Potrebbero piacerti anche

- Accounting Policies and Procedures Manual: A Blueprint for Running an Effective and Efficient DepartmentDa EverandAccounting Policies and Procedures Manual: A Blueprint for Running an Effective and Efficient DepartmentNessuna valutazione finora

- Introduction To Transaction ProcessingDocumento23 pagineIntroduction To Transaction ProcessingAngel Cauilan100% (1)

- The General Ledger and Reporting CycleDocumento12 pagineThe General Ledger and Reporting CycleNHNessuna valutazione finora

- Chapter 2 PPT (AIS - James Hall)Documento5 pagineChapter 2 PPT (AIS - James Hall)Nur-aima MortabaNessuna valutazione finora

- Ch8-Financial Reporting & Management Reporting SystemsDocumento78 pagineCh8-Financial Reporting & Management Reporting SystemsMaxene PigtainNessuna valutazione finora

- General Ledger Department: Introduction and Overview Definition: TheDocumento29 pagineGeneral Ledger Department: Introduction and Overview Definition: Thekanwal1234Nessuna valutazione finora

- Introduction To Transaction Processing: Dr. Hisham MadiDocumento35 pagineIntroduction To Transaction Processing: Dr. Hisham Madiziade roalesNessuna valutazione finora

- Chapter TwoDocumento42 pagineChapter Twohasan jabrNessuna valutazione finora

- Wk2 1Documento43 pagineWk2 1Queenie AlgireNessuna valutazione finora

- Chapter 8 AISDocumento42 pagineChapter 8 AISNica VizcondeNessuna valutazione finora

- BBP FI 02 General Ledger Accounting v.0Documento14 pagineBBP FI 02 General Ledger Accounting v.0shailendra kumarNessuna valutazione finora

- SAP FICO General Ledger Enduser Training HTTP Sapdocs InfoDocumento80 pagineSAP FICO General Ledger Enduser Training HTTP Sapdocs InfoBala RanganathNessuna valutazione finora

- Chapter 1 A Model For Processing AIS (New)Documento6 pagineChapter 1 A Model For Processing AIS (New)Muhammad IrshadNessuna valutazione finora

- Lakshmi Sampath OAUG 2011Documento51 pagineLakshmi Sampath OAUG 2011lakshram143Nessuna valutazione finora

- Financial Reporting and Management Reporting System NotesDocumento7 pagineFinancial Reporting and Management Reporting System NotesJoana TrinidadNessuna valutazione finora

- Chapter 2 Introduction To Transaction Processing AISDocumento5 pagineChapter 2 Introduction To Transaction Processing AISKen Ivan HervasNessuna valutazione finora

- Tutorial 3 ACCTDocumento10 pagineTutorial 3 ACCTKhánh Linh CaoNessuna valutazione finora

- Financials Reports R13 (Version 1)Documento101 pagineFinancials Reports R13 (Version 1)MohammadSharawyNessuna valutazione finora

- At The End of The Accounting PeriodDocumento16 pagineAt The End of The Accounting PeriodAra ArinqueNessuna valutazione finora

- RTRDocumento4 pagineRTRDANIELNessuna valutazione finora

- Chapter 02 Introduction To Transaction Processing.: Presented byDocumento46 pagineChapter 02 Introduction To Transaction Processing.: Presented byjelNessuna valutazione finora

- Accounting Information System Chapter 8Documento45 pagineAccounting Information System Chapter 8Cassie100% (4)

- Accounting Cycle For A Merchandising Business The Basic Accounting CycleDocumento4 pagineAccounting Cycle For A Merchandising Business The Basic Accounting CycleEloizaMarieNessuna valutazione finora

- Accounting Information Systems 6 TH Edition JamesDocumento86 pagineAccounting Information Systems 6 TH Edition JameswawanNessuna valutazione finora

- BR Erp GLDocumento8 pagineBR Erp GLifyunalorNessuna valutazione finora

- SAP FI OverviewDocumento16 pagineSAP FI OverviewManoj Kumar100% (1)

- Oracle EBS Release 12 Features: Ramsubramani Amravaneswaren Bhupesh Bajaj Mark Dietrich Niranjan Rao Jeff SpearinDocumento77 pagineOracle EBS Release 12 Features: Ramsubramani Amravaneswaren Bhupesh Bajaj Mark Dietrich Niranjan Rao Jeff SpearinNRK Murthy100% (1)

- Income - Used in Connection With The Inflow of AssetsDocumento4 pagineIncome - Used in Connection With The Inflow of AssetsKimberly FloresNessuna valutazione finora

- Chapter 16 (GENERAL LEDGER AND REPORTING SYSTEM)Documento7 pagineChapter 16 (GENERAL LEDGER AND REPORTING SYSTEM)Amara Prabasari100% (1)

- Accounting Basics 16-10-11Documento157 pagineAccounting Basics 16-10-11hud ameenNessuna valutazione finora

- IIMB Term1 PGP Chapter3Documento14 pagineIIMB Term1 PGP Chapter3Arun SaktheeshNessuna valutazione finora

- of Tally PresentationDocumento79 pagineof Tally PresentationSandip JadavNessuna valutazione finora

- Dheeraj Brochure V2Documento5 pagineDheeraj Brochure V2Liaqut Ali KhanNessuna valutazione finora

- Chapter 2 Intro To Transaction ProcessingDocumento55 pagineChapter 2 Intro To Transaction ProcessingCyril DE LA VEGANessuna valutazione finora

- Ch2-Introduction To Transaction ProcessingDocumento69 pagineCh2-Introduction To Transaction ProcessingMaxene PigtainNessuna valutazione finora

- Intermediate Accounting 19th Edition Stice Solutions ManualDocumento35 pagineIntermediate Accounting 19th Edition Stice Solutions Manualpassagevoyagera5cnhd100% (24)

- 1dd472d8-3b87-4940-be3a-9d676384377cDocumento19 pagine1dd472d8-3b87-4940-be3a-9d676384377cmakouapenda2000Nessuna valutazione finora

- Business Transactions - Chapter 2: Steps in The Accounting Cycle Accounting RecordsDocumento9 pagineBusiness Transactions - Chapter 2: Steps in The Accounting Cycle Accounting RecordssnowiieeNessuna valutazione finora

- Ais Module 3Documento13 pagineAis Module 3Maxine ConstantinoNessuna valutazione finora

- FIN201 Fundamentals Finance Part 3 BookletDocumento10 pagineFIN201 Fundamentals Finance Part 3 BookletThulani NdlovuNessuna valutazione finora

- Overview of Financial Accounting in SAPDocumento31 pagineOverview of Financial Accounting in SAPyashghodke83Nessuna valutazione finora

- Chapter 2 AISDocumento3 pagineChapter 2 AISgailmissionNessuna valutazione finora

- Agenda of GL WorkshopsDocumento2 pagineAgenda of GL WorkshopsZill HumaNessuna valutazione finora

- S4 PPTDocumento9 pagineS4 PPTAmrutaNessuna valutazione finora

- Tutorial 2 Chapter2 Foundational Concepts of The AisDocumento10 pagineTutorial 2 Chapter2 Foundational Concepts of The AisWael AyariNessuna valutazione finora

- Chapter 2 and 3Documento36 pagineChapter 2 and 3kirbydegay1028Nessuna valutazione finora

- PDF&Rendition 1Documento25 paginePDF&Rendition 1nitin jaulkarNessuna valutazione finora

- Fusion Setups-1Documento28 pagineFusion Setups-1Vidya Sagar100% (1)

- Basic AccountingDocumento1 paginaBasic AccountingLyka FaneNessuna valutazione finora

- Partial Payment & Residual Payment ...Documento17 paginePartial Payment & Residual Payment ...Ahmed ElhawaryNessuna valutazione finora

- EBS R12 FinancialsDocumento38 pagineEBS R12 FinancialsNarumon SrisuwanNessuna valutazione finora

- ACTG 21B (CH3) - Lecture NotesDocumento4 pagineACTG 21B (CH3) - Lecture Notesraimefaye seduconNessuna valutazione finora

- Record To ReportDocumento3 pagineRecord To ReportNaresh KumarNessuna valutazione finora

- 04 JournalEntrytoPeriodCloseDocumento33 pagine04 JournalEntrytoPeriodClosegpcrao143Nessuna valutazione finora

- BAAE 12-BSAC 1B AssignmentDocumento2 pagineBAAE 12-BSAC 1B AssignmentjepsyutNessuna valutazione finora

- GSI Fusion Receivables - AR To GL Reconciliation (R11D02)Documento10 pagineGSI Fusion Receivables - AR To GL Reconciliation (R11D02)Andreea GeorgianaNessuna valutazione finora

- BBP - FI - 006 - Document SplittingDocumento6 pagineBBP - FI - 006 - Document SplittingPrem PrakashNessuna valutazione finora

- Chapter 2 INTRODUCTION TO TRANSACTION PROCESSINGDocumento14 pagineChapter 2 INTRODUCTION TO TRANSACTION PROCESSINGXela Mae BigorniaNessuna valutazione finora

- SAP FI Account Payable APDocumento91 pagineSAP FI Account Payable APahmed shomanNessuna valutazione finora

- g10 Music 3rd Page 2Documento1 paginag10 Music 3rd Page 2Kent CondinoNessuna valutazione finora

- 4 Cash and Cash Equivalents. Bank Recon. Proof of Cash - ReceivablesDocumento11 pagine4 Cash and Cash Equivalents. Bank Recon. Proof of Cash - ReceivablesKent CondinoNessuna valutazione finora

- Facts of CheerleadingDocumento1 paginaFacts of CheerleadingKent CondinoNessuna valutazione finora

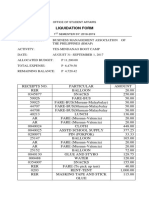

- Liquidation Form: Office of Student AffairsDocumento3 pagineLiquidation Form: Office of Student AffairsKent CondinoNessuna valutazione finora

- Reviewers and ScheduleDocumento1 paginaReviewers and ScheduleKent CondinoNessuna valutazione finora

- Chapter 1 and 2Documento16 pagineChapter 1 and 2Kent CondinoNessuna valutazione finora

- Chapter VDocumento4 pagineChapter VKent CondinoNessuna valutazione finora

- Vetsci00118 0006Documento1 paginaVetsci00118 0006Kent CondinoNessuna valutazione finora

- Cash and Cash Equivalents Audit Procedures CONDINODocumento11 pagineCash and Cash Equivalents Audit Procedures CONDINOKent CondinoNessuna valutazione finora

- Computation For Formation of PartnershipDocumento10 pagineComputation For Formation of PartnershipErille Julianne (Rielianne)Nessuna valutazione finora

- Balance of Payment AdjustmentDocumento37 pagineBalance of Payment AdjustmentJash ShethiaNessuna valutazione finora

- Isc 2017 BQPDocumento25 pagineIsc 2017 BQPPANKAJ's ACCOUNTANCY PATHSHALANessuna valutazione finora

- Kunci JWB pkt2. 3 PDsuburDocumento45 pagineKunci JWB pkt2. 3 PDsuburSyifa FaNessuna valutazione finora

- FABM1 Q4 Module 14Documento15 pagineFABM1 Q4 Module 14Earl Christian BonaobraNessuna valutazione finora

- Long-Term Construction Contracts and FranchisingDocumento16 pagineLong-Term Construction Contracts and FranchisingAlexis SosingNessuna valutazione finora

- Ch14 Long Term LiabilitiesDocumento39 pagineCh14 Long Term LiabilitiesBabi Dimaano Navarez67% (3)

- Admission of A PartnerDocumento5 pagineAdmission of A PartnerTimothy BrownNessuna valutazione finora

- 21936mtp Cptvolu1 Part4Documento404 pagine21936mtp Cptvolu1 Part4Arun KCNessuna valutazione finora

- 3 PDFDocumento4 pagine3 PDFDarius DelacruzNessuna valutazione finora

- 5 CC 82 AafDocumento2 pagine5 CC 82 Aafdae ChoNessuna valutazione finora

- CARO, 2003-: (As Amended by The CARO Amendment Order 2004)Documento19 pagineCARO, 2003-: (As Amended by The CARO Amendment Order 2004)Rishabh GuptaNessuna valutazione finora

- Counseling Fee Payment ProcedureDocumento3 pagineCounseling Fee Payment ProcedureabhishekNessuna valutazione finora

- Dayna Mclaughlin: Debit Account Transactions Date Description Type Amount Available Matthew SteversonDocumento4 pagineDayna Mclaughlin: Debit Account Transactions Date Description Type Amount Available Matthew SteversonPatty Morrarty24Nessuna valutazione finora

- AccountingDocumento5 pagineAccountingIhsan UllahNessuna valutazione finora

- ANSWERDocumento10 pagineANSWERGab IgnacioNessuna valutazione finora

- Listed Below Are Roughly 70 Multiple Choice Governmental and Not For Profit Accounting QuestionsDocumento17 pagineListed Below Are Roughly 70 Multiple Choice Governmental and Not For Profit Accounting Questionsrio100% (3)

- Journal, T Accounts, TrialDocumento14 pagineJournal, T Accounts, TrialJasmine ActaNessuna valutazione finora

- Intermediate 1-Assessment ExamDocumento20 pagineIntermediate 1-Assessment ExamAllen KateNessuna valutazione finora

- Akuntansi - Accounting Information SystemDocumento50 pagineAkuntansi - Accounting Information SystemArif YuliantoNessuna valutazione finora

- Solution Manual Advanced Financial Accounting 8th Edition Baker Chap015 PDFDocumento54 pagineSolution Manual Advanced Financial Accounting 8th Edition Baker Chap015 PDFYopie ChandraNessuna valutazione finora

- Electronic Payment Systems-FinalDocumento105 pagineElectronic Payment Systems-FinalDileep VkNessuna valutazione finora

- Budgeting BasicsDocumento21 pagineBudgeting BasicsMish AlontoNessuna valutazione finora

- BASIC ACCO Simulated MidtermDocumento10 pagineBASIC ACCO Simulated MidtermistepNessuna valutazione finora

- 3 Partnership AccountsDocumento93 pagine3 Partnership AccountsCA K D Purkayastha100% (1)

- Virtual University Presents: Slide 1 / 69Documento69 pagineVirtual University Presents: Slide 1 / 69mba departmentNessuna valutazione finora

- Module 8 Special and Combination Journals, and Voucher SystemDocumento64 pagineModule 8 Special and Combination Journals, and Voucher SystemMCM EnterpriseNessuna valutazione finora

- CH 2Documento4 pagineCH 2ايهاب غزالةNessuna valutazione finora

- STD 11 Book Keeping and AccountancyDocumento18 pagineSTD 11 Book Keeping and AccountancyRam IyerNessuna valutazione finora

- Basics of Variance Calculation-UnderstandingDocumento6 pagineBasics of Variance Calculation-Understandingkhalidmahmoodqumar0% (1)