Potrebbero piacerti anche

- Accountant Resume 10Documento2 pagineAccountant Resume 10kelvin mkweshaNessuna valutazione finora

- Intuit QuickBooks Enterprise Accountant Edition 18 License-CertificateDocumento1 paginaIntuit QuickBooks Enterprise Accountant Edition 18 License-Certificatekelvin mkweshaNessuna valutazione finora

- Accountant Resume 14Documento3 pagineAccountant Resume 14kelvin mkweshaNessuna valutazione finora

- Chemistry Paper 4 October 2004Documento11 pagineChemistry Paper 4 October 2004Dean DambazaNessuna valutazione finora

- 2167 Paper 1 Q&aDocumento131 pagine2167 Paper 1 Q&akelvin mkweshaNessuna valutazione finora

- BM 208 Capital Gains Tax NotesDocumento52 pagineBM 208 Capital Gains Tax Noteskelvin mkweshaNessuna valutazione finora

- 4003q2 Specimen PDFDocumento24 pagine4003q2 Specimen PDFgray100% (2)

- What Are The Economic Functions of Government?: Lesson DescriptionDocumento3 pagineWhat Are The Economic Functions of Government?: Lesson Descriptionkelvin mkweshaNessuna valutazione finora

- Astrology Signs Meanings and CharacteristicsDocumento50 pagineAstrology Signs Meanings and Characteristicskelvin mkweshaNessuna valutazione finora

- Edoc - Tips - Free Poultry Business Plan PDF Poultry Farming PoultryDocumento2 pagineEdoc - Tips - Free Poultry Business Plan PDF Poultry Farming PoultrysuelaNessuna valutazione finora

- Complete Poultry Farming Business Plan for 2,400 Layers FarmDocumento8 pagineComplete Poultry Farming Business Plan for 2,400 Layers FarmAlina zainabNessuna valutazione finora

- Transfer Pricing-Based Money Laundering in Barter Trade: Dexiang Mei, Xiaojun LiDocumento8 pagineTransfer Pricing-Based Money Laundering in Barter Trade: Dexiang Mei, Xiaojun Likelvin mkweshaNessuna valutazione finora

- Poultry Farming Business Plan ExampleDocumento27 paginePoultry Farming Business Plan Examplemetro hydra80% (5)

- Poultry Farming Business Plan ExampleDocumento27 paginePoultry Farming Business Plan Examplemetro hydra80% (5)

- Illicit Financial Flows and Measures To Counter Them An IntroductionDocumento4 pagineIllicit Financial Flows and Measures To Counter Them An Introductionkelvin mkweshaNessuna valutazione finora

- Cac4203 The Auditor & Liability Under The LawDocumento14 pagineCac4203 The Auditor & Liability Under The Lawkelvin mkweshaNessuna valutazione finora

- Edoc - Tips - Free Poultry Business Plan PDF Poultry Farming PoultryDocumento2 pagineEdoc - Tips - Free Poultry Business Plan PDF Poultry Farming PoultrysuelaNessuna valutazione finora

- Your Guide To Acca Session CbesDocumento26 pagineYour Guide To Acca Session CbesdeepakNessuna valutazione finora

- New Doc 2018-01-09Documento2 pagineNew Doc 2018-01-09kelvin mkweshaNessuna valutazione finora

- Your Guide To Acca Session CbesDocumento26 pagineYour Guide To Acca Session CbesdeepakNessuna valutazione finora

- Your Guide To Acca Session CbesDocumento26 pagineYour Guide To Acca Session CbesdeepakNessuna valutazione finora

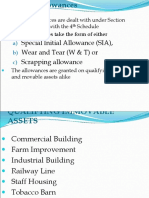

- 07 Capital Allowances-1Documento31 pagine07 Capital Allowances-1kelvin mkweshaNessuna valutazione finora

- Audit CasesDocumento4 pagineAudit Caseskelvin mkweshaNessuna valutazione finora

- Your Guide To Acca Session CbesDocumento26 pagineYour Guide To Acca Session CbesdeepakNessuna valutazione finora

- ADT V BDO Binder HamlynDocumento1 paginaADT V BDO Binder Hamlynkelvin mkweshaNessuna valutazione finora

- WorldcomDocumento1 paginaWorldcomkelvin mkweshaNessuna valutazione finora

- As Economics RevisionDocumento144 pagineAs Economics Revisionkelvin mkweshaNessuna valutazione finora

- Estate Duty Calculation for Late Mr Jones MpofuDocumento17 pagineEstate Duty Calculation for Late Mr Jones Mpofukelvin mkweshaNessuna valutazione finora

- Agenda Item 5-B: International Framework For Assurance EngagementsDocumento21 pagineAgenda Item 5-B: International Framework For Assurance Engagementskelvin mkweshaNessuna valutazione finora

- For PPEDocumento286 pagineFor PPEkelvin mkweshaNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Acctg3-7 Debt SecuritiesDocumento2 pagineAcctg3-7 Debt Securitiesflammy07Nessuna valutazione finora

- Bonds with Embedded Options ValuationDocumento52 pagineBonds with Embedded Options ValuationkalyanshreeNessuna valutazione finora

- International Capital Market Case Study - Part 1. Basic Knowledge of Capital MarketDocumento27 pagineInternational Capital Market Case Study - Part 1. Basic Knowledge of Capital Marketmanojbhatia1220Nessuna valutazione finora

- BTG Pactual - LocawebDocumento6 pagineBTG Pactual - LocawebV Borges EngenhariaNessuna valutazione finora

- Digvijay Construction 4may2021Documento7 pagineDigvijay Construction 4may2021hesham zakiNessuna valutazione finora

- Mutual Fund Investment Study In IndiaDocumento69 pagineMutual Fund Investment Study In IndiaSv KhanNessuna valutazione finora

- Secondary Market: Primary vs. Secondary MarketsDocumento2 pagineSecondary Market: Primary vs. Secondary Marketsdeepanshu1234Nessuna valutazione finora

- Chapter 4Documento6 pagineChapter 4Seemab KanwalNessuna valutazione finora

- ITM-IFM PlacementDocumento12 pagineITM-IFM PlacementpawanbajpaiNessuna valutazione finora

- Test Bank For Investments 9th Canadian by BodieDocumento32 pagineTest Bank For Investments 9th Canadian by BodieMonica Sanchez100% (31)

- Licensing HandbookDocumento75 pagineLicensing HandbookTan YLunNessuna valutazione finora

- Unit 4Documento3 pagineUnit 4Rossi Ana100% (1)

- Comparative Analysis of Three Asset Management CompaniesDocumento103 pagineComparative Analysis of Three Asset Management CompaniesAayushi PatelNessuna valutazione finora

- HDFC Prudence Fund PDFDocumento21 pagineHDFC Prudence Fund PDFaadhil1992Nessuna valutazione finora

- The Land Acquisition Act, 1894Documento9 pagineThe Land Acquisition Act, 1894Atif RehmanNessuna valutazione finora

- Financial Statement AssignmentDocumento16 pagineFinancial Statement Assignmentapi-275910271Nessuna valutazione finora

- A Final Project ReportDocumento82 pagineA Final Project ReportTarun BishtNessuna valutazione finora

- Column1 Column2 Column3 Column1 Column 2Documento3 pagineColumn1 Column2 Column3 Column1 Column 2Joele shNessuna valutazione finora

- STLT Finance 1 - Banking SystemDocumento10 pagineSTLT Finance 1 - Banking SystemHanae ElNessuna valutazione finora

- Concepts and Process of Book BuildingDocumento4 pagineConcepts and Process of Book BuildingGopalsamy SelvaduraiNessuna valutazione finora

- Investment CompanyDocumento16 pagineInvestment CompanyMd Abu Taher ChowdhuryNessuna valutazione finora

- DBB2104 Unit-09Documento24 pagineDBB2104 Unit-09anamikarajendran441998Nessuna valutazione finora

- Two Way CDADocumento4 pagineTwo Way CDAAnthony WalkerNessuna valutazione finora

- Testbank - Multinational Business Finance - Chapter 14Documento19 pagineTestbank - Multinational Business Finance - Chapter 14Uyen Nhi NguyenNessuna valutazione finora

- Financial Markets and Institutions GuideDocumento48 pagineFinancial Markets and Institutions GuideJun AdajarNessuna valutazione finora

- Comprehensive Annual Financial REPORT 2013: Puerto RicoDocumento142 pagineComprehensive Annual Financial REPORT 2013: Puerto RicoCarmen MenkarNessuna valutazione finora

- NedenumitDocumento17 pagineNedenumitAlice AnnaNessuna valutazione finora

- Taxation Two 2Documento23 pagineTaxation Two 2Truman TemperanteNessuna valutazione finora

- Request For Copy of Collateral Deposit Account POWERS CASEDocumento2 pagineRequest For Copy of Collateral Deposit Account POWERS CASETitle IV-D Man with a plan100% (1)

- Stock Market Project VaibhavDocumento71 pagineStock Market Project VaibhavVaibhav DhayeNessuna valutazione finora