Potrebbero piacerti anche

- Chap 003Documento80 pagineChap 003Loser NeetNessuna valutazione finora

- Chapter 3Documento53 pagineChapter 3cejofe2892Nessuna valutazione finora

- Financial Statement Analysis: K.R. SubramanyamDocumento79 pagineFinancial Statement Analysis: K.R. SubramanyamFitri SafiraNessuna valutazione finora

- Financial Statement Analysis: K.R. SubramanyamDocumento37 pagineFinancial Statement Analysis: K.R. SubramanyamFitri SafiraNessuna valutazione finora

- Bab 5 Analisis Laporan KeuanganDocumento54 pagineBab 5 Analisis Laporan KeuanganBenedict MihoyoNessuna valutazione finora

- ICM Text Book UpdateDocumento78 pagineICM Text Book UpdatemariposaNessuna valutazione finora

- DirectFileTopicDownload 7Documento18 pagineDirectFileTopicDownload 7anikiwe489Nessuna valutazione finora

- Financial Statement Analysis, 10e by K. R. Subramanyam & John J. Wild Chapter03Documento40 pagineFinancial Statement Analysis, 10e by K. R. Subramanyam & John J. Wild Chapter03RidhoVerianNessuna valutazione finora

- Financial Statement Analysis: K R Subramanyam John J WildDocumento38 pagineFinancial Statement Analysis: K R Subramanyam John J WildMar SihNessuna valutazione finora

- Chapter 3 Analysing Financing ActivitiesDocumento35 pagineChapter 3 Analysing Financing ActivitiesGRACE CHANNessuna valutazione finora

- Lec 3Documento54 pagineLec 3Ahmad FauzanNessuna valutazione finora

- Corporate Structure and AdministrationDocumento10 pagineCorporate Structure and AdministrationDr.Sree Lakshmi KNessuna valutazione finora

- FIASDocumento4 pagineFIASTika GusmawarniNessuna valutazione finora

- Module 7 - Xid-133533 - 1Documento18 pagineModule 7 - Xid-133533 - 1Maurizze BarcarseNessuna valutazione finora

- Financing Decision: Dr. Md. Rezaul KabirDocumento129 pagineFinancing Decision: Dr. Md. Rezaul KabirUrbana Raquib Rodosee100% (1)

- Remf Module 5Documento32 pagineRemf Module 5Sharon BennyNessuna valutazione finora

- Topic 11 EquityDocumento21 pagineTopic 11 EquityAbd AL Rahman Shah Bin Azlan ShahNessuna valutazione finora

- Presented by - Parikshit Saha Pankaj Lokesh Randeep Garg Sahil Aggarwal Nishant AdlakhaDocumento70 paginePresented by - Parikshit Saha Pankaj Lokesh Randeep Garg Sahil Aggarwal Nishant AdlakhaRandeep Garg100% (1)

- Chapter 8 OSC PSC, Loan Capital and Bond ValuationDocumento34 pagineChapter 8 OSC PSC, Loan Capital and Bond Valuationathirah jamaludinNessuna valutazione finora

- CH 5 Types of Financing DecisionsDocumento30 pagineCH 5 Types of Financing DecisionsAnkur AggarwalNessuna valutazione finora

- Chapter 03Documento39 pagineChapter 03Nor Asma LodeNessuna valutazione finora

- Finance OverviewDocumento38 pagineFinance OverviewGeethika NayanaprabhaNessuna valutazione finora

- Debt or Equity For BusinessDocumento7 pagineDebt or Equity For BusinessEdgar OkitoiNessuna valutazione finora

- Capital Markt: (Short Term Market)Documento59 pagineCapital Markt: (Short Term Market)Tanish BhasinNessuna valutazione finora

- 1 Corporate Finance IntroductionDocumento21 pagine1 Corporate Finance IntroductionNiharika AgarwalNessuna valutazione finora

- CSC - Chapter11 - Corporations and Their Financial Statements - F2021Documento72 pagineCSC - Chapter11 - Corporations and Their Financial Statements - F2021AlecNessuna valutazione finora

- Capitulo 3Documento6 pagineCapitulo 3Sara CarvalhoNessuna valutazione finora

- Chapter 23BBDocumento27 pagineChapter 23BBTaVuKieuNhi100% (1)

- Ch03-Corporations Issuing Equity in The Share MarketDocumento17 pagineCh03-Corporations Issuing Equity in The Share MarketHồ ThảoNessuna valutazione finora

- Chapter 7Documento36 pagineChapter 7Natanael Pakpahan100% (1)

- Libby 4ce Solutions Manual - Ch12Documento43 pagineLibby 4ce Solutions Manual - Ch127595522Nessuna valutazione finora

- MGMT2023 Lecture 7 STOCK VALUATION - Parts I, II IIIDocumento86 pagineMGMT2023 Lecture 7 STOCK VALUATION - Parts I, II IIIIsmadth2918388Nessuna valutazione finora

- FM-Sessions 23 - 24 Dividend Policy-CompleteDocumento72 pagineFM-Sessions 23 - 24 Dividend Policy-CompleteSaadat ShaikhNessuna valutazione finora

- Accounting For Companies-1Documento50 pagineAccounting For Companies-1daniel.maina2005Nessuna valutazione finora

- The Balance Sheet and Notes To The Financial StatementDocumento106 pagineThe Balance Sheet and Notes To The Financial StatementJainee Dumaya CatipayNessuna valutazione finora

- FIASDocumento15 pagineFIASTika GusmawarniNessuna valutazione finora

- Financial StatementDocumento117 pagineFinancial Statementyensyifa77Nessuna valutazione finora

- Ch.10 Financing BusinessDocumento32 pagineCh.10 Financing BusinessSisiliaNessuna valutazione finora

- The Balance Sheet and Financial DisclosuresDocumento20 pagineThe Balance Sheet and Financial DisclosuresMadchestervillainNessuna valutazione finora

- Capital Structure PlanningDocumento25 pagineCapital Structure PlanningSumit MahajanNessuna valutazione finora

- BBMF 3183 Strategic Financial Management: 13 Corporate ReorganizationsDocumento22 pagineBBMF 3183 Strategic Financial Management: 13 Corporate ReorganizationsKarthina RishiNessuna valutazione finora

- Ias 7Documento26 pagineIas 7Tiya AmuNessuna valutazione finora

- Sources of Finance Voice Recorded Slides 2021Documento21 pagineSources of Finance Voice Recorded Slides 2021Mihlali MgxekwanaNessuna valutazione finora

- Topic 7Documento42 pagineTopic 7Áliyà ÀliNessuna valutazione finora

- Long Term Source of FinanceDocumento35 pagineLong Term Source of FinanceAditya100% (1)

- Dividend Decisions: Dividend: Cash Distribution of Earnings Among ShareholdersDocumento33 pagineDividend Decisions: Dividend: Cash Distribution of Earnings Among ShareholdersKritika BhattNessuna valutazione finora

- Long Term Finance Shares Debentures and Term LoansDocumento21 pagineLong Term Finance Shares Debentures and Term LoansBhagyashree DevNessuna valutazione finora

- Leveraged Buy Outs and Buy Ins: DR Clive Vlieland-BoddyDocumento37 pagineLeveraged Buy Outs and Buy Ins: DR Clive Vlieland-Boddyjturner19742Nessuna valutazione finora

- RM Assignment-3: Q1. Dividend Policy Can Be Used To Maximize The Wealth of The Shareholder. Explain. AnswerDocumento4 pagineRM Assignment-3: Q1. Dividend Policy Can Be Used To Maximize The Wealth of The Shareholder. Explain. AnswerSiddhant gudwaniNessuna valutazione finora

- Financing - Equity Finance: Chapter Learning ObjectivesDocumento15 pagineFinancing - Equity Finance: Chapter Learning ObjectivesDINEO PRUDENCE NONGNessuna valutazione finora

- Unit 4 FM AJKDocumento26 pagineUnit 4 FM AJKOmega SambakunsiNessuna valutazione finora

- Chap 005Documento41 pagineChap 005Loser Neet100% (1)

- 1 Corporate Finance IntroductionDocumento41 pagine1 Corporate Finance IntroductionPooja KaulNessuna valutazione finora

- Chapter 9: Balance Sheet and Statement of Cash Flows SystemsDocumento21 pagineChapter 9: Balance Sheet and Statement of Cash Flows SystemsPUTTU GURU PRASAD SENGUNTHA MUDALIARNessuna valutazione finora

- Estimating Capital RequirementDocumento7 pagineEstimating Capital RequirementVishwo ShresthaNessuna valutazione finora

- Outline of Discussions.Documento103 pagineOutline of Discussions.JamesNessuna valutazione finora

- Far410 Chapter 3 Equity EditedDocumento32 pagineFar410 Chapter 3 Equity EditedWAN AMIRUL MUHAIMIN WAN ZUKAMALNessuna valutazione finora

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingDa EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNessuna valutazione finora

- SERIES 65 EXAM STUDY GUIDE 2021 + TEST BANKDa EverandSERIES 65 EXAM STUDY GUIDE 2021 + TEST BANKNessuna valutazione finora

- Financial Statement Analysis: K.R. SubramanyamDocumento49 pagineFinancial Statement Analysis: K.R. Subramanyammaria fernNessuna valutazione finora

- ENG2012 GEN2010 Unit 1Documento88 pagineENG2012 GEN2010 Unit 1maria fernNessuna valutazione finora

- Eng 2012Documento69 pagineEng 2012maria fernNessuna valutazione finora

- ACY4401 Advanced Taxation Lecture 3 International Aspects of Current Hong Kong Taxation Law and Practice 1. Double Taxation Agreement ("DTA")Documento13 pagineACY4401 Advanced Taxation Lecture 3 International Aspects of Current Hong Kong Taxation Law and Practice 1. Double Taxation Agreement ("DTA")maria fernNessuna valutazione finora

- Lectures 4 and 5Documento7 pagineLectures 4 and 5maria fernNessuna valutazione finora

- Business Law Notes - AllDocumento56 pagineBusiness Law Notes - Allmaria fernNessuna valutazione finora

- Lecture 2Documento42 pagineLecture 2maria fernNessuna valutazione finora

- Week 13 Exercise With AnswersDocumento10 pagineWeek 13 Exercise With Answersmaria fernNessuna valutazione finora

- ACY 3201 Pre-FinalDocumento8 pagineACY 3201 Pre-Finalmaria fernNessuna valutazione finora

- 7 Employment LawDocumento4 pagine7 Employment Lawmaria fernNessuna valutazione finora

- Purchase Payment Exercise-Answers ASIDocumento3 paginePurchase Payment Exercise-Answers ASImaria fernNessuna valutazione finora

- Internal ControlDocumento6 pagineInternal Controlmaria fernNessuna valutazione finora

- Assignment 2 An Analytical Report On The Advertising and Promotion of A Catering CompanyDocumento6 pagineAssignment 2 An Analytical Report On The Advertising and Promotion of A Catering Companymaria fernNessuna valutazione finora

- BDB1 Unit 7 Assignment 1Documento9 pagineBDB1 Unit 7 Assignment 1maria fernNessuna valutazione finora

- 6 Agency Summary 2Documento4 pagine6 Agency Summary 2maria fernNessuna valutazione finora

- Historic Returns - Small Cap Fund, Small Cap Fund Performance Tracker Mutual Funds With Highest ReturnsDocumento3 pagineHistoric Returns - Small Cap Fund, Small Cap Fund Performance Tracker Mutual Funds With Highest ReturnsAkhilesh Kumar SinghNessuna valutazione finora

- Survey of Economics 8th Edition Tucker Test BankDocumento31 pagineSurvey of Economics 8th Edition Tucker Test Bankamandabinh1j6100% (27)

- Maf603 Test 1 May 2021 - SolutionDocumento3 pagineMaf603 Test 1 May 2021 - SolutionSITI FATIMAH AZ-ZAHRA ABD WAHIDNessuna valutazione finora

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocumento75 pagineInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownAmrit KeyalNessuna valutazione finora

- United States District Court Southern District of New YorkDocumento28 pagineUnited States District Court Southern District of New YorkAnn DwyerNessuna valutazione finora

- Barber & Odean - The Internet and The InvestorDocumento14 pagineBarber & Odean - The Internet and The Investoronat85Nessuna valutazione finora

- Fxrate 28 05 2023Documento2 pagineFxrate 28 05 2023ShohanNessuna valutazione finora

- The Bond Market in GhanaDocumento12 pagineThe Bond Market in GhanaJohn Kennedy Akotia100% (3)

- Universiti Teknologi Mara Common Test 1: Confidential AC/AUG 2015/MAF253Documento6 pagineUniversiti Teknologi Mara Common Test 1: Confidential AC/AUG 2015/MAF253Bonna Della TianamNessuna valutazione finora

- Gann Intraday CalculatorDocumento2 pagineGann Intraday CalculatorSanjay PuriNessuna valutazione finora

- A PROJECT REPORT On "Kotak Mahindra Mutul Fund"Documento69 pagineA PROJECT REPORT On "Kotak Mahindra Mutul Fund"jai786063% (16)

- Investment Management TLPDocumento5 pagineInvestment Management TLPGayathri VijayakumarNessuna valutazione finora

- Relevant Provisions of Companies ActDocumento19 pagineRelevant Provisions of Companies Actrthi04Nessuna valutazione finora

- 3 Day CycleDocumento27 pagine3 Day Cyclemohamedkeynan99Nessuna valutazione finora

- Capra Breadth Internal Indicators For Winning Swing and Posistion Trading ManualDocumento58 pagineCapra Breadth Internal Indicators For Winning Swing and Posistion Trading ManualVarun VasurendranNessuna valutazione finora

- Busi431 - Formative Assessment 1Documento4 pagineBusi431 - Formative Assessment 1hamzaNessuna valutazione finora

- Features of Equity SharesDocumento4 pagineFeatures of Equity SharesAnkita Modi100% (1)

- International Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Documento20 pagineInternational Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Chintakunta PreethiNessuna valutazione finora

- UFCE - Annex 1 &2Documento8 pagineUFCE - Annex 1 &2Salil NagvekarNessuna valutazione finora

- Vinamilk (Damodaran 2018) PDFDocumento201 pagineVinamilk (Damodaran 2018) PDFPi PewdsNessuna valutazione finora

- Securities Law PDFDocumento7 pagineSecurities Law PDFGabril AsadeNessuna valutazione finora

- Summer Internship Project Synopsis ON "Capital Investment & Stock Return"Documento11 pagineSummer Internship Project Synopsis ON "Capital Investment & Stock Return"rinkeshNessuna valutazione finora

- Stock Investing Mastermind - Zebra Learn-165Documento2 pagineStock Investing Mastermind - Zebra Learn-165RGNitinDevaNessuna valutazione finora

- Final Exam SolutionsDocumento3 pagineFinal Exam Solutionsceo.spammableNessuna valutazione finora

- Portfolio Management Theory and ApplicatDocumento572 paginePortfolio Management Theory and ApplicatsmatiNessuna valutazione finora

- AdrDocumento10 pagineAdrvahid100% (1)

- Hedge-Fund World's One-Man Wealth Machine - WSJDocumento4 pagineHedge-Fund World's One-Man Wealth Machine - WSJDamon Meng100% (1)

- IFRS Metodo Del Derivado HipoteticoDocumento12 pagineIFRS Metodo Del Derivado HipoteticoEdgar Ramon Guillen VallejoNessuna valutazione finora

- International Financial Management 12Th by Jeff Madura Full ChapterDocumento41 pagineInternational Financial Management 12Th by Jeff Madura Full Chapterstephanie.selestewa674100% (23)

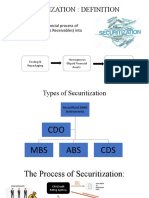

- SECURITIZATIONDocumento5 pagineSECURITIZATIONASHISH KUMARNessuna valutazione finora