Potrebbero piacerti anche

- Fiverrr AsadDocumento3 pagineFiverrr AsadRajib Ali100% (2)

- Aes Case SolutionDocumento3 pagineAes Case SolutionXimenaLopezCifuentes100% (1)

- Chapter 5 Bonds and StocksDocumento61 pagineChapter 5 Bonds and StocksJulie Mae Caling MalitNessuna valutazione finora

- Quiz 4 Sample QuestionsDocumento4 pagineQuiz 4 Sample Questionsbusiness docNessuna valutazione finora

- Dixon Technologies Annual Report Analysis 18 September 2021Documento12 pagineDixon Technologies Annual Report Analysis 18 September 2021Equity NestNessuna valutazione finora

- BUY ITC: On A Steady PathDocumento19 pagineBUY ITC: On A Steady PathTatsam VipulNessuna valutazione finora

- 2023 M&A Trends ReportDocumento16 pagine2023 M&A Trends ReportFuture-Proof AdvisorsNessuna valutazione finora

- Rul Mamoelis Update 181122Documento6 pagineRul Mamoelis Update 181122jonathan gohNessuna valutazione finora

- City Boys - Europe, North and Central AsiaDocumento12 pagineCity Boys - Europe, North and Central Asia7fhhnrxgnyNessuna valutazione finora

- Pidilite Industries: Robust Recovery Margin Pressure AheadDocumento15 paginePidilite Industries: Robust Recovery Margin Pressure AheadIS group 7Nessuna valutazione finora

- MR D.I.Y. Group (M) (MRDIY MK) : Shopping For A Great BargainDocumento18 pagineMR D.I.Y. Group (M) (MRDIY MK) : Shopping For A Great BargainMohd ShahrirNessuna valutazione finora

- ACCT 503B Advanced Business Analysis - Disney Final Report V2Documento16 pagineACCT 503B Advanced Business Analysis - Disney Final Report V2reiner satrioNessuna valutazione finora

- 2022 09 07 BILI - Oq Macquarie Research Bilibili (9626 HKBILI US) 98239208Documento28 pagine2022 09 07 BILI - Oq Macquarie Research Bilibili (9626 HKBILI US) 98239208bellabell8821Nessuna valutazione finora

- IDBI Capital Century Plyboards Q4FY22 Result UpdateDocumento10 pagineIDBI Capital Century Plyboards Q4FY22 Result UpdateTai TranNessuna valutazione finora

- City Boys - Europe, North and Central AsiaDocumento12 pagineCity Boys - Europe, North and Central Asia7fhhnrxgnyNessuna valutazione finora

- Bharti Airtel Q3FY24 Result Update - 07022024 - 07-02-2024 - 12Documento9 pagineBharti Airtel Q3FY24 Result Update - 07022024 - 07-02-2024 - 12Sanjeedeep Mishra , 315Nessuna valutazione finora

- Dixon Technologies - Q4FY22 Result Update - 31052022 - 31-05-2022 - 14Documento8 pagineDixon Technologies - Q4FY22 Result Update - 31052022 - 31-05-2022 - 14Sachin DhimanNessuna valutazione finora

- 'KQHK NhikoyhDocumento12 pagine'KQHK NhikoyhGiri BabaNessuna valutazione finora

- PB Fintech Icici SecuritiesDocumento33 paginePB Fintech Icici SecuritieshamsNessuna valutazione finora

- Glo Ir2020Documento378 pagineGlo Ir2020akosimawilynNessuna valutazione finora

- Dixon Technologies Q1FY22 Result UpdateDocumento8 pagineDixon Technologies Q1FY22 Result UpdateAmos RiveraNessuna valutazione finora

- File 1686286056102Documento14 pagineFile 1686286056102Tomar SahaabNessuna valutazione finora

- BSY Equity Research - Final ReportDocumento16 pagineBSY Equity Research - Final Reportjazz.srishNessuna valutazione finora

- ITC Limited: Strategy Refresh To Build Investor ConfidenceDocumento15 pagineITC Limited: Strategy Refresh To Build Investor Confidenceaathi sakthiNessuna valutazione finora

- Wipro CompanyUpdate22Nov21 ResearchDocumento6 pagineWipro CompanyUpdate22Nov21 Researchde natureshopNessuna valutazione finora

- PLDT Inc.: Raising The Bar - Upgrade To BuyDocumento10 paginePLDT Inc.: Raising The Bar - Upgrade To BuyP RosenbergNessuna valutazione finora

- 2022 q3 Earnings Results PresentationDocumento21 pagine2022 q3 Earnings Results PresentationZerohedgeNessuna valutazione finora

- Group1 SectionADocumento10 pagineGroup1 SectionAAnurag KumarNessuna valutazione finora

- 7204 - D&O - PUBLIC BANK - 2023-08-24 - BUY - 4.37 - DOGreenTechnologiesExpectingaVShapeRecovery - 1840691060Documento5 pagine7204 - D&O - PUBLIC BANK - 2023-08-24 - BUY - 4.37 - DOGreenTechnologiesExpectingaVShapeRecovery - 1840691060Nicholas ChehNessuna valutazione finora

- Divis RRDocumento10 pagineDivis RRRicha P SinghalNessuna valutazione finora

- Wlcon - PS Wlcon PMDocumento10 pagineWlcon - PS Wlcon PMP RosenbergNessuna valutazione finora

- CMP: INR264 Strong Near-Term Visibility Environment ConduciveDocumento14 pagineCMP: INR264 Strong Near-Term Visibility Environment ConducivebradburywillsNessuna valutazione finora

- Itc (Itc In) : Analyst Meet UpdateDocumento18 pagineItc (Itc In) : Analyst Meet UpdateTatsam Vipul100% (1)

- Barclays WMG U.S. Media - DIS - Still Early in The Reset PhaseDocumento27 pagineBarclays WMG U.S. Media - DIS - Still Early in The Reset PhaseraymanNessuna valutazione finora

- Jarir GIB 2022.10Documento15 pagineJarir GIB 2022.10robynxjNessuna valutazione finora

- Siemens India: Thematically It Makes Sense But Valuations Don'tDocumento9 pagineSiemens India: Thematically It Makes Sense But Valuations Don'tRaghvendra N DhootNessuna valutazione finora

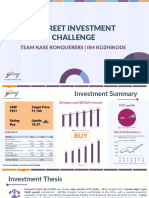

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocumento12 pagineR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNessuna valutazione finora

- NB Stock Pitch-Stocksrock - (For Scribd)Documento7 pagineNB Stock Pitch-Stocksrock - (For Scribd)Mankaran KharbandaNessuna valutazione finora

- Infosys: Growth Certainty On Explosive Deal WinsDocumento2 pagineInfosys: Growth Certainty On Explosive Deal Winsmehrotraanand016912Nessuna valutazione finora

- Crompton Gr. Con: CMP: INR455Documento28 pagineCrompton Gr. Con: CMP: INR455Jayash KaushalNessuna valutazione finora

- Renewable Volume ObligationDocumento9 pagineRenewable Volume ObligationHieu NgoNessuna valutazione finora

- 4716156162022739schneider Electric Infrastructure Ltd. Q4FY22 - SignedDocumento5 pagine4716156162022739schneider Electric Infrastructure Ltd. Q4FY22 - SignedbradburywillsNessuna valutazione finora

- IIFL Report For RefrenceDocumento101 pagineIIFL Report For RefrenceaddadddddddddNessuna valutazione finora

- 0102191402-Analyst PPT 9MFY19Documento39 pagine0102191402-Analyst PPT 9MFY19Vineet SharmaNessuna valutazione finora

- (Kotak) Zee Entertainment Enterprises, May 30, 2022Documento11 pagine(Kotak) Zee Entertainment Enterprises, May 30, 2022darshanmaldeNessuna valutazione finora

- Persistent Sys Case StudyDocumento34 paginePersistent Sys Case StudyGrim ReaperNessuna valutazione finora

- Corning Inc Q2 GraphicDocumento1 paginaCorning Inc Q2 GraphicGeorge StockburgerNessuna valutazione finora

- InfosysDocumento13 pagineInfosysreena21a9Nessuna valutazione finora

- Affle Corporate PresentationDocumento39 pagineAffle Corporate Presentationchiragchhillar9711Nessuna valutazione finora

- Barclays U Unity Software Inc. Beat & Raise With $1B EBITDA TargetDocumento15 pagineBarclays U Unity Software Inc. Beat & Raise With $1B EBITDA Targetoldman lokNessuna valutazione finora

- Itc 12 12 23 PLDocumento21 pagineItc 12 12 23 PLDeepul WadhwaNessuna valutazione finora

- Nirmal Bang PDFDocumento11 pagineNirmal Bang PDFBook MonkNessuna valutazione finora

- Creating Value For ShareholdersDocumento8 pagineCreating Value For Shareholders18ITR028 Janaranjan ENessuna valutazione finora

- Syngene International: Discovery Services Driving Growth Outlook UpbeatDocumento11 pagineSyngene International: Discovery Services Driving Growth Outlook Upbeatsanketsabale26Nessuna valutazione finora

- AffleIndia Q2FY22ResultReview12Nov21 ResearchDocumento8 pagineAffleIndia Q2FY22ResultReview12Nov21 Researchde natureshopNessuna valutazione finora

- Bhansali Engineering Polymers - 34 AGM HighlightsDocumento4 pagineBhansali Engineering Polymers - 34 AGM HighlightsAbhinav SrivastavaNessuna valutazione finora

- Infosys: Digital Trajectory Intact, Revises Guidance UpwardsDocumento11 pagineInfosys: Digital Trajectory Intact, Revises Guidance UpwardsanjugaduNessuna valutazione finora

- 2019 q1 Earnings Results PresentationDocumento23 pagine2019 q1 Earnings Results PresentationValter SilveiraNessuna valutazione finora

- Dish TV: IndiaDocumento8 pagineDish TV: Indiaashok yadavNessuna valutazione finora

- Infosys: Strong Revenue, Margin Resilience Is KeyDocumento8 pagineInfosys: Strong Revenue, Margin Resilience Is KeyKrish JNessuna valutazione finora

- Safari Industries BUY: Growth Momentum To Continue.Documento20 pagineSafari Industries BUY: Growth Momentum To Continue.dcoolsamNessuna valutazione finora

- Wipro LTD: Profitable Growth Focus of New CEODocumento11 pagineWipro LTD: Profitable Growth Focus of New CEOPramod KulkarniNessuna valutazione finora

- Kino Indonesia: Equity ResearchDocumento5 pagineKino Indonesia: Equity ResearchHot AsiNessuna valutazione finora

- A New Dawn for Global Value Chain Participation in the PhilippinesDa EverandA New Dawn for Global Value Chain Participation in the PhilippinesNessuna valutazione finora

- Property Valuation Analysis: Building I Want 160Documento21 pagineProperty Valuation Analysis: Building I Want 160yhcdyhdNessuna valutazione finora

- M&a Intern Analyst - Job DetailsDocumento4 pagineM&a Intern Analyst - Job DetailsyhcdyhdNessuna valutazione finora

- Poland A2 Motorway Case: Opim 5894 Advanced Project ManagementDocumento10 paginePoland A2 Motorway Case: Opim 5894 Advanced Project ManagementyhcdyhdNessuna valutazione finora

- Mifft Journey Planner: Term 1 Term 2 Term 3 Term 4 (Optional)Documento3 pagineMifft Journey Planner: Term 1 Term 2 Term 3 Term 4 (Optional)yhcdyhdNessuna valutazione finora

- Case Questions: Poland's A2 MotorwayDocumento1 paginaCase Questions: Poland's A2 MotorwayyhcdyhdNessuna valutazione finora

- Chapter01 Legal ConceptsDocumento14 pagineChapter01 Legal ConceptsyhcdyhdNessuna valutazione finora

- Disney Trading Comps AnalysisDocumento4 pagineDisney Trading Comps AnalysisyhcdyhdNessuna valutazione finora

- Hard Difficulty QuestionsDocumento4 pagineHard Difficulty QuestionsyhcdyhdNessuna valutazione finora

- ImmuLogic Phar A (Student)Documento11 pagineImmuLogic Phar A (Student)yhcdyhdNessuna valutazione finora

- JNDJWNDJWDocumento7 pagineJNDJWNDJWyhcdyhdNessuna valutazione finora

- Competition and Policies Towards Monopolies and Oligopolies, Privatization and RegulationDocumento9 pagineCompetition and Policies Towards Monopolies and Oligopolies, Privatization and RegulationTrisha VelascoNessuna valutazione finora

- CF WACC, WC NewDocumento5 pagineCF WACC, WC NewSanjana PottipallyNessuna valutazione finora

- MCA 1st & 2nd FinalDocumento12 pagineMCA 1st & 2nd FinalbibekbcNessuna valutazione finora

- Compass RecordsDocumento5 pagineCompass RecordsLuxmiSoodNessuna valutazione finora

- 6 Receivables ManagementDocumento12 pagine6 Receivables ManagementShreya BhagavatulaNessuna valutazione finora

- Chapter 11 Leveraged Buyout Structures and ValuationDocumento27 pagineChapter 11 Leveraged Buyout Structures and ValuationanubhavhinduNessuna valutazione finora

- Capital Structure Theories FINALDocumento46 pagineCapital Structure Theories FINALkawalsekhonNessuna valutazione finora

- Afm June 2016 QTDocumento13 pagineAfm June 2016 QTBijay AgrawalNessuna valutazione finora

- CapBud-Outline-Spring 2021Documento2 pagineCapBud-Outline-Spring 2021Mahmudur RahmanNessuna valutazione finora

- Corporate Finance Project On: Estimation of Beta and Weighted Average Cost of Capital (WACC) of Selected Stock (HUL)Documento10 pagineCorporate Finance Project On: Estimation of Beta and Weighted Average Cost of Capital (WACC) of Selected Stock (HUL)Sumedh BhagwatNessuna valutazione finora

- Voluntary DisclosureDocumento9 pagineVoluntary DisclosuremalemekhannaNessuna valutazione finora

- Women in Banking 40m (Empty)Documento338 pagineWomen in Banking 40m (Empty)El rincón de las 5 EL RINCÓN DE LAS 5Nessuna valutazione finora

- Chapter 16 - : Planning The Firm's Financing MixDocumento56 pagineChapter 16 - : Planning The Firm's Financing MixHanna Al ZahraNessuna valutazione finora

- Cost of CapitalDocumento16 pagineCost of CapitalRuchi SharmaNessuna valutazione finora

- Feu Mas Midterm Summer 2019Documento27 pagineFeu Mas Midterm Summer 2019louise carinoNessuna valutazione finora

- Training Hand Out - Economic Evaluation and Modeling of Mining ProjectsDocumento73 pagineTraining Hand Out - Economic Evaluation and Modeling of Mining ProjectsAriyanto WibowoNessuna valutazione finora

- Wasim Uddin Orakzai KUST IM Sciences Multinational Business Finance All Formula List 10th Edition by David K Etiman Stone Hi Ill Micheal H Moffitt ISBN 0 321 17894 7Documento14 pagineWasim Uddin Orakzai KUST IM Sciences Multinational Business Finance All Formula List 10th Edition by David K Etiman Stone Hi Ill Micheal H Moffitt ISBN 0 321 17894 7WasimOrakzaiNessuna valutazione finora

- GogglesDocumento42 pagineGogglesVatsal GadhiaNessuna valutazione finora

- Exxon Mobil MergerDocumento60 pagineExxon Mobil MergerTojobdNessuna valutazione finora

- 2019 Level I Mock C (PM) QuestionsDocumento21 pagine2019 Level I Mock C (PM) QuestionsshNessuna valutazione finora

- Capital Structure Decision Is Important For A Firm BecauseDocumento9 pagineCapital Structure Decision Is Important For A Firm BecauseAditya RathiNessuna valutazione finora

- IAS 36 Impairment Testing 2011Documento20 pagineIAS 36 Impairment Testing 2011Mihai CojocaruNessuna valutazione finora

- II M.Com Even Semester 2023-24Documento7 pagineII M.Com Even Semester 2023-24pgkathiravan007Nessuna valutazione finora

- CPALE Syllabi Effective May 2019 PROPOSALDocumento25 pagineCPALE Syllabi Effective May 2019 PROPOSALSMBNessuna valutazione finora

- BEC 3 - Financial ManagementDocumento11 pagineBEC 3 - Financial ManagementAudreys PageNessuna valutazione finora

- The Effect of Capital Structure On Firms' Profitability (Evidenced From Ethiopian) PDFDocumento9 pagineThe Effect of Capital Structure On Firms' Profitability (Evidenced From Ethiopian) PDFKulsoomNessuna valutazione finora