Potrebbero piacerti anche

- How to Audit Your Account without Hiring an AuditorDa EverandHow to Audit Your Account without Hiring an AuditorNessuna valutazione finora

- Purpose of Internal ControlDocumento50 paginePurpose of Internal ControlTHATONessuna valutazione finora

- Audit 4Documento14 pagineAudit 4Nikhil KumarNessuna valutazione finora

- Internal Check and Internal ControlDocumento30 pagineInternal Check and Internal ControlMd. Saiful Islam BhuiyanNessuna valutazione finora

- Internal ControlDocumento39 pagineInternal Controlmiam67830Nessuna valutazione finora

- Internal-Control C3Documento22 pagineInternal-Control C3Sayraj Siddiki AnikNessuna valutazione finora

- Chapter Four Internal Control SystemDocumento28 pagineChapter Four Internal Control SystemMeseret AsefaNessuna valutazione finora

- Internal ControlDocumento30 pagineInternal ControlMarcel VelascoNessuna valutazione finora

- Systems Assessment Prepared by Omnia HassanDocumento25 pagineSystems Assessment Prepared by Omnia HassanOmnia HassanNessuna valutazione finora

- Auditing and Internal Control: Structure of An IT AuditDocumento6 pagineAuditing and Internal Control: Structure of An IT AuditMervidelleNessuna valutazione finora

- Module 2 - Internal Control-1Documento20 pagineModule 2 - Internal Control-1Melvin JustinNessuna valutazione finora

- Accounting Controls: What Are Internal Controls and Why Are They Important?Documento18 pagineAccounting Controls: What Are Internal Controls and Why Are They Important?sueernNessuna valutazione finora

- Internal ControlDocumento37 pagineInternal ControlMichelle Joy Nuyad-Pantinople100% (1)

- CHAPTER 4 Audit IDocumento24 pagineCHAPTER 4 Audit IDanisaraNessuna valutazione finora

- Unit II Company Audit and VouchingDocumento36 pagineUnit II Company Audit and VouchingMuskan TyagiNessuna valutazione finora

- Auditing One 04 For ClassDocumento22 pagineAuditing One 04 For ClassRObel demisNessuna valutazione finora

- Unit 2 Internal Check SystemDocumento24 pagineUnit 2 Internal Check SystemShaifaliChauhanNessuna valutazione finora

- Internal Control and ReviewDocumento22 pagineInternal Control and ReviewAnep ZainuldinNessuna valutazione finora

- Consideration of Internal ControlDocumento69 pagineConsideration of Internal Controlmah loveNessuna valutazione finora

- Chapter 2 Internal Control NotesDocumento46 pagineChapter 2 Internal Control Notesajaybc2104Nessuna valutazione finora

- Auditing Principles and PracticesDocumento31 pagineAuditing Principles and PracticesFackallofyouNessuna valutazione finora

- CHapter 5 Internal ControlDocumento11 pagineCHapter 5 Internal ControlYitera SisayNessuna valutazione finora

- Chapter 4 - Internal ControlDocumento107 pagineChapter 4 - Internal Controleskedar eyachewNessuna valutazione finora

- In The Name of Allah, The Most Beneficent, The Most MercifulDocumento40 pagineIn The Name of Allah, The Most Beneficent, The Most MercifulMuhammad SaadNessuna valutazione finora

- CH04 1Documento5 pagineCH04 1Tilahun TesemaNessuna valutazione finora

- Meaning of Internal Control (AUDIT 04)Documento13 pagineMeaning of Internal Control (AUDIT 04)Annam InayatNessuna valutazione finora

- TOPIC 3b - Internal ControlsDocumento15 pagineTOPIC 3b - Internal ControlsLANGITBIRUNessuna valutazione finora

- Control, Security and Audit: What Is Internal Control?Documento12 pagineControl, Security and Audit: What Is Internal Control?symhoutNessuna valutazione finora

- Auditing Lesson 4Documento11 pagineAuditing Lesson 4Ruth KanaizaNessuna valutazione finora

- Auditing and Internal Control: IT Auditing, J.Hall, 4eDocumento29 pagineAuditing and Internal Control: IT Auditing, J.Hall, 4eCherrie Arianne Fhaye NarajaNessuna valutazione finora

- Auditing and Internal Control: IT Auditing, J.Hall, 4eDocumento29 pagineAuditing and Internal Control: IT Auditing, J.Hall, 4eCherrie Arianne Fhaye NarajaNessuna valutazione finora

- Accounting Information Systems: Moscove, Simkin & BagranoffDocumento31 pagineAccounting Information Systems: Moscove, Simkin & BagranoffJessa WongNessuna valutazione finora

- Auditing Short NoteDocumento27 pagineAuditing Short Noteetebark h/michaleNessuna valutazione finora

- Objectives of Internal ControlDocumento2 pagineObjectives of Internal ControlAnurag GargNessuna valutazione finora

- Internal Control InventoryDocumento13 pagineInternal Control Inventoryabbyplexx100% (3)

- Auditing Part BDocumento26 pagineAuditing Part BVishwas AgarwalNessuna valutazione finora

- Internal Control and CashDocumento8 pagineInternal Control and CashHassleBustNessuna valutazione finora

- Audit Note TOPIC 4Documento47 pagineAudit Note TOPIC 4Tusiime Wa Kachope SamsonNessuna valutazione finora

- 500 Cash and Internal ControlDocumento28 pagine500 Cash and Internal ControlNirhd Jeff100% (1)

- Auditing Part BDocumento26 pagineAuditing Part BVishwas AgarwalNessuna valutazione finora

- COSO Implementation and The Role of Compliance Function: A Practical CaseDocumento39 pagineCOSO Implementation and The Role of Compliance Function: A Practical Casekhawarsher100% (1)

- Internal Control and Internal CheckDocumento18 pagineInternal Control and Internal CheckSuyash PatidarNessuna valutazione finora

- Z17520020220174021New PPT Ch1Documento30 pagineZ17520020220174021New PPT Ch1Melissa Indah FiantyNessuna valutazione finora

- Chapter 16 - Corporate GovernanceDocumento34 pagineChapter 16 - Corporate Governancekarryl barnuevoNessuna valutazione finora

- Internal Control: Aamer AllauddinDocumento36 pagineInternal Control: Aamer AllauddinNatalia NaveedNessuna valutazione finora

- Sistem Informasi Akuntansi Dan Tata KelolaDocumento23 pagineSistem Informasi Akuntansi Dan Tata KelolaRahmat KaswarNessuna valutazione finora

- .Study and Evaluation of Internal ControlDocumento35 pagine.Study and Evaluation of Internal Controlpamelajanmea2018Nessuna valutazione finora

- Auditing - Internal ControlDocumento3 pagineAuditing - Internal ControlPhassang TariuNessuna valutazione finora

- Chapter No.02: Internal ControlDocumento28 pagineChapter No.02: Internal ControlMasood khanNessuna valutazione finora

- Transaction Cycles and Internal ControlsDocumento16 pagineTransaction Cycles and Internal ControlsPreyNessuna valutazione finora

- Auditors Code of ConductDocumento33 pagineAuditors Code of ConductSherwin MosomosNessuna valutazione finora

- Ethics, Fraud, and Internal ControlDocumento10 pagineEthics, Fraud, and Internal ControlAstxilNessuna valutazione finora

- Internal Controls: Geetali TareDocumento50 pagineInternal Controls: Geetali TareKaren Anne AnteneoNessuna valutazione finora

- CAPE Accounting Unit 1 Module 1 Internal ControlsDocumento12 pagineCAPE Accounting Unit 1 Module 1 Internal ControlsRhea Lee RossNessuna valutazione finora

- Coso FrameworkDocumento47 pagineCoso FrameworkSrishti AgarwalNessuna valutazione finora

- At-14-Internal-Control ReviewerDocumento14 pagineAt-14-Internal-Control ReviewerHI HelloNessuna valutazione finora

- UNIT-2 Audit and Audit Procedure Audit EvidenceDocumento12 pagineUNIT-2 Audit and Audit Procedure Audit EvidenceLohith Kumar SNessuna valutazione finora

- Internal ControlDocumento6 pagineInternal ControlSumbul SammoNessuna valutazione finora

- Consideration of Internal ControlDocumento37 pagineConsideration of Internal ControlMaria Paz GanotNessuna valutazione finora

- Chapter 7Documento7 pagineChapter 7Bella KurebelNessuna valutazione finora

- Accounting, Unit 1 - Topic 1Documento68 pagineAccounting, Unit 1 - Topic 1Teal JacobsNessuna valutazione finora

- Accounting, Unit 1 - Topic 2 (Students)Documento64 pagineAccounting, Unit 1 - Topic 2 (Students)Teal Jacobs100% (1)

- Address: 4 East Avenue, Ocho Rios City: St. Ann Telephone: (876) 534-7869 Fax: (876) 544-6708Documento2 pagineAddress: 4 East Avenue, Ocho Rios City: St. Ann Telephone: (876) 534-7869 Fax: (876) 544-6708Teal JacobsNessuna valutazione finora

- National Health Fund Human Resource Department 25 Dominica Drive Kingston 5Documento2 pagineNational Health Fund Human Resource Department 25 Dominica Drive Kingston 5Teal JacobsNessuna valutazione finora

- Problem Solving Mark Scheme Grade 11Documento3 pagineProblem Solving Mark Scheme Grade 11Teal JacobsNessuna valutazione finora

- Announcing Our Sale: Product/Service InformationDocumento2 pagineAnnouncing Our Sale: Product/Service InformationTeal JacobsNessuna valutazione finora

- Credit MonitoringDocumento15 pagineCredit MonitoringTushar JoshiNessuna valutazione finora

- Afa 708 Midterm NotesDocumento8 pagineAfa 708 Midterm NotesMariam SiddiquiNessuna valutazione finora

- Ics 3210 Information Systems Security and AuditDocumento2 pagineIcs 3210 Information Systems Security and AuditWaguma LeticiaNessuna valutazione finora

- Sec Code of Corporate Governance AnswerDocumento3 pagineSec Code of Corporate Governance AnswerHechel DatinguinooNessuna valutazione finora

- Personal Data Sheet Vita VergaraDocumento6 paginePersonal Data Sheet Vita VergaraAljo FernandezNessuna valutazione finora

- Chapter 1 - Introduction To Information System AuditDocumento9 pagineChapter 1 - Introduction To Information System AuditMuriithi Murage100% (1)

- Appendix 2 - ISO/IEC 17025:2017 Internal Audit Checklist: Clause Requirement YES NO CommentsDocumento27 pagineAppendix 2 - ISO/IEC 17025:2017 Internal Audit Checklist: Clause Requirement YES NO CommentsahmedNessuna valutazione finora

- Audit ProceduresDocumento6 pagineAudit Procedureszxchua3100% (5)

- Checklist Pre-Tender Civil ProjectsDocumento8 pagineChecklist Pre-Tender Civil Projectssarathirv6Nessuna valutazione finora

- Internal AuditingDocumento68 pagineInternal AuditingLumin Han100% (2)

- Industry Forum IATF and VDA Training - Dec2016Documento12 pagineIndustry Forum IATF and VDA Training - Dec2016anthony dunnNessuna valutazione finora

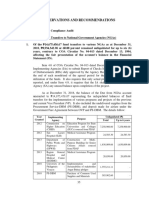

- COA's Observation and Recommendations (2018 Audit Report On OVP)Documento38 pagineCOA's Observation and Recommendations (2018 Audit Report On OVP)VERA FilesNessuna valutazione finora

- CIA Part 1, Unit 1-1Documento35 pagineCIA Part 1, Unit 1-1Ahmed AzaziNessuna valutazione finora

- BKAS3083 Topic1Documento27 pagineBKAS3083 Topic1WEIWEICHONG93Nessuna valutazione finora

- ISO 9001 Auditor Training Q&ADocumento10 pagineISO 9001 Auditor Training Q&AAli Zafar71% (7)

- Appendix 25 VDA 6 3 Process AuditDocumento12 pagineAppendix 25 VDA 6 3 Process AuditFirmino Simplicio0% (1)

- Accounting, Information Technology, and Business Solutions, 2nd EditionDocumento60 pagineAccounting, Information Technology, and Business Solutions, 2nd EditionDr.Mohamed Abd Allah MakhloufNessuna valutazione finora

- Integrated Case Application: Part II Required (A)Documento2 pagineIntegrated Case Application: Part II Required (A)T1sha100% (2)

- 6 Sa 250Documento2 pagine6 Sa 250Sai Naveen KumarNessuna valutazione finora

- Audit Working PapersDocumento49 pagineAudit Working Paperscgarcias7675% (4)

- Executive SummaryDocumento40 pagineExecutive SummaryEarl Louie M. MasacayanNessuna valutazione finora

- AA-Inherent RiskDocumento1 paginaAA-Inherent RiskRafsan JazzNessuna valutazione finora

- Internship ReportDocumento33 pagineInternship ReportPriyanka A SNessuna valutazione finora

- Paper10 SolutionDocumento19 paginePaper10 SolutionRkNessuna valutazione finora

- Audit On Accounts Receivable: Oni CosmeticsDocumento7 pagineAudit On Accounts Receivable: Oni Cosmeticsjoyce KimNessuna valutazione finora

- UntitledDocumento4 pagineUntitledteecee chidzvondoNessuna valutazione finora

- Functional FixationDocumento29 pagineFunctional Fixationyohanes adi nugrohoNessuna valutazione finora

- FINM024 AS1 Assessment BriefDocumento5 pagineFINM024 AS1 Assessment BriefSoumyadeep BoseNessuna valutazione finora

- Sustainability Report 2019: Going Green: We Take It Personally For SustainabilityDocumento78 pagineSustainability Report 2019: Going Green: We Take It Personally For SustainabilityVincent KohNessuna valutazione finora

- Chapter 9 - Audit Sampling - Substantive Tests of Account Balances - AnswersDocumento49 pagineChapter 9 - Audit Sampling - Substantive Tests of Account Balances - Answerssat726Nessuna valutazione finora