwo Poles of Theologynelle de leonNessuna valutazione finora

- Acct. No. Account Title Debit CreditDocumento2 pagineAcct. No. Account Title Debit Creditnelle de leonNessuna valutazione finora

- Capital Budgeting Cash Flows ComputationDocumento6 pagineCapital Budgeting Cash Flows Computationnelle de leonNessuna valutazione finora

- Capital Budgeting Seatwork 2 MWFDocumento1 paginaCapital Budgeting Seatwork 2 MWFnelle de leonNessuna valutazione finora

- Optimal Heat Transfer Calculation and Balancing For Gas Sweetening Process A Case StudyDocumento9 pagineOptimal Heat Transfer Calculation and Balancing For Gas Sweetening Process A Case Studylutfi awnNessuna valutazione finora

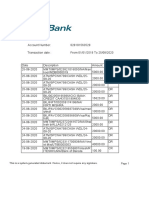

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDocumento15 pagineThis Is A System-Generated Statement. Hence, It Does Not Require Any SignaturemohitNessuna valutazione finora

- КАТАЛОГ РОБИТ 2012г - lowresDocumento94 pagineКАТАЛОГ РОБИТ 2012г - lowresДамир НазиповNessuna valutazione finora

- Fairtrade, Employment and Poverty Reduction in Ethiopia and Uganda - Final Report To DFID, April 2014Documento143 pagineFairtrade, Employment and Poverty Reduction in Ethiopia and Uganda - Final Report To DFID, April 2014poorfarmerNessuna valutazione finora

- Green Steel AssuranceDocumento6 pagineGreen Steel AssuranceRajat SinghNessuna valutazione finora

- AnlysisDocumento15 pagineAnlysisMoustafaNessuna valutazione finora

- Marathon TX 1Documento12 pagineMarathon TX 1alexandruyoNessuna valutazione finora

- Air Water System Design Using Revit Mep For A Residential BuildingDocumento5 pagineAir Water System Design Using Revit Mep For A Residential BuildingEditor IJTSRDNessuna valutazione finora

- San Miguel vs. Khan (Valera)Documento2 pagineSan Miguel vs. Khan (Valera)ASGarcia24Nessuna valutazione finora

- PVC Pipe Industry Analysis in PakistanDocumento4 paginePVC Pipe Industry Analysis in PakistanOlufemi MoyegunNessuna valutazione finora

- Complete CatalogueDocumento86 pagineComplete CatalogueDaredevil CreationsNessuna valutazione finora

- 978 0 7503 5301 4.previewDocumento86 pagine978 0 7503 5301 4.previewHakim KaciNessuna valutazione finora

- Miami Dade County Ethics Commission Report in Re Miami Beach Fire MarshallDocumento12 pagineMiami Dade County Ethics Commission Report in Re Miami Beach Fire MarshallDavid Arthur WaltersNessuna valutazione finora

- Schneider PLC and Unity Pro XLDocumento18 pagineSchneider PLC and Unity Pro XLSrinivas VenkatramanNessuna valutazione finora

- Week 10 - Monitoring and Auditing AIS - PresentationDocumento32 pagineWeek 10 - Monitoring and Auditing AIS - PresentationChristian Gundran DiamseNessuna valutazione finora

- Problem 1.6Documento1 paginaProblem 1.6SamerNessuna valutazione finora

- Mipi-Tutorial PDF CompressedDocumento13 pagineMipi-Tutorial PDF CompressedGeorgeNessuna valutazione finora

- State Wise Installed Capacity As On 30.06.2019Documento2 pagineState Wise Installed Capacity As On 30.06.2019Bhom Singh NokhaNessuna valutazione finora

- Fallling Objects TBT - FinalDocumento2 pagineFallling Objects TBT - FinalAhmed EssaNessuna valutazione finora

- Risk Management and Insurance PDFDocumento172 pagineRisk Management and Insurance PDFRohit VkNessuna valutazione finora

- MAX1204 5V, 8-Channel, Serial, 10-Bit ADC With 3V Digital InterfaceDocumento24 pagineMAX1204 5V, 8-Channel, Serial, 10-Bit ADC With 3V Digital InterfaceGeorge BintarchasNessuna valutazione finora

- Customer Relationship Management and Customer ExperienceDocumento43 pagineCustomer Relationship Management and Customer ExperienceYusrah JberNessuna valutazione finora

- Role of Banking in International BusinessDocumento15 pagineRole of Banking in International Businesstheaaj100% (2)

- Question PaperDocumento4 pagineQuestion PaperKenneth RichardsNessuna valutazione finora

- Globolisation and CultureDocumento4 pagineGlobolisation and CultureDavide MwaleNessuna valutazione finora

- Formation Damage and StimulationDocumento16 pagineFormation Damage and Stimulationxion_mew2Nessuna valutazione finora

- Module 1: Exploring EntrepreneurshipDocumento5 pagineModule 1: Exploring EntrepreneurshipZara DelacruzNessuna valutazione finora

- Get Rich Young - Kishore MDocumento85 pagineGet Rich Young - Kishore MArmand Dagbegnon TossouNessuna valutazione finora

- Blender 3D Incredible Machines - Sample ChapterDocumento34 pagineBlender 3D Incredible Machines - Sample ChapterPackt PublishingNessuna valutazione finora

- 67N SIP5 - 7SA-SD-SL-VK-87 - V04.00 - Manual - C011-4 - En-2Documento44 pagine67N SIP5 - 7SA-SD-SL-VK-87 - V04.00 - Manual - C011-4 - En-2Luis Miguel DíazNessuna valutazione finora