Potrebbero piacerti anche

- Mercantile Law ReviewerDocumento226 pagineMercantile Law ReviewerMelody BangsaludNessuna valutazione finora

- 32-Marubeni Corp. v. CIR G.R. No. 76573 March 7, 1990Documento2 pagine32-Marubeni Corp. v. CIR G.R. No. 76573 March 7, 1990Jopan SJNessuna valutazione finora

- CIR vs. CE Luzon 190198Documento1 paginaCIR vs. CE Luzon 190198magenNessuna valutazione finora

- National Power Corporation v. City of Cabanatuan, G.R. No. 149110, April 09, 2003Documento19 pagineNational Power Corporation v. City of Cabanatuan, G.R. No. 149110, April 09, 2003Glargo GlargoNessuna valutazione finora

- Tax Review Notes 2018 19 Part 6 PDFDocumento24 pagineTax Review Notes 2018 19 Part 6 PDFKeziah HuelarNessuna valutazione finora

- Supreme Transliner Vs BpiDocumento10 pagineSupreme Transliner Vs BpiEricson Sarmiento Dela CruzNessuna valutazione finora

- Gosiaco v. Ching and Casta, GR 173807, April 16, 2009 FactsDocumento2 pagineGosiaco v. Ching and Casta, GR 173807, April 16, 2009 FactsRoselle LagamayoNessuna valutazione finora

- Cir Vs CA, Cta, GCL Retirement PlanDocumento6 pagineCir Vs CA, Cta, GCL Retirement PlanLord AumarNessuna valutazione finora

- Competition LawDocumento14 pagineCompetition LawVikas AhujaNessuna valutazione finora

- CASES - DigestDocumento11 pagineCASES - DigestChameNessuna valutazione finora

- MC 02-1-93 or 14-9-92Documento3 pagineMC 02-1-93 or 14-9-92Jet BesacruzNessuna valutazione finora

- Special Issues On International LawDocumento2 pagineSpecial Issues On International LawRobert RamirezNessuna valutazione finora

- Vat Refunds (Compilation)Documento42 pagineVat Refunds (Compilation)Jesús LapuzNessuna valutazione finora

- 1-Republic Vs CA 200 SCRA 226Documento9 pagine1-Republic Vs CA 200 SCRA 226enan_intonNessuna valutazione finora

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocumento6 pagineBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledJoyce LapuzNessuna valutazione finora

- CIR vs. LiquigazDocumento2 pagineCIR vs. LiquigazRodney SantiagoNessuna valutazione finora

- PIL ReviewerDocumento2 paginePIL ReviewerMA D SantosNessuna valutazione finora

- BIR - DONOR'S TaxDocumento5 pagineBIR - DONOR'S TaxKim EspinaNessuna valutazione finora

- 35 Metro Pacific Corp Vs CIR (CTA Case)Documento3 pagine35 Metro Pacific Corp Vs CIR (CTA Case)Yaneeza MacapadoNessuna valutazione finora

- Supreme Court of Canada C: Canada V. Glaxosmithkline Inc., 2012 SCC 52, (2012) 3 D: 20121018 D: 33874 B: Her Majesty The QueenDocumento39 pagineSupreme Court of Canada C: Canada V. Glaxosmithkline Inc., 2012 SCC 52, (2012) 3 D: 20121018 D: 33874 B: Her Majesty The QueenJm CruzNessuna valutazione finora

- Sample LawRev Case DigestDocumento2 pagineSample LawRev Case DigestZacky AzarragaNessuna valutazione finora

- J. Bersamin TaxDocumento14 pagineJ. Bersamin TaxJessica JungNessuna valutazione finora

- Explanatory Notes NIRC 1-30 Part 1 Aug2018Documento23 pagineExplanatory Notes NIRC 1-30 Part 1 Aug2018Anonymous MikI28PkJcNessuna valutazione finora

- Rem-Finals Cajayon r1Documento12 pagineRem-Finals Cajayon r1BaseDwellerNessuna valutazione finora

- 67 CIR V Procter GambleDocumento2 pagine67 CIR V Procter GambleNaomi QuimpoNessuna valutazione finora

- CPAR B94 TAX Final PB Exam - QuestionsDocumento14 pagineCPAR B94 TAX Final PB Exam - QuestionsSilver LilyNessuna valutazione finora

- CIR v. PALDocumento18 pagineCIR v. PALmceline19Nessuna valutazione finora

- Soriano Vs SOFDocumento5 pagineSoriano Vs SOFChelle BelenzoNessuna valutazione finora

- 1-CIR Vs General Foods, Inc. - GR NO. 143672Documento1 pagina1-CIR Vs General Foods, Inc. - GR NO. 143672Jason BUENANessuna valutazione finora

- Chapter Vii TaxationDocumento15 pagineChapter Vii Taxationkimberly milagNessuna valutazione finora

- SRC Cases DigestedDocumento5 pagineSRC Cases DigestedTalina BinondoNessuna valutazione finora

- Team Pacific Vs DazaDocumento2 pagineTeam Pacific Vs Dazaroquesa burayNessuna valutazione finora

- Non-REVENUE OBJECTIVES OF TAXATIONDocumento1 paginaNon-REVENUE OBJECTIVES OF TAXATIONPrecious Grace Enrera ValenciaNessuna valutazione finora

- Tax CasesDocumento65 pagineTax CasesMaria BethNessuna valutazione finora

- WMPC V CIR - SPITDocumento1 paginaWMPC V CIR - SPITliapobsNessuna valutazione finora

- Rulings2000 DigestDocumento21 pagineRulings2000 DigestArriane MartinezNessuna valutazione finora

- Cases 3Documento28 pagineCases 3Joy VillasisNessuna valutazione finora

- Digest TaxDocumento3 pagineDigest TaxAimee MilleteNessuna valutazione finora

- What Is Toyota Financial ServicesDocumento3 pagineWhat Is Toyota Financial ServicesSaurabh TyagiNessuna valutazione finora

- Marcial Vs Hi-CementDocumento12 pagineMarcial Vs Hi-Cementkat perezNessuna valutazione finora

- Estate Tax: 86, NIRC)Documento15 pagineEstate Tax: 86, NIRC)Cesyl Patricia BallesterosNessuna valutazione finora

- Real Property Taxation Sec. of Finance V. Ilarde G.R. No. 121782. May 9, 2005 Chico-Nazario, J.Documento19 pagineReal Property Taxation Sec. of Finance V. Ilarde G.R. No. 121782. May 9, 2005 Chico-Nazario, J.dyosaNessuna valutazione finora

- Spouses Genato v. ViolaDocumento8 pagineSpouses Genato v. ViolaPam RamosNessuna valutazione finora

- Samar-I Electric Cooperative. v. CommissionerDocumento12 pagineSamar-I Electric Cooperative. v. CommissionerRheneir Mora100% (1)

- Transfer Taxes: SEC. 84 Rates of Estate Tax. - There Shall Be Levied, AssessedDocumento16 pagineTransfer Taxes: SEC. 84 Rates of Estate Tax. - There Shall Be Levied, AssessedAster Beane AranetaNessuna valutazione finora

- Ursal vs. CADocumento1 paginaUrsal vs. CAPreciousNessuna valutazione finora

- Republic Act No 9337Documento31 pagineRepublic Act No 9337Mie TotNessuna valutazione finora

- Lung Center of The PH v. QCDocumento3 pagineLung Center of The PH v. QCJB GuevarraNessuna valutazione finora

- Western Minolco Corporation Vs CIRDocumento1 paginaWestern Minolco Corporation Vs CIRRafael JuicoNessuna valutazione finora

- G.R. No. 190506 Coral Bay Nickel Corporation, Petitioner, Commissioner of Internal Revenue, Respondent. Decision Bersamin, J.Documento3 pagineG.R. No. 190506 Coral Bay Nickel Corporation, Petitioner, Commissioner of Internal Revenue, Respondent. Decision Bersamin, J.carlo_tabangcuraNessuna valutazione finora

- Republic vs. Bolante, G.R. No. 186717, April 17, 2017Documento7 pagineRepublic vs. Bolante, G.R. No. 186717, April 17, 2017Rodolfo Villamer Tobias Jr.Nessuna valutazione finora

- Remedial Law Case DigestsDocumento37 pagineRemedial Law Case DigestsDonna PhoebeNessuna valutazione finora

- Abs-Cbn v. Cta and NPC v. CbaaDocumento2 pagineAbs-Cbn v. Cta and NPC v. CbaaRyan BagagnanNessuna valutazione finora

- Ra 10607Documento27 pagineRa 10607Deneb DoydoraNessuna valutazione finora

- The Corporation Code of The PhilippinesDocumento5 pagineThe Corporation Code of The PhilippinesIbiang DeleozNessuna valutazione finora

- 8.cir V Roh Auto ProductsDocumento2 pagine8.cir V Roh Auto ProductsQuengilyn QuintosNessuna valutazione finora

- Eneral Rinciples OF Axation F P T: TaxationDocumento7 pagineEneral Rinciples OF Axation F P T: TaxationMarconie Nacar100% (1)

- Value-Added Tax: Characteristics (Abcd Vip)Documento9 pagineValue-Added Tax: Characteristics (Abcd Vip)janjan eresoNessuna valutazione finora

- VAT Exempt SalesDocumento14 pagineVAT Exempt SalesJuvanni SantosNessuna valutazione finora

- PT, Excise and DST NotesDocumento10 paginePT, Excise and DST NotesFayie De LunaNessuna valutazione finora

- Philippine ConstitutionDocumento14 paginePhilippine ConstitutionSamantha TayoneNessuna valutazione finora

- Section 1139Documento10 pagineSection 1139Samantha TayoneNessuna valutazione finora

- VAT Zero-Rated TransactionDocumento41 pagineVAT Zero-Rated TransactionSamantha TayoneNessuna valutazione finora

- Regular Output Vat 1Documento39 pagineRegular Output Vat 1Samantha Tayone100% (1)

- Written ReportDocumento10 pagineWritten ReportSamantha TayoneNessuna valutazione finora

- RenewalDocumento6 pagineRenewalSamantha TayoneNessuna valutazione finora

- 2.6 Commissioner V PhilAmLifeDocumento5 pagine2.6 Commissioner V PhilAmLifeJayNessuna valutazione finora

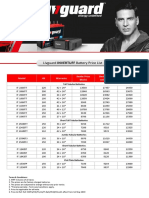

- Livguard IB Dealers Pricelist May 2019Documento1 paginaLivguard IB Dealers Pricelist May 2019chirag tandonNessuna valutazione finora

- Business Finance: Management of Working Capital AccountsDocumento17 pagineBusiness Finance: Management of Working Capital AccountsNicole Ann RamosNessuna valutazione finora

- Tax Consequences: No Output Tax Allowed and Seller IsDocumento12 pagineTax Consequences: No Output Tax Allowed and Seller IsXerez SingsonNessuna valutazione finora

- Income From Other SourcesDocumento29 pagineIncome From Other SourcesSatish BhadaniNessuna valutazione finora

- Bir RequirmentsDocumento4 pagineBir RequirmentsMa Therese MontessoriNessuna valutazione finora

- Tax 01 Prefinals Sept 9 2018 BSA4 Answer KeyDocumento11 pagineTax 01 Prefinals Sept 9 2018 BSA4 Answer KeyJohn Carlo Dela CruzNessuna valutazione finora

- ST SupO 3069 2022 23 193255Documento1 paginaST SupO 3069 2022 23 193255Rajat SharmaNessuna valutazione finora

- W2 & Earnings: Vanessa Sapien GonzalezDocumento4 pagineW2 & Earnings: Vanessa Sapien GonzalezVANESSA SAPIEN GONZALEZNessuna valutazione finora

- Wallace Hills Land Designation Referendum PresentationDocumento24 pagineWallace Hills Land Designation Referendum PresentationSipekne'katikNessuna valutazione finora

- BIR Form No. 1801 (Estate Tax Return)Documento2 pagineBIR Form No. 1801 (Estate Tax Return)Juan Miguel UngsodNessuna valutazione finora

- Mepco Online BillDocumento1 paginaMepco Online BillMahr MazharNessuna valutazione finora

- Penang Realty Case Against IRBDocumento15 paginePenang Realty Case Against IRBsimson singawahNessuna valutazione finora

- PEP Assignment 2Documento3 paginePEP Assignment 2Wajeeha NadeemNessuna valutazione finora

- Mothersonsumi Infotech & Designs Limited: Monthly Leave StatusDocumento1 paginaMothersonsumi Infotech & Designs Limited: Monthly Leave StatusswabhiNessuna valutazione finora

- Tax Issues in Demarger & AmalgamationDocumento25 pagineTax Issues in Demarger & AmalgamationMohit MishuNessuna valutazione finora

- Bring Back BABs: A Proposal To Strengthen The Municipal Bond Market With Build America BondsDocumento30 pagineBring Back BABs: A Proposal To Strengthen The Municipal Bond Market With Build America BondsCenter for American ProgressNessuna valutazione finora

- Activity 1 Employee Benefits AKDocumento7 pagineActivity 1 Employee Benefits AKRalph Rivera SantosNessuna valutazione finora

- Acc 496 Chapter 6Documento2 pagineAcc 496 Chapter 6Abdul HassonNessuna valutazione finora

- #35500038 - Megha Engg - MLIP Project Cluster-V - Tax InvoiceDocumento4 pagine#35500038 - Megha Engg - MLIP Project Cluster-V - Tax InvoicerameshNessuna valutazione finora

- Blank 4506TDocumento2 pagineBlank 4506TRoger PeiNessuna valutazione finora

- Income TaxationDocumento4 pagineIncome TaxationCervus Augustiniana LexNessuna valutazione finora

- Income Tax 2nd PretestDocumento3 pagineIncome Tax 2nd PretestEllaMay Delazerna0% (1)

- AITPN6389G - Issue Letter - 1053923881 (1) - 23062023Documento2 pagineAITPN6389G - Issue Letter - 1053923881 (1) - 23062023Peddaiah KarthiNessuna valutazione finora

- Tax 1.1Documento13 pagineTax 1.1Mheryza De Castro PabustanNessuna valutazione finora

- Od 226140729696188000Documento1 paginaOd 226140729696188000abhinaygvsNessuna valutazione finora

- Spa Services: Revenue ParametersDocumento2 pagineSpa Services: Revenue ParametersJosel Millan UbaldoNessuna valutazione finora

- Form 16Documento9 pagineForm 16KOKILA VIJAYAKUMARNessuna valutazione finora

- Taxguru - In-Taxes and Constitutional LimitationsDocumento4 pagineTaxguru - In-Taxes and Constitutional LimitationsAbi CherubNessuna valutazione finora

- Cary Conger Debunks Adam Ledford's Sac City Street Improvement Project Explanation Letter in The January 8, 2013 Sac SunDocumento3 pagineCary Conger Debunks Adam Ledford's Sac City Street Improvement Project Explanation Letter in The January 8, 2013 Sac SunthesacnewsNessuna valutazione finora