Potrebbero piacerti anche

- Strong Knot Inc A Service Company Performs Adjusting Entries MonthlyDocumento2 pagineStrong Knot Inc A Service Company Performs Adjusting Entries MonthlyAmit PandeyNessuna valutazione finora

- Final Exam BSC 2nd 2020Documento3 pagineFinal Exam BSC 2nd 2020NadeemNessuna valutazione finora

- Chapter 20 Accounting For State and Local Governmental Units - Proprietary and Fiduciary FundsDocumento34 pagineChapter 20 Accounting For State and Local Governmental Units - Proprietary and Fiduciary FundsFauzi AchmadNessuna valutazione finora

- M1 - A3 Calculating Inventory - Finlon Upholstery IncDocumento3 pagineM1 - A3 Calculating Inventory - Finlon Upholstery Inczb83100% (1)

- Cost AccountingDocumento43 pagineCost AccountingAmina QamarNessuna valutazione finora

- Financial Accounting Theory Craig Deegan Chapter 2Documento34 pagineFinancial Accounting Theory Craig Deegan Chapter 2Siti AdawiyahNessuna valutazione finora

- AUD Southampton PLCDocumento3 pagineAUD Southampton PLCAivie Pangilinan0% (1)

- Topic 12 - Financial - Statement - AnalysisDocumento64 pagineTopic 12 - Financial - Statement - AnalysisdenixngNessuna valutazione finora

- Chapter 4 SolutionsDocumento12 pagineChapter 4 SolutionsSoshiNessuna valutazione finora

- Activity No 1Documento2 pagineActivity No 1Makeyc Stis100% (1)

- Final Exam, s1, 2019 FINALDocumento12 pagineFinal Exam, s1, 2019 FINALShivneel NaiduNessuna valutazione finora

- Debited The Asset Supplies. This Account Shows A Debited The Account Supplies Expense. ThisDocumento4 pagineDebited The Asset Supplies. This Account Shows A Debited The Account Supplies Expense. ThiszairahNessuna valutazione finora

- Sallys Struthers - Answer KeyDocumento7 pagineSallys Struthers - Answer KeyLlyod Francis LaylayNessuna valutazione finora

- Module 6 - Worksheet and Financial Statements Part IDocumento12 pagineModule 6 - Worksheet and Financial Statements Part IMJ San Pedro100% (1)

- SMChap 017Documento35 pagineSMChap 017testbank100% (6)

- Jerrison Company Operates A Wholesale Hardware Business The FolDocumento1 paginaJerrison Company Operates A Wholesale Hardware Business The FolM Bilal SaleemNessuna valutazione finora

- CFI 3 Statement Model Complete in ClassDocumento10 pagineCFI 3 Statement Model Complete in ClassThiện NhânNessuna valutazione finora

- Soal P 7.2, 7.3, 7.5Documento3 pagineSoal P 7.2, 7.3, 7.5boba milkNessuna valutazione finora

- Chapter 9 - Budgeting1Documento27 pagineChapter 9 - Budgeting1Martinus WarsitoNessuna valutazione finora

- FSA Course Pack Before Mid Balance Sheet PDFDocumento16 pagineFSA Course Pack Before Mid Balance Sheet PDFRehman RajpootNessuna valutazione finora

- Financial Accounting (Unsolved Papers of ICMAP)Documento48 pagineFinancial Accounting (Unsolved Papers of ICMAP)Platonic0% (1)

- Chap 5 Accounting For Merchandising OperationDocumento71 pagineChap 5 Accounting For Merchandising OperationtamimNessuna valutazione finora

- Work Book Unit 2 Proforma Variation - SolvedDocumento12 pagineWork Book Unit 2 Proforma Variation - SolvedZaheer SwatiNessuna valutazione finora

- CH 12 Irrecoverable Debts and Allowance v3Documento8 pagineCH 12 Irrecoverable Debts and Allowance v3BuntheaNessuna valutazione finora

- Quiz 5 - QuesDocumento14 pagineQuiz 5 - QuesPhán Tiêu TiềnNessuna valutazione finora

- Excercises MerchandisingDocumento4 pagineExcercises MerchandisingRenz AbadNessuna valutazione finora

- Basic Financial Accounting PPT 1Documento26 pagineBasic Financial Accounting PPT 1anon_254280391100% (1)

- JOB, BATCH AND SERVICE COSTING-lesson 11Documento22 pagineJOB, BATCH AND SERVICE COSTING-lesson 11Kj NayeeNessuna valutazione finora

- Gross Profit AnalysisDocumento5 pagineGross Profit AnalysisInayat Ur RehmanNessuna valutazione finora

- Week Seven - Translation of Foreign Currency Financial StatementsDocumento28 pagineWeek Seven - Translation of Foreign Currency Financial StatementsCoffee JellyNessuna valutazione finora

- 3, Fa1 Question Book 2021 (Gen 5) - G I Cho Sinh ViênDocumento76 pagine3, Fa1 Question Book 2021 (Gen 5) - G I Cho Sinh ViênHoàng Vũ HuyNessuna valutazione finora

- CostConExercise - COGM & COGSDocumento3 pagineCostConExercise - COGM & COGSLee Tarroza100% (1)

- Chapter 03Documento12 pagineChapter 03Asim NazirNessuna valutazione finora

- Incomplete RecordsDocumento9 pagineIncomplete RecordsOkasha AliNessuna valutazione finora

- Question 2: Ias 19 Employee Benefits: Page 1 of 2Documento2 pagineQuestion 2: Ias 19 Employee Benefits: Page 1 of 2paul sagudaNessuna valutazione finora

- Study Guide For Students in Cost AccountingDocumento41 pagineStudy Guide For Students in Cost Accountingjanine moldinNessuna valutazione finora

- Master Budget Assignment CH 9Documento4 pagineMaster Budget Assignment CH 9api-240741436Nessuna valutazione finora

- Chapter-Six Accounting For General, Special Revenue and Capital Project FundsDocumento31 pagineChapter-Six Accounting For General, Special Revenue and Capital Project FundsMany Girma100% (1)

- Accounting PracticeDocumento14 pagineAccounting PracticeHamza RaufNessuna valutazione finora

- Chapter 1-Introduction To Financial Reporting: Multiple ChoiceDocumento17 pagineChapter 1-Introduction To Financial Reporting: Multiple Choicekurinkato83100% (1)

- Accounting Problems On Joint Venture AccountsDocumento6 pagineAccounting Problems On Joint Venture Accountskulvirchanna06Nessuna valutazione finora

- Chapter 1 - Introduction To Financial AccountingDocumento9 pagineChapter 1 - Introduction To Financial AccountingJon garcia100% (1)

- POA1-Assignment - Chapter 5 - QDocumento5 paginePOA1-Assignment - Chapter 5 - QAuora Bianca100% (1)

- Rais12 SM ch13Documento32 pagineRais12 SM ch13Edwin MayNessuna valutazione finora

- Accounting SolutionsDocumento11 pagineAccounting SolutionsKrittima Parn SuwanphorungNessuna valutazione finora

- Hillyard Master BudgetDocumento4 pagineHillyard Master Budgetyuikokhj75% (4)

- CH 09Documento94 pagineCH 09Sahar YehiaNessuna valutazione finora

- CH 4 - End of Chapter Exercises SolutionsDocumento80 pagineCH 4 - End of Chapter Exercises SolutionsPatrick AlphonseNessuna valutazione finora

- Formal Letters - CV PDFDocumento4 pagineFormal Letters - CV PDFIrina DavidNessuna valutazione finora

- Budget Practice QuestionsDocumento8 pagineBudget Practice Questionsmohammad bilalNessuna valutazione finora

- PartnershipsDocumento27 paginePartnershipssamuel debebeNessuna valutazione finora

- Audit Case14 33 CompleteDocumento9 pagineAudit Case14 33 CompleteIhsan NurhilmiNessuna valutazione finora

- Assignment 3 Managerial Accounting: Submitted By-Ghayoor Zafar Submitted To - DR MohsinDocumento11 pagineAssignment 3 Managerial Accounting: Submitted By-Ghayoor Zafar Submitted To - DR Mohsinjgfjhf arwtr100% (1)

- 7 Cs of Communication QuizDocumento4 pagine7 Cs of Communication QuizLUCINO JR VALMORESNessuna valutazione finora

- ACN 201 - Course Outline, Summer 2017Documento6 pagineACN 201 - Course Outline, Summer 2017saha sudipNessuna valutazione finora

- Chapter 2 - MCQ - Basic Cost Management ConceptsDocumento8 pagineChapter 2 - MCQ - Basic Cost Management Conceptslalith4uNessuna valutazione finora

- A211 Syllabus BKAR1013-StudentDocumento7 pagineA211 Syllabus BKAR1013-StudentVinoshini DeviNessuna valutazione finora

- Business BudgetingDocumento77 pagineBusiness BudgetingDewanFoysalHaqueNessuna valutazione finora

- Chapter 4 Inventorie Ifa 4Documento38 pagineChapter 4 Inventorie Ifa 4Nigussie BerhanuNessuna valutazione finora

- Asset Recognition and Operating Assets: Fourth EditionDocumento55 pagineAsset Recognition and Operating Assets: Fourth EditionAyush JainNessuna valutazione finora

- MG Chap 26 6, 8, and 10 - Feb 7, 2020Documento10 pagineMG Chap 26 6, 8, and 10 - Feb 7, 2020Mg Garcia100% (1)

- Managerial Accounting ExamDocumento10 pagineManagerial Accounting ExamJeremy Linn100% (1)

- Ch06 InventoryDocumento73 pagineCh06 Inventoryhiroshi aditNessuna valutazione finora

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocumento27 pagineIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeccNessuna valutazione finora

- Ch6 Inventories BBDocumento40 pagineCh6 Inventories BBmkrmashaqNessuna valutazione finora

- Working CapitalDocumento55 pagineWorking CapitalAlli Praveen KumarNessuna valutazione finora

- ACC 410 Critical AssignmentDocumento34 pagineACC 410 Critical AssignmentMichael LeibaNessuna valutazione finora

- Accounting AssignmentDocumento16 pagineAccounting AssignmentAarya SharmaNessuna valutazione finora

- Week 1 Nature & Scope of Financial ManagementDocumento49 pagineWeek 1 Nature & Scope of Financial Managementleong kahminNessuna valutazione finora

- What Is The Goodwill To Assets Ratio?Documento5 pagineWhat Is The Goodwill To Assets Ratio?YanxiZoe CruzNessuna valutazione finora

- P 16-3 PDFDocumento2 pagineP 16-3 PDFNatasha PNessuna valutazione finora

- Deutsche Finan ExcelDocumento6 pagineDeutsche Finan ExcelAnonymous VVSLkDOAC1Nessuna valutazione finora

- BADVAC2X Review (Partnership Formation-Dissolution) - P1Documento15 pagineBADVAC2X Review (Partnership Formation-Dissolution) - P1Reymark SadoyNessuna valutazione finora

- Inventories Notes2 170419181823Documento28 pagineInventories Notes2 170419181823Ebsa AdemeNessuna valutazione finora

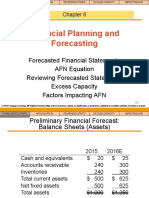

- Financial Planning and ForecastingDocumento15 pagineFinancial Planning and ForecastingNicolaus BagaskaraNessuna valutazione finora

- Vertical and HorizontalDocumento25 pagineVertical and HorizontalJunaid MalikNessuna valutazione finora

- Module 13Documento8 pagineModule 13Maria Therese CorderoNessuna valutazione finora

- Karen Moving Co. WorksheetDocumento9 pagineKaren Moving Co. WorksheetDanica OnteNessuna valutazione finora

- Mba Summer 2019Documento4 pagineMba Summer 2019Dhruvi PatelNessuna valutazione finora

- Review Materials 2 - Partnership Dissolution and Liquidation (Concised)Documento3 pagineReview Materials 2 - Partnership Dissolution and Liquidation (Concised)Jason RadamNessuna valutazione finora

- Balance Sheet As Per Schedule VI Indian Companies Act, 1956: Liabilities AssetsDocumento50 pagineBalance Sheet As Per Schedule VI Indian Companies Act, 1956: Liabilities AssetsSreekumar NarayanaNessuna valutazione finora

- Accounting I ModuleDocumento92 pagineAccounting I ModuleJay Githuku100% (1)

- (041621) Nike, Inc. - Cost of CapitalDocumento8 pagine(041621) Nike, Inc. - Cost of CapitalPutri Alya RamadhaniNessuna valutazione finora

- MS7SL800 - Assignment - 1 - McBrideDocumento36 pagineMS7SL800 - Assignment - 1 - McBrideDaniel AjanthanNessuna valutazione finora

- TIP: Transaction (A) Is Presented Below As An Example.: 1. Ejercicio E2-12 de La Página 85 yDocumento9 pagineTIP: Transaction (A) Is Presented Below As An Example.: 1. Ejercicio E2-12 de La Página 85 yEstefanía ZavalaNessuna valutazione finora

- Ch16 DepreciationMethodsDocumento48 pagineCh16 DepreciationMethodsJoelle KharratNessuna valutazione finora

- Audit of Property, Plant, and Equipment, Wasting Assets, and Intangible AssetsDocumento9 pagineAudit of Property, Plant, and Equipment, Wasting Assets, and Intangible AssetsyhygyugNessuna valutazione finora

- Pledge - : Far 6810 - Receivable FinancingDocumento3 paginePledge - : Far 6810 - Receivable FinancingKent Raysil PamaongNessuna valutazione finora

- 06 Financial Estimates and ProjectionsDocumento19 pagine06 Financial Estimates and ProjectionsSri RanjaniNessuna valutazione finora