Potrebbero piacerti anche

- Banking and Financial Institutions Chapter 5Documento34 pagineBanking and Financial Institutions Chapter 5Lorena100% (1)

- Chapter 5 Bank Credit InstrumentsDocumento5 pagineChapter 5 Bank Credit InstrumentsMariel Crista Celda Maravillosa100% (2)

- Credit Instruments Power PointDocumento11 pagineCredit Instruments Power PointEd Leen Ü80% (10)

- Credit and Collection Lecture 3Documento25 pagineCredit and Collection Lecture 3Jackie RaborarNessuna valutazione finora

- Chapter 6 & 7 - Credit and Collection ReportDocumento25 pagineChapter 6 & 7 - Credit and Collection Reportshairalee201475% (4)

- Credit and Collection 2Documento8 pagineCredit and Collection 2Jaimee VelchezNessuna valutazione finora

- Examples of Credit InstrumentsDocumento35 pagineExamples of Credit Instrumentsjessica anne100% (1)

- Fima30063-Lect1-Overview of CreditDocumento24 pagineFima30063-Lect1-Overview of CreditNicole Lanorio100% (1)

- Introduction of Loan PortfolioDocumento2 pagineIntroduction of Loan PortfolioGaurav SharmaNessuna valutazione finora

- Banking and Financial Institutions Chapter 3Documento32 pagineBanking and Financial Institutions Chapter 3Lorena100% (1)

- Source of CreditDocumento2 pagineSource of Creditkhaireyah hashim100% (1)

- Collection Calendar, Role of Collectors in Business, and Cash On Delivery (COD)Documento49 pagineCollection Calendar, Role of Collectors in Business, and Cash On Delivery (COD)marife100% (1)

- Loan and Discount FunctionsDocumento2 pagineLoan and Discount FunctionsMegan Adeline Hale100% (2)

- Credit and Collection ActivityDocumento4 pagineCredit and Collection ActivityAngelouNessuna valutazione finora

- Credit & Collection + Capital MarketDocumento8 pagineCredit & Collection + Capital MarketMilky CoffeeNessuna valutazione finora

- Regulation and Supervision of Financial InstitutionsDocumento43 pagineRegulation and Supervision of Financial Institutionskim byunooNessuna valutazione finora

- CHAPTER 1 - The Nature and Role of CreditDocumento4 pagineCHAPTER 1 - The Nature and Role of Creditdoray100% (1)

- FM16 Credit and Collection Semi-FinalDocumento22 pagineFM16 Credit and Collection Semi-FinalMark Anthony Jr. Yanson100% (2)

- The Philippine Financial System and International Business FinanceDocumento18 pagineThe Philippine Financial System and International Business Financejames100% (1)

- 1 Meaning Classification Nature and Function of CreditDocumento7 pagine1 Meaning Classification Nature and Function of CreditMartije MonesaNessuna valutazione finora

- Chapter 1 of The Book Credit and Collection MGT by Jose Glenn Briones Sr.Documento43 pagineChapter 1 of The Book Credit and Collection MGT by Jose Glenn Briones Sr.Ruvelyn Lenares75% (4)

- Credit and CollectionDocumento21 pagineCredit and CollectionMara Pancho75% (4)

- Credit InstrumentsDocumento12 pagineCredit InstrumentsDplis UsjrNessuna valutazione finora

- Thrift Bank Vs Commercial BankDocumento4 pagineThrift Bank Vs Commercial Bankfaranmalik0% (1)

- Collection Policies and Procedures PrintedDocumento10 pagineCollection Policies and Procedures PrintedCarl Joseph Ninobla JosueNessuna valutazione finora

- BSPDocumento11 pagineBSPMeloy ApiladoNessuna valutazione finora

- Banking and Financial InstitutionDocumento25 pagineBanking and Financial InstitutionAlgie PlondayaNessuna valutazione finora

- Credit and Collection - IntroductionDocumento9 pagineCredit and Collection - IntroductionRonnel Aldin Fernando33% (9)

- 1 The Nature and Functions of Credit.Documento16 pagine1 The Nature and Functions of Credit.weddiemae villarizaNessuna valutazione finora

- FM 8 Module 2 Multinational Financial ManagementDocumento35 pagineFM 8 Module 2 Multinational Financial ManagementJasper Mortos VillanuevaNessuna valutazione finora

- Chapter 10 Bank ReservesDocumento5 pagineChapter 10 Bank ReservesMariel Crista Celda MaravillosaNessuna valutazione finora

- Credit and Collection - 081517Documento21 pagineCredit and Collection - 081517Nerissa100% (2)

- Week 13-15 Collection, Remedial Management, Credit ReviewDocumento9 pagineWeek 13-15 Collection, Remedial Management, Credit ReviewAkii WingNessuna valutazione finora

- Bank Supervision and Examination FinalDocumento56 pagineBank Supervision and Examination FinalKhaizar Moi OlaldeNessuna valutazione finora

- Logos of Central Bank of The Philippines and Bangko Sentral NG PilipinasDocumento16 pagineLogos of Central Bank of The Philippines and Bangko Sentral NG Pilipinaslaerham50% (2)

- The Credit SystemDocumento6 pagineThe Credit SystemJamil MacabandingNessuna valutazione finora

- Chapter 8 Deposit FunctionDocumento5 pagineChapter 8 Deposit FunctionMariel Crista Celda MaravillosaNessuna valutazione finora

- Principles of CreditDocumento16 paginePrinciples of CreditRonnel Aldin Fernando80% (5)

- Banking and Financial Institutions Module5Documento14 pagineBanking and Financial Institutions Module5bad genius100% (1)

- Banking and Financial InstitutionDocumento48 pagineBanking and Financial InstitutionMylene Orain SevillaNessuna valutazione finora

- 5 A Credit and Collection LetterDocumento33 pagine5 A Credit and Collection LetterEj AguilarNessuna valutazione finora

- Course Code and Title: Lesson Number: Topic: Anti Money Laundering (AML) ProfessorDocumento7 pagineCourse Code and Title: Lesson Number: Topic: Anti Money Laundering (AML) ProfessorJha Jha CaLvezNessuna valutazione finora

- Chapter 4 Purpose of Examination and SupervisionDocumento5 pagineChapter 4 Purpose of Examination and SupervisionMariel Crista Celda MaravillosaNessuna valutazione finora

- Classification of CreditDocumento3 pagineClassification of CreditMD. IBRAHIM KHOLILULLAH100% (1)

- Chapter 7 Commercial BanksDocumento7 pagineChapter 7 Commercial BanksMariel Crista Celda Maravillosa100% (1)

- Module OneDocumento95 pagineModule OneJoana Marie CabuteNessuna valutazione finora

- An Introduction To Money and The Financial System: Chapter OverviewDocumento13 pagineAn Introduction To Money and The Financial System: Chapter Overviewmyungjin mjinNessuna valutazione finora

- Lesson 3 - Credit ProcessDocumento6 pagineLesson 3 - Credit ProcessRachel Ann RazonableNessuna valutazione finora

- Report On Debt ManagementDocumento79 pagineReport On Debt ManagementSiddharth Mehta100% (1)

- Credit C7Documento14 pagineCredit C7Chantelle Ishi Macatangay AquinoNessuna valutazione finora

- Different Classifications of BanksDocumento48 pagineDifferent Classifications of BanksNash DenverNessuna valutazione finora

- Final Examination INVESTMENT AND PORTFOLIO MANAGEMENTDocumento2 pagineFinal Examination INVESTMENT AND PORTFOLIO MANAGEMENTRemar Allen Bautista100% (1)

- FMPR3 Banking and Financial Institutions MergedDocumento36 pagineFMPR3 Banking and Financial Institutions MergedErika Mae JaranillaNessuna valutazione finora

- Credit and Collection 1Documento4 pagineCredit and Collection 1Jaimee Velchez67% (3)

- Universal BankDocumento1 paginaUniversal Bankhailene lorenaNessuna valutazione finora

- Collection Policies and ProceduresDocumento15 pagineCollection Policies and ProceduresAlyza TorresNessuna valutazione finora

- Monetary Policy and Central Banking in The PhilippinesDocumento29 pagineMonetary Policy and Central Banking in The PhilippinesYogun BayonaNessuna valutazione finora

- Ch5-Credit and Collection PolicyDocumento59 pagineCh5-Credit and Collection PolicyWilsonNessuna valutazione finora

- Tahir KhanDocumento10 pagineTahir KhantahirkkkNessuna valutazione finora

- #02 - Service Products of BanksDocumento9 pagine#02 - Service Products of BanksiitbhuNessuna valutazione finora

- Deposit Function PDFDocumento75 pagineDeposit Function PDFrojon pharmacyNessuna valutazione finora

- Rojon Opening and Closing PrayerDocumento2 pagineRojon Opening and Closing Prayerrojon pharmacy100% (1)

- Risk Management PlanDocumento2 pagineRisk Management Planrojon pharmacy100% (2)

- Risk Management PlanDocumento2 pagineRisk Management Planrojon pharmacy84% (37)

- Rojon PharmacyDocumento1 paginaRojon Pharmacyrojon pharmacyNessuna valutazione finora

- Islamic BankingDocumento50 pagineIslamic Bankingmusbri mohamed100% (2)

- CP 3Documento14 pagineCP 3aaapppaaapppNessuna valutazione finora

- Number: CIPT Passing Score: 800 Time Limit: 120 Min File Version: 1Documento30 pagineNumber: CIPT Passing Score: 800 Time Limit: 120 Min File Version: 1Mohamed Fazila Abd RahmanNessuna valutazione finora

- Causation in Tort LawDocumento16 pagineCausation in Tort LawAayush KumarNessuna valutazione finora

- My Phillips Family 000-010Documento138 pagineMy Phillips Family 000-010Joni Coombs-HaynesNessuna valutazione finora

- Positive Role The Indian Youth Can Play in PoliticsDocumento2 paginePositive Role The Indian Youth Can Play in PoliticsArul ChamariaNessuna valutazione finora

- AMLA SingaporeDocumento105 pagineAMLA SingaporeturkeypmNessuna valutazione finora

- II Fdi IIDocumento16 pagineII Fdi IIsakshi tiwariNessuna valutazione finora

- Business Name Registration Process FlowDocumento2 pagineBusiness Name Registration Process FlowJulius Espiga ElmedorialNessuna valutazione finora

- Syllab of Dip in Life Ins UnderwritingDocumento17 pagineSyllab of Dip in Life Ins Underwritinganon_303912439100% (1)

- Business Math - W3 - Gross and Net EarningsDocumento5 pagineBusiness Math - W3 - Gross and Net Earningscj100% (1)

- 1.2 Internal Control and RiskDocumento84 pagine1.2 Internal Control and Riskadrian100% (1)

- Ei 1529Documento43 pagineEi 1529milecsa100% (1)

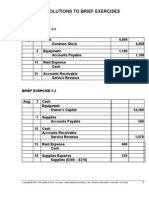

- Self Study Solutions Chapter 3Documento27 pagineSelf Study Solutions Chapter 3flowerkmNessuna valutazione finora

- Accounting BusinessDocumento11 pagineAccounting BusinessLyndonNessuna valutazione finora

- VoetpadkloofDocumento1 paginaVoetpadkloofRia VisagieNessuna valutazione finora

- Direct Shear Test ReprtDocumento4 pagineDirect Shear Test ReprtShivaraj SubramaniamNessuna valutazione finora

- Technical Data - LUPOLEN 5261 ZDocumento3 pagineTechnical Data - LUPOLEN 5261 ZCristhian Huanqui TapiaNessuna valutazione finora

- While WeDocumento4 pagineWhile WeAhmed S. MubarakNessuna valutazione finora

- Ha Ovirt IscsiDocumento28 pagineHa Ovirt IscsizennroNessuna valutazione finora

- Roan v. Gonzales, 145 SCRA 687Documento2 pagineRoan v. Gonzales, 145 SCRA 687Katrina Anne Layson YeenNessuna valutazione finora

- De Jesus vs. Aquino GR No.164662Documento11 pagineDe Jesus vs. Aquino GR No.164662Anabelle C. AvenidoNessuna valutazione finora

- Trafalgar Square: World Council For Corporate GovernanceDocumento2 pagineTrafalgar Square: World Council For Corporate GovernanceJohn Adam St Gang: Crown Control100% (1)

- (LLOYD) Law of Conservation of Linear MomentumDocumento9 pagine(LLOYD) Law of Conservation of Linear MomentumHideous PikaNessuna valutazione finora

- Balance Sheet of Tata Power Company: - in Rs. Cr.Documento3 pagineBalance Sheet of Tata Power Company: - in Rs. Cr.ashishrajmakkarNessuna valutazione finora

- Ilnas-En Iso 17665-1:2006Documento8 pagineIlnas-En Iso 17665-1:2006BakeWizretNessuna valutazione finora

- GST Invoice: SL No. 1 2.000 KG. 2 2.000 KGDocumento2 pagineGST Invoice: SL No. 1 2.000 KG. 2 2.000 KGDNYANESHWAR PAWARNessuna valutazione finora

- E Commerce Notes Chapter 5-10Documento5 pagineE Commerce Notes Chapter 5-10Taniya Bhalla100% (1)

- Payslip 104883 112021Documento1 paginaPayslip 104883 112021arvindNessuna valutazione finora

- Declaration of Security Between A Vessel and A Marine Facility (Canada)Documento3 pagineDeclaration of Security Between A Vessel and A Marine Facility (Canada)Steve Yh HuangNessuna valutazione finora