Potrebbero piacerti anche

- Tax Compliance On PayrollDocumento2 pagineTax Compliance On PayrollJoyceNessuna valutazione finora

- Strategic Tax Management - Week 2Documento44 pagineStrategic Tax Management - Week 2Arman DalisayNessuna valutazione finora

- ACCOUNTING FOR CORPORATES (BBBH233) - 001 Module 1 - 1573561029351Documento66 pagineACCOUNTING FOR CORPORATES (BBBH233) - 001 Module 1 - 1573561029351Harshit Kumar GuptaNessuna valutazione finora

- Answer Guidance For c6Documento13 pagineAnswer Guidance For c6thicknhinmaykhoc100% (1)

- Regular Itemized DeductionDocumento24 pagineRegular Itemized DeductionPrince Anton DomondonNessuna valutazione finora

- Single Entry System or ADocumento12 pagineSingle Entry System or AsmilesamNessuna valutazione finora

- DTC ProvisionsDocumento3 pagineDTC ProvisionsrajdeeppawarNessuna valutazione finora

- Basic BookkeepingDocumento80 pagineBasic BookkeepingCharity CotejoNessuna valutazione finora

- (D) Capital of The Surviving SpouseDocumento3 pagine(D) Capital of The Surviving SpouseAnthony Angel TejaresNessuna valutazione finora

- Save Monies, Save Time and ADD VALUE To Your Business!Documento5 pagineSave Monies, Save Time and ADD VALUE To Your Business!Yasser AureadaNessuna valutazione finora

- Sales Tax GuideDocumento6 pagineSales Tax GuideakhileshkantNessuna valutazione finora

- PPTXDocumento140 paginePPTXGuinevereNessuna valutazione finora

- Ias 12Documento33 pagineIas 12samrawithagos2002Nessuna valutazione finora

- Registration Procedure Under Central Sales Act (SectionDocumento23 pagineRegistration Procedure Under Central Sales Act (SectionkgudiyaNessuna valutazione finora

- Optional Standard Deductions ExampleDocumento7 pagineOptional Standard Deductions ExampleSandia EspejoNessuna valutazione finora

- Peachtree Exercise Part 2Documento10 paginePeachtree Exercise Part 2Juan KermaNessuna valutazione finora

- Tax Practice Set ReviewerDocumento9 pagineTax Practice Set Reviewerjjay_santosNessuna valutazione finora

- Internal Control WeaknessesDocumento3 pagineInternal Control WeaknessesRosaly JadraqueNessuna valutazione finora

- Accounting 3 NotesDocumento7 pagineAccounting 3 NotesJudyNessuna valutazione finora

- Chart of Accounts: Account NumberingDocumento15 pagineChart of Accounts: Account NumberingrjrjrjNessuna valutazione finora

- Problem Set 3 Financial Statements BS SE S18Documento8 pagineProblem Set 3 Financial Statements BS SE S18Nust Razi100% (1)

- Module For Managerial Accounting-Job Order CostingDocumento17 pagineModule For Managerial Accounting-Job Order CostingMary De JesusNessuna valutazione finora

- Draft RR Registration EOPT - For Public ConsultationDocumento18 pagineDraft RR Registration EOPT - For Public ConsultationGennelyn OdulioNessuna valutazione finora

- Inventory List SubmissionDocumento2 pagineInventory List SubmissionLevi Lazareno EugenioNessuna valutazione finora

- Chapter 22Documento19 pagineChapter 22Betelehem GebremedhinNessuna valutazione finora

- Job Order CostingDocumento1 paginaJob Order CostingVincent Pham100% (1)

- Notes To Financial StatementsDocumento9 pagineNotes To Financial StatementsCheryl FuentesNessuna valutazione finora

- Independent Auditor'S Report Abc CompanyDocumento4 pagineIndependent Auditor'S Report Abc CompanyLorena TudorascuNessuna valutazione finora

- Deductions From Gross IncomeDocumento2 pagineDeductions From Gross Incomericamae saladagaNessuna valutazione finora

- Chapter One Accounting Principles and Professional PracticeDocumento22 pagineChapter One Accounting Principles and Professional PracticeHussen Abdulkadir100% (1)

- Accounting For CashDocumento10 pagineAccounting For CashjoannaberroNessuna valutazione finora

- CHAPTER 4 Partiner ShipDocumento22 pagineCHAPTER 4 Partiner ShipTolesa Mogos100% (1)

- Answers R41920 Acctg Varsity Basic Acctg Level 2Documento12 pagineAnswers R41920 Acctg Varsity Basic Acctg Level 2John AceNessuna valutazione finora

- Tax Bulletin by SGV As of Oct 2014Documento18 pagineTax Bulletin by SGV As of Oct 2014adobopinikpikanNessuna valutazione finora

- ADV I Chapter 3 2009Documento17 pagineADV I Chapter 3 2009temedebere100% (1)

- Legal Writng Atty. Alejandria Sept. 14,2016Documento4 pagineLegal Writng Atty. Alejandria Sept. 14,2016Anonymous IJah4mNessuna valutazione finora

- Electronic Filing and Payment System (EFPS)Documento12 pagineElectronic Filing and Payment System (EFPS)Karissa GaviolaNessuna valutazione finora

- Accountancy Chapter 1Documento9 pagineAccountancy Chapter 1Yhale DomiguezNessuna valutazione finora

- Practical Accounting Problems 1Documento4 paginePractical Accounting Problems 1Eleazer Ego-oganNessuna valutazione finora

- Companies Law: Presented by Deepshikha Meeta Nikita ShivaniDocumento63 pagineCompanies Law: Presented by Deepshikha Meeta Nikita ShivaniSahil SherasiyaNessuna valutazione finora

- Accounting Test Prep 1Documento9 pagineAccounting Test Prep 1Swathi ShekarNessuna valutazione finora

- Recording of Business TransactionsDocumento30 pagineRecording of Business TransactionsAnthony John BrionesNessuna valutazione finora

- Auditing QuestionsDocumento10 pagineAuditing Questionssalva8983Nessuna valutazione finora

- Sample On Professional Letter To ClientDocumento4 pagineSample On Professional Letter To ClientcapslocktabNessuna valutazione finora

- Accounting Information Systems, 10th Edition: James A. HallDocumento35 pagineAccounting Information Systems, 10th Edition: James A. HallAlexis Kaye DayagNessuna valutazione finora

- Strategic Cost Management Jpfranco: Lecture Note in Responsibility AccountingDocumento10 pagineStrategic Cost Management Jpfranco: Lecture Note in Responsibility AccountingAnnamarisse parungaoNessuna valutazione finora

- Practice Test - Financial ManagementDocumento6 paginePractice Test - Financial Managementelongoria278100% (1)

- Alpha ListDocumento22 pagineAlpha ListArnold BaladjayNessuna valutazione finora

- Are Electronic Medical Records A Cure For Health Care?Documento4 pagineAre Electronic Medical Records A Cure For Health Care?Sanjay PudasainiNessuna valutazione finora

- Accruals and DeferralsDocumento2 pagineAccruals and DeferralsravisankarNessuna valutazione finora

- Advanced Tax Laws CS Professional, YES AcademyDocumento33 pagineAdvanced Tax Laws CS Professional, YES AcademyKaran AroraNessuna valutazione finora

- Chapter-5-Drafting Fundamental Documents PDFDocumento4 pagineChapter-5-Drafting Fundamental Documents PDFShubham AgarwalNessuna valutazione finora

- Final Exam Advance Accounting WADocumento5 pagineFinal Exam Advance Accounting WAShawn OrganoNessuna valutazione finora

- Chapter 9 Percentage TaxDocumento25 pagineChapter 9 Percentage TaxTrisha Mae BoholNessuna valutazione finora

- CS Form Oath of OfficeDocumento1 paginaCS Form Oath of OfficeJan PriorNessuna valutazione finora

- PHC-BOA UpdatesDocumento67 paginePHC-BOA UpdatesMaynard Mirano100% (1)

- BIR RR 13 - 18 MatrixDocumento2 pagineBIR RR 13 - 18 MatrixErmawooNessuna valutazione finora

- Government Accounting DiscussionDocumento8 pagineGovernment Accounting DiscussionSamantha Alice LysanderNessuna valutazione finora

- p2 - Guerrero Ch11Documento24 paginep2 - Guerrero Ch11JerichoPedragosa100% (2)

- MBBcurrent 562526534235 2022-06-30 PDFDocumento6 pagineMBBcurrent 562526534235 2022-06-30 PDFmuhamad faidzalNessuna valutazione finora

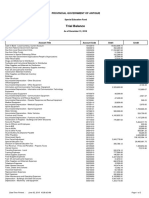

- Special Education Fund - Trial BalanceDocumento2 pagineSpecial Education Fund - Trial BalanceAccounting AntiqueNessuna valutazione finora

- Investment Banking Firms (Handouts)Documento2 pagineInvestment Banking Firms (Handouts)Joyce Ann SosaNessuna valutazione finora

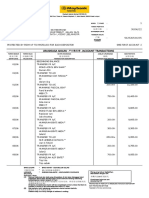

- Account Statement From 1 Nov 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento3 pagineAccount Statement From 1 Nov 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceMukesh SharmaNessuna valutazione finora

- Activity1.3.the Contemporary World ClassDocumento6 pagineActivity1.3.the Contemporary World ClassJhon dave Surbano100% (6)

- Plastic MoneyDocumento9 paginePlastic Moneyraj sharmaNessuna valutazione finora

- Profit Sharing PDFDocumento19 pagineProfit Sharing PDFGadisNessuna valutazione finora

- Sbi Fix Deposit SlipDocumento1 paginaSbi Fix Deposit SlipRahul Kumar82% (11)

- CH 7 SourcesDocumento6 pagineCH 7 Sourcesmanoj kashyapNessuna valutazione finora

- Euro Currency Deposits: Aakash Bafna (Tybms A) 9100108Documento3 pagineEuro Currency Deposits: Aakash Bafna (Tybms A) 9100108Akash BafnaNessuna valutazione finora

- EquityDocumento126 pagineEquityChristopherNessuna valutazione finora

- Loan PolicyDocumento5 pagineLoan PolicyAyesha FarooqNessuna valutazione finora

- Ifcb2009 16Documento291 pagineIfcb2009 16Shakti SinghNessuna valutazione finora

- Bdo Cir Form PDFDocumento2 pagineBdo Cir Form PDFLeslie Ann Cabasi TenioNessuna valutazione finora

- Factors Affecting Commercial Banks Profitability in PakistanDocumento12 pagineFactors Affecting Commercial Banks Profitability in PakistanArif ullahNessuna valutazione finora

- Zoho - GoAir Ticket PDFDocumento2 pagineZoho - GoAir Ticket PDFJaikumar Janarthanan0% (1)

- Debt Funding in India, Nishith Desai Associates, Available At, Last Visited On 8 April, 2019 External Commercial Borrowings & Trade Credits, Available at Last Visited On 9 April 2019Documento3 pagineDebt Funding in India, Nishith Desai Associates, Available At, Last Visited On 8 April, 2019 External Commercial Borrowings & Trade Credits, Available at Last Visited On 9 April 2019Kunwar AbhudayNessuna valutazione finora

- PPT Presentation RbiDocumento10 paginePPT Presentation RbiAayushNessuna valutazione finora

- Conclusion It or EbankDocumento1 paginaConclusion It or EbankchandamatlaniNessuna valutazione finora

- Opening Saving Account in HDFC BankDocumento31 pagineOpening Saving Account in HDFC BankSukhchain AggarwalNessuna valutazione finora

- Luca PacioliDocumento14 pagineLuca PaciolialexileaNessuna valutazione finora

- BA303 - Tutorial 10Documento2 pagineBA303 - Tutorial 10Vin ShyangNessuna valutazione finora

- Edward Burns - 5444Documento5 pagineEdward Burns - 5444Mark WilliamsNessuna valutazione finora

- Hayek Vs Keynes - A ComparisonDocumento4 pagineHayek Vs Keynes - A ComparisonIttisha SarahNessuna valutazione finora

- MetLife Endowment Savings Plan PRINT Brochure - 2016 V2 - tcm47-27873Documento4 pagineMetLife Endowment Savings Plan PRINT Brochure - 2016 V2 - tcm47-27873himanshu goyalNessuna valutazione finora

- Cityam 2011-09-19Documento36 pagineCityam 2011-09-19City A.M.Nessuna valutazione finora

- MITC CCDocumento15 pagineMITC CCArman MominNessuna valutazione finora

- PNB Vs CirDocumento8 paginePNB Vs CirAnonymous VtsflLix1Nessuna valutazione finora

- Latest BillDocumento3 pagineLatest Billrostyn160% (5)

- Corrigendum Gramin Bank MPDocumento60 pagineCorrigendum Gramin Bank MPsaurabhbectorNessuna valutazione finora