Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Air India - Balance Score CardDocumento6 pagineAir India - Balance Score Cardramyavenugopal100% (1)

- Super Injunction BookDocumento3 pagineSuper Injunction BookReckless Kobold0% (1)

- Forex Trend Line Strategy Note For Advance TraderDocumento82 pagineForex Trend Line Strategy Note For Advance TraderMohd Ridzuan100% (2)

- Appendix 8 - Instructions - RAPALDocumento1 paginaAppendix 8 - Instructions - RAPALTesa GDNessuna valutazione finora

- Masan Group CorporationDocumento31 pagineMasan Group Corporationhồ nam longNessuna valutazione finora

- Avro RJ General Data Brochure PDFDocumento66 pagineAvro RJ General Data Brochure PDFMonica Enin100% (2)

- PinoyDocumento5 paginePinoyLarete PaoloNessuna valutazione finora

- Jack Daniel'sDocumento17 pagineJack Daniel'sIon TarlevNessuna valutazione finora

- Antwoordblad Instaptoets EngelsDocumento4 pagineAntwoordblad Instaptoets EngelskadpoortNessuna valutazione finora

- Magazine Still Holds True With Its Mission Statement-Dedicated To The Growth of TheDocumento5 pagineMagazine Still Holds True With Its Mission Statement-Dedicated To The Growth of TheRush YuviencoNessuna valutazione finora

- Capital StructureDocumento44 pagineCapital Structure26155152Nessuna valutazione finora

- Tourism PolicyDocumento6 pagineTourism Policylanoox0% (1)

- English Listening MaterialsDocumento3 pagineEnglish Listening MaterialsVita NovitasariNessuna valutazione finora

- TWSS CFA Level I - Planner and TrackerDocumento6 pagineTWSS CFA Level I - Planner and TrackerSai Ranjit TummalapalliNessuna valutazione finora

- Key Points in Creation of Huf and Format of Deed For Creation of HufDocumento5 pagineKey Points in Creation of Huf and Format of Deed For Creation of HufGopalakrishna SrinivasanNessuna valutazione finora

- Break Even Point ExplanationDocumento2 pagineBreak Even Point ExplanationEdgar IbarraNessuna valutazione finora

- Indifference CurveDocumento16 pagineIndifference Curveএস. এম. তানজিলুল ইসলামNessuna valutazione finora

- Short AnswerDocumento4 pagineShort AnswerMichiko Kyung-soonNessuna valutazione finora

- Rufino Tan Vs Ramon Del RosarioDocumento1 paginaRufino Tan Vs Ramon Del RosarioJocelyn MagbanuaNessuna valutazione finora

- Sap MM Standard Business ProcessesDocumento65 pagineSap MM Standard Business ProcessesDipak BanerjeeNessuna valutazione finora

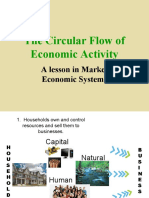

- Circular FlowDocumento21 pagineCircular FlowSheryl BorromeoNessuna valutazione finora

- Best Practices in Hotel Financial ManagementDocumento3 pagineBest Practices in Hotel Financial ManagementDhruv BansalNessuna valutazione finora

- StartUp India - Case AnalysisDocumento3 pagineStartUp India - Case AnalysisIrshad AzeezNessuna valutazione finora

- Cash Flows From Operating ActivitiesDocumento5 pagineCash Flows From Operating ActivitiesIrfan MansoorNessuna valutazione finora

- Walt Disney Company PDFDocumento20 pagineWalt Disney Company PDFGabriella VenturinaNessuna valutazione finora

- Agriculture Subsidies and DevelopmentDocumento2 pagineAgriculture Subsidies and Developmentbluerockwalla100% (2)

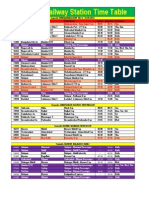

- Solapur Railway Station Time TableDocumento2 pagineSolapur Railway Station Time TableAndrea Lopez33% (3)

- Tennis Ball Activity - Diminishing Returns - Notes - 3Documento1 paginaTennis Ball Activity - Diminishing Returns - Notes - 3Raghvi AryaNessuna valutazione finora

- Bangkok Retail 4q13Documento1 paginaBangkok Retail 4q13Bea LorinczNessuna valutazione finora