Potrebbero piacerti anche

- Reformulation - Analysis of SCFDocumento17 pagineReformulation - Analysis of SCFAkib Mahbub KhanNessuna valutazione finora

- One Job: Counterpoint Global InsightsDocumento25 pagineOne Job: Counterpoint Global Insightscartigayan100% (1)

- Yacktman PresentationDocumento34 pagineYacktman PresentationVijay MalikNessuna valutazione finora

- Fill and KillDocumento12 pagineFill and Killad9292Nessuna valutazione finora

- Guide To Capital AllocationDocumento5 pagineGuide To Capital AllocationUmbyisNessuna valutazione finora

- On Streaks: Perception, Probability, and SkillDocumento5 pagineOn Streaks: Perception, Probability, and Skilljohnwang_174817Nessuna valutazione finora

- Free Cash Flow Investing 04-18-11Documento6 pagineFree Cash Flow Investing 04-18-11lowbankNessuna valutazione finora

- Viewing Business Through The Lens of Financial StatementsDocumento55 pagineViewing Business Through The Lens of Financial StatementsAkib Mahbub KhanNessuna valutazione finora

- Penman FullDocumento64 paginePenman FullHenry So E DiarkoNessuna valutazione finora

- Arithmetic of EquitiesDocumento5 pagineArithmetic of Equitiesrwmortell3580Nessuna valutazione finora

- Buffett On ValuationDocumento7 pagineBuffett On ValuationAyush AggarwalNessuna valutazione finora

- Value For Money: Equity Valuation AcademyDocumento33 pagineValue For Money: Equity Valuation Academypritish jainNessuna valutazione finora

- Arlington Value 2006 Annual Shareholder LetterDocumento5 pagineArlington Value 2006 Annual Shareholder LetterSmitty WNessuna valutazione finora

- Bottom-Up EV Calculation (Finatics)Documento5 pagineBottom-Up EV Calculation (Finatics)Jessica KaryonoNessuna valutazione finora

- HOLT Notes - FadeDocumento3 pagineHOLT Notes - FadeElliott JimenezNessuna valutazione finora

- Dangers of DCF MortierDocumento12 pagineDangers of DCF MortierKitti WongtuntakornNessuna valutazione finora

- Primer On Stock ResearchDocumento37 paginePrimer On Stock ResearchgirishrajsNessuna valutazione finora

- Michael Mauboussin - Surge in The Urge To Merge, M&a Trends & Analysis 1-12-10Documento15 pagineMichael Mauboussin - Surge in The Urge To Merge, M&a Trends & Analysis 1-12-10Phaedrus34Nessuna valutazione finora

- Quality of Earnings Guide to Determining ProfitsDocumento2 pagineQuality of Earnings Guide to Determining ProfitsAshutosh GuptaNessuna valutazione finora

- BBVA OpenMind Libro El Proximo Paso Vida Exponencial2Documento59 pagineBBVA OpenMind Libro El Proximo Paso Vida Exponencial2giovanniNessuna valutazione finora

- CFROIDocumento15 pagineCFROImakrantjiNessuna valutazione finora

- Where's The Bar - Introducing Market-Expected Return On InvestmentDocumento17 pagineWhere's The Bar - Introducing Market-Expected Return On Investmentpjs15Nessuna valutazione finora

- Meausing A MoatDocumento73 pagineMeausing A MoatjesprileNessuna valutazione finora

- MS - Good Losses, Bad LossesDocumento13 pagineMS - Good Losses, Bad LossesResearch ReportsNessuna valutazione finora

- Redleaf Andy Absolute Return WhiteboxDocumento6 pagineRedleaf Andy Absolute Return WhiteboxMatt Taylor100% (1)

- Guggenheim ROIC PDFDocumento16 pagineGuggenheim ROIC PDFJames PattersonNessuna valutazione finora

- Economic Returns, Reversion To The Mean, and Total Shareholder Returns Anticipating Change Is Hard But ProfitableDocumento15 pagineEconomic Returns, Reversion To The Mean, and Total Shareholder Returns Anticipating Change Is Hard But ProfitableAhmed MadhaNessuna valutazione finora

- Strong Returns in 2014Documento8 pagineStrong Returns in 2014ChrisNessuna valutazione finora

- Morningstar Learning ResourcesDocumento1 paginaMorningstar Learning ResourcesLouisSigneNessuna valutazione finora

- Roe To CfroiDocumento30 pagineRoe To CfroiSyifa034Nessuna valutazione finora

- Complexity in Economic and Financial MarketsDocumento16 pagineComplexity in Economic and Financial Marketsdavebell30Nessuna valutazione finora

- Roc Roic Roe PDFDocumento69 pagineRoc Roic Roe PDFCharlie NealNessuna valutazione finora

- Corporate strategy and shareholder valueDocumento24 pagineCorporate strategy and shareholder valueprabhat127Nessuna valutazione finora

- FSAP ManualDocumento7 pagineFSAP ManualJose ArmazaNessuna valutazione finora

- How Active Share and Tracking Error Identify Skillful Portfolio ManagersDocumento13 pagineHow Active Share and Tracking Error Identify Skillful Portfolio ManagersPhaedrus34Nessuna valutazione finora

- Benjamin Graham and The Birth of Value InvestingDocumento85 pagineBenjamin Graham and The Birth of Value Investingrsepassi100% (1)

- A Piece of The Action - Employee Stock Options in The New EconomyDocumento45 pagineA Piece of The Action - Employee Stock Options in The New Economypjs15Nessuna valutazione finora

- Formulas #1: Future Value of A Single Cash FlowDocumento4 pagineFormulas #1: Future Value of A Single Cash FlowVikram Sathish AsokanNessuna valutazione finora

- Value Investor Insight Play Your GameDocumento4 pagineValue Investor Insight Play Your Gamevouzvouz7127100% (1)

- Bin There Done That - Us PDFDocumento19 pagineBin There Done That - Us PDFaaquibnasirNessuna valutazione finora

- Financial Fine Print: Uncovering a Company's True ValueDa EverandFinancial Fine Print: Uncovering a Company's True ValueValutazione: 3 su 5 stelle3/5 (3)

- Competitive Advantage PeriodDocumento6 pagineCompetitive Advantage PeriodAndrija BabićNessuna valutazione finora

- Capital AllocationDocumento75 pagineCapital Allocationak87840% (1)

- Still Powerful - The Internet's Hidden OrderDocumento17 pagineStill Powerful - The Internet's Hidden Orderpjs15Nessuna valutazione finora

- FINVEST Free Cash Flow Valuation SlidesDocumento5 pagineFINVEST Free Cash Flow Valuation SlidesOliverCheongNessuna valutazione finora

- Mauboussin Life of GameDocumento10 pagineMauboussin Life of GameDaniel TingNessuna valutazione finora

- The Executive Guide to Boosting Cash Flow and Shareholder Value: The Profit Pool ApproachDa EverandThe Executive Guide to Boosting Cash Flow and Shareholder Value: The Profit Pool ApproachNessuna valutazione finora

- Graham & Doddsville Winter Issue 2018Documento33 pagineGraham & Doddsville Winter Issue 2018marketfolly.comNessuna valutazione finora

- Profit Guru Bill NygrenDocumento5 pagineProfit Guru Bill NygrenekramcalNessuna valutazione finora

- Article - Mercer Capital Guide Option Pricing ModelDocumento18 pagineArticle - Mercer Capital Guide Option Pricing ModelKshitij SharmaNessuna valutazione finora

- Be Your Own ActivistDocumento11 pagineBe Your Own ActivistSwagdogNessuna valutazione finora

- Corporate Valuation Using The Free Cash Flow Method Applied To Coca-ColaDocumento66 pagineCorporate Valuation Using The Free Cash Flow Method Applied To Coca-ColaRober Nunez100% (1)

- In Defense of Shareholder ValueDocumento11 pagineIn Defense of Shareholder ValueJaime Andres Laverde ZuletaNessuna valutazione finora

- DCF Model TemplateDocumento6 pagineDCF Model TemplateHamda AkbarNessuna valutazione finora

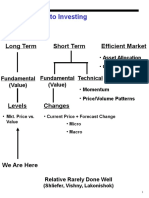

- Approaches To Investing: Long Term Short Term Efficient MarketDocumento71 pagineApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeNessuna valutazione finora

- Tech Stock Valuation: Investor Psychology and Economic AnalysisDa EverandTech Stock Valuation: Investor Psychology and Economic AnalysisValutazione: 4 su 5 stelle4/5 (1)

- Free Cash Flow and Shareholder Yield: New Priorities for the Global InvestorDa EverandFree Cash Flow and Shareholder Yield: New Priorities for the Global InvestorNessuna valutazione finora

- Summary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingDa EverandSummary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingNessuna valutazione finora

- Capital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisDa EverandCapital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisNessuna valutazione finora

- Corporate Share Capital ExplainedDocumento16 pagineCorporate Share Capital ExplainedPeter PiperNessuna valutazione finora

- Math in Finance MITDocumento22 pagineMath in Finance MITkkappaNessuna valutazione finora

- Design Process - BhavyaaDocumento47 pagineDesign Process - Bhavyaasahay designNessuna valutazione finora

- Day Trading Success Cheat Sheet DesireToTRADE PDFDocumento3 pagineDay Trading Success Cheat Sheet DesireToTRADE PDFRogério Oliveira100% (3)

- Finance Basics MCQs I Multiple Choice Questions I Business FinanceDocumento11 pagineFinance Basics MCQs I Multiple Choice Questions I Business FinanceTahir RehmanNessuna valutazione finora

- E-commerce-Assignment 01Documento4 pagineE-commerce-Assignment 01Abdul Rauf QureshiNessuna valutazione finora

- Contemporary World Course SyllabusDocumento6 pagineContemporary World Course SyllabusRose May LlosaNessuna valutazione finora

- Keywords: Rumors, Marketplace Rumors, Consumer Behavior, Word ofDocumento20 pagineKeywords: Rumors, Marketplace Rumors, Consumer Behavior, Word ofortega mukoNessuna valutazione finora

- Non Security Form of InvestmentDocumento16 pagineNon Security Form of InvestmentMonalisa BagdeNessuna valutazione finora

- MKT 646Documento7 pagineMKT 646sharifah ainnaNessuna valutazione finora

- Vk-Amfr-Pro-1 Vafax PDFDocumento63 pagineVk-Amfr-Pro-1 Vafax PDFElizabeth MontesNessuna valutazione finora

- The Impact of E-Business and Competitive AdvantageDocumento4 pagineThe Impact of E-Business and Competitive AdvantageInternational Journal of Innovative Science and Research TechnologyNessuna valutazione finora

- Chapter 4: The Costs of ProductionDocumento14 pagineChapter 4: The Costs of ProductionDiễn VânNessuna valutazione finora

- Caso Haiman El Troudi - Odebrecht - Cresswell OverseasDocumento14 pagineCaso Haiman El Troudi - Odebrecht - Cresswell OverseasCuentasClarasDigital.orgNessuna valutazione finora

- Q&A MarketingDocumento12 pagineQ&A MarketingrajeeevaNessuna valutazione finora

- Introduction to Operations ManagementDocumento5 pagineIntroduction to Operations Managementdra_gonNessuna valutazione finora

- How To Trade Flags (Continuation Patterns)Documento3 pagineHow To Trade Flags (Continuation Patterns)alpepezNessuna valutazione finora

- A Summer Internship Report ON Security Analysis and Portfolio Management AT "India Infoline Limited " (Iifl India)Documento34 pagineA Summer Internship Report ON Security Analysis and Portfolio Management AT "India Infoline Limited " (Iifl India)deepak tejaNessuna valutazione finora

- Unit 9 - Exchange Rate KeyDocumento7 pagineUnit 9 - Exchange Rate KeyBò SữaNessuna valutazione finora

- Factors Influencing Credit PolicyDocumento5 pagineFactors Influencing Credit PolicyMrDj Khan75% (4)

- Marketing in The Era of COVID 19: Janny C. Hoekstra Peter S. H. LeeflangDocumento12 pagineMarketing in The Era of COVID 19: Janny C. Hoekstra Peter S. H. LeeflangEnglish ClassNessuna valutazione finora

- Achieving Excellence in Retail Banking Marketing and Customer RelationshipsDocumento17 pagineAchieving Excellence in Retail Banking Marketing and Customer RelationshipsMohammad Ejaz AhmedNessuna valutazione finora

- DeMystifying DesignDocumento21 pagineDeMystifying DesignJolene FernandesNessuna valutazione finora

- AUD 323 Auditing & Assurance: Concepts & ApplicationsDocumento33 pagineAUD 323 Auditing & Assurance: Concepts & ApplicationsYvone Claire Fernandez SalmorinNessuna valutazione finora

- List of shareholders detailsDocumento1 paginaList of shareholders detailskaminiNessuna valutazione finora

- Developing Business Ideas Screening TechniquesDocumento28 pagineDeveloping Business Ideas Screening TechniquesTaisyNessuna valutazione finora

- BROKERDocumento2 pagineBROKERanotida marambaNessuna valutazione finora

- Low Income Welder's Business JourneyDocumento2 pagineLow Income Welder's Business JourneyAndy NarainNessuna valutazione finora

- Session 4 Urban Heritage and CommunityDocumento368 pagineSession 4 Urban Heritage and CommunityQuang Huy NguyễnNessuna valutazione finora

- Module No. 2 Lesson 1 ABM112Documento10 pagineModule No. 2 Lesson 1 ABM112Rush RushNessuna valutazione finora