Potrebbero piacerti anche

- Energy Crises in PakistanDocumento9 pagineEnergy Crises in PakistanHamza MunirNessuna valutazione finora

- Pep Bangladesch Pakistan Praes2Documento16 paginePep Bangladesch Pakistan Praes2scarletpimpernel009Nessuna valutazione finora

- Demand Projection and Generation Planning: Reasons For SlippageDocumento6 pagineDemand Projection and Generation Planning: Reasons For SlippageAnil SarangNessuna valutazione finora

- Presentation On State of Power Crisis in BangladeshDocumento10 paginePresentation On State of Power Crisis in BangladeshrifatNessuna valutazione finora

- IETO 2022 OutlookDocumento22 pagineIETO 2022 OutlooklatifahNessuna valutazione finora

- Pakistan's State of The Electricity Generation and TransmissionDocumento8 paginePakistan's State of The Electricity Generation and TransmissionZaraNessuna valutazione finora

- International Virtual Course 2022 Dr. Musa PLNDocumento29 pagineInternational Virtual Course 2022 Dr. Musa PLNSivLy100% (1)

- Power Division of Energy GOP Year Book 2021-22Documento79 paginePower Division of Energy GOP Year Book 2021-22Aftab MuabarikNessuna valutazione finora

- HaDuong 2023 PDP8BoldStepDocumento5 pagineHaDuong 2023 PDP8BoldStepLuan RobertNessuna valutazione finora

- Status, Challenges and Forecast of The Philippines Wind IndustryDocumento28 pagineStatus, Challenges and Forecast of The Philippines Wind IndustryOlivia FilloneNessuna valutazione finora

- GB Power Sector Overview SituationDocumento3 pagineGB Power Sector Overview SituationAdditional secretary-1Nessuna valutazione finora

- PWC Indonesia Eum Newsflash 2016 59Documento4 paginePWC Indonesia Eum Newsflash 2016 59AndreNessuna valutazione finora

- 2015 Tanesco Presentation TansaniaDocumento27 pagine2015 Tanesco Presentation TansaniaShuaib MalikNessuna valutazione finora

- The Kimal Lo Aguirre HVDC Project: Chile's Decarbonization Transmission LineDocumento8 pagineThe Kimal Lo Aguirre HVDC Project: Chile's Decarbonization Transmission LineAdriana Q.Nessuna valutazione finora

- PTI Energy PolicyDocumento52 paginePTI Energy PolicyPTI Official100% (9)

- Energy PDFDocumento22 pagineEnergy PDFSultan AhmedNessuna valutazione finora

- The Energy Sector in Egypt - August 2023 - OstoulDocumento5 pagineThe Energy Sector in Egypt - August 2023 - Ostoulhesham zakiNessuna valutazione finora

- Power: Public SectorDocumento4 paginePower: Public SectorHitesh ShahNessuna valutazione finora

- Promotion of Hydro SectorDocumento2 paginePromotion of Hydro SectornamitaNessuna valutazione finora

- Renewable Pib-9Documento9 pagineRenewable Pib-9unwantedaccountno1Nessuna valutazione finora

- POGEE PowerTech Brochure 2020Documento4 paginePOGEE PowerTech Brochure 2020yasirsohaibNessuna valutazione finora

- Energy Transition Initiative Islands, Energy Snapshot Antigua and Barbuda, May 2015Documento4 pagineEnergy Transition Initiative Islands, Energy Snapshot Antigua and Barbuda, May 2015Detlef LoyNessuna valutazione finora

- 2832Documento27 pagine2832mhdsolehNessuna valutazione finora

- Energy Storage: Legal and Regulatory Challenges and OpportunitiesDa EverandEnergy Storage: Legal and Regulatory Challenges and OpportunitiesNessuna valutazione finora

- Power Sector OverviewDocumento9 paginePower Sector OverviewMuneer AhmedNessuna valutazione finora

- Energy Policy 2013 To 18Documento10 pagineEnergy Policy 2013 To 18Shine BrightNessuna valutazione finora

- 1.4 Power Sector MainDocumento24 pagine1.4 Power Sector MainAbhaSinghNessuna valutazione finora

- Solar Energy and Its Role in Sri Lanka: G.H.D.Wijesena, A.R.AmarasingheDocumento8 pagineSolar Energy and Its Role in Sri Lanka: G.H.D.Wijesena, A.R.AmarasingheLakshani AkalankaNessuna valutazione finora

- Power Shortages in PakistanDocumento4 paginePower Shortages in PakistanAmna SajidNessuna valutazione finora

- Indian Power Sector Analysis PDFDocumento9 pagineIndian Power Sector Analysis PDFvinay_814585077Nessuna valutazione finora

- Presentation-Shahid SaghirDocumento44 paginePresentation-Shahid SaghirpakistanacademyofengineeringNessuna valutazione finora

- Check For Answers. Hope You Will Find ItDocumento11 pagineCheck For Answers. Hope You Will Find ItMohammad Nazmul IslamNessuna valutazione finora

- Public & Private Participation in The Development of The Indian Power SectorDocumento19 paginePublic & Private Participation in The Development of The Indian Power SectorRashmi ChawlaNessuna valutazione finora

- Energy: Performance Review 2014-15Documento19 pagineEnergy: Performance Review 2014-15Muhammad SaqibNessuna valutazione finora

- Socoteco 2 Astro Energy Order,+ERC+Case+No.+2015-148+RCDocumento17 pagineSocoteco 2 Astro Energy Order,+ERC+Case+No.+2015-148+RCSamMooreNessuna valutazione finora

- Thailand Power Development Plan (PDPDocumento121 pagineThailand Power Development Plan (PDPlancelvanderhaven3130Nessuna valutazione finora

- Challenges Facing The Electricity Sector Industry in UgandaDocumento11 pagineChallenges Facing The Electricity Sector Industry in UgandaLucie Bulyaba100% (1)

- 013 Phi SsaDocumento6 pagine013 Phi SsamsreenaperezNessuna valutazione finora

- 14 EnergyDocumento20 pagine14 EnergyMehar HassanNessuna valutazione finora

- Energy & Environment: ENV-804 Dr. Muhammad Fahim KhokharDocumento69 pagineEnergy & Environment: ENV-804 Dr. Muhammad Fahim KhokharMuhammad Omamah SaeedNessuna valutazione finora

- Sri Lanka PresentationDocumento26 pagineSri Lanka PresentationADB_SAEN_ProjectsNessuna valutazione finora

- Banda GAsDocumento17 pagineBanda GAsRamswarup BhaskarNessuna valutazione finora

- Case Study PhilippinesDocumento4 pagineCase Study PhilippinesNelbert SumalpongNessuna valutazione finora

- Template Budget AnalysisDocumento18 pagineTemplate Budget AnalysisNasim HaidarNessuna valutazione finora

- KESC Case StudyDocumento6 pagineKESC Case Studyhira mateen100% (2)

- Cobp Phi 2013 2015 Ssa 02 PDFDocumento6 pagineCobp Phi 2013 2015 Ssa 02 PDFMhay VelascoNessuna valutazione finora

- Status of Indian Power Sector Dec 2023Documento13 pagineStatus of Indian Power Sector Dec 2023sonia raj gillNessuna valutazione finora

- Overview of Power SectorDocumento26 pagineOverview of Power SectorRameswar DashNessuna valutazione finora

- Power Sector - Opportunities and IssuesDocumento28 paginePower Sector - Opportunities and IssuesRamesh AnanthanarayananNessuna valutazione finora

- COMBINED1Documento24 pagineCOMBINED1AizNessuna valutazione finora

- (Assignment) PDFDocumento7 pagine(Assignment) PDFKnight》 MinhajNessuna valutazione finora

- Energy Transition Norway 2023Documento60 pagineEnergy Transition Norway 2023Andy PrimaNessuna valutazione finora

- Bangladesh Power System Enhancement and Efficiency Improvement Project-Additional Financing (RRP BAN 49423-006)Documento7 pagineBangladesh Power System Enhancement and Efficiency Improvement Project-Additional Financing (RRP BAN 49423-006)SajibNessuna valutazione finora

- Energy Sector in Pakistan: MembersDocumento25 pagineEnergy Sector in Pakistan: MembersHassan AhmedNessuna valutazione finora

- IcoldDocumento13 pagineIcoldkong yiNessuna valutazione finora

- Power Sector Scenario in India: Krishna Murari (009909) Dhiraj Arora (009915) Ranjan Kumar (009949) B.Subhakar (009910)Documento38 paginePower Sector Scenario in India: Krishna Murari (009909) Dhiraj Arora (009915) Ranjan Kumar (009949) B.Subhakar (009910)SamNessuna valutazione finora

- A Brighter Future for Maldives Powered by Renewables: Road Map for the Energy Sector 2020–2030Da EverandA Brighter Future for Maldives Powered by Renewables: Road Map for the Energy Sector 2020–2030Nessuna valutazione finora

- Driving the Green Transition: The Promise and Progress of Vehicle-to-Grid (V2G) SolutionsDa EverandDriving the Green Transition: The Promise and Progress of Vehicle-to-Grid (V2G) SolutionsNessuna valutazione finora

- EU China Energy Magazine 2023 September Issue: 2023, #8Da EverandEU China Energy Magazine 2023 September Issue: 2023, #8Nessuna valutazione finora

- Lapse RateDocumento23 pagineLapse RateJamal JalalaniNessuna valutazione finora

- Coal AnylysisDocumento19 pagineCoal AnylysisJamal JalalaniNessuna valutazione finora

- Sources of Air Pollution PDFDocumento30 pagineSources of Air Pollution PDFJamal Jalalani100% (1)

- Flow of FluidDocumento28 pagineFlow of FluidJamal JalalaniNessuna valutazione finora

- Types of CoalDocumento43 pagineTypes of CoalJamal JalalaniNessuna valutazione finora

- Environmental Controls I/IGDocumento37 pagineEnvironmental Controls I/IGJamal JalalaniNessuna valutazione finora

- Crystallographic PointsDocumento10 pagineCrystallographic PointsJamal JalalaniNessuna valutazione finora

- Basic Concept of MeasurementDocumento48 pagineBasic Concept of MeasurementJamal JalalaniNessuna valutazione finora

- 6-Moments Couples and Force Couple SystemsDocumento69 pagine6-Moments Couples and Force Couple SystemsJamal JalalaniNessuna valutazione finora

- EasyPact EZC - EZC100H3100Documento6 pagineEasyPact EZC - EZC100H3100Abdulraheem SalmanNessuna valutazione finora

- HBL Ni CD VRPP Battery SpecsDocumento18 pagineHBL Ni CD VRPP Battery SpecsSanjeev DhariwalNessuna valutazione finora

- Wireless Power TransmissionDocumento25 pagineWireless Power TransmissionT ROHIT SINGHNessuna valutazione finora

- Design of Intake ManifoldDocumento6 pagineDesign of Intake ManifoldShailendra SinghNessuna valutazione finora

- Mar, 2011 - News - SANYO Asia Pacific RegionDocumento2 pagineMar, 2011 - News - SANYO Asia Pacific RegionTham Chee AunNessuna valutazione finora

- LGBR ReportDocumento107 pagineLGBR Reportayush1001Nessuna valutazione finora

- Squared ArrancadoresDocumento154 pagineSquared ArrancadoresAlex RamirezNessuna valutazione finora

- Sistemas Eléctricos de Potencia (SEP) : Repaso Sistema en Por UnidadDocumento13 pagineSistemas Eléctricos de Potencia (SEP) : Repaso Sistema en Por UnidadBraulio GutiérrezNessuna valutazione finora

- Victron Pylontech Up2500 Us2000 Us3000 Us2000c Us3000c Us5000 Us5000b Us5000c Pelio-L Up5000 Phantom-S Force-L1 l2Documento15 pagineVictron Pylontech Up2500 Us2000 Us3000 Us2000c Us3000c Us5000 Us5000b Us5000c Pelio-L Up5000 Phantom-S Force-L1 l2Warren MorseNessuna valutazione finora

- Shree Cement LTD, Bangurcity: HALF YEARLY / YEARLY CHECK LIST For Monitoring of Earthing System (Earth Pits) (4 X 18 MW)Documento8 pagineShree Cement LTD, Bangurcity: HALF YEARLY / YEARLY CHECK LIST For Monitoring of Earthing System (Earth Pits) (4 X 18 MW)Stephen BridgesNessuna valutazione finora

- Internship Report: Chevron Indonesia CompanyDocumento48 pagineInternship Report: Chevron Indonesia CompanyWilliam AndreasNessuna valutazione finora

- Green BuildingDocumento10 pagineGreen BuildingvishalNessuna valutazione finora

- J. J. Tabarek, Dale E. Klein and James R. Fair Center For Energy Studies The University Aftexas at Austin Austin, Texas 78712Documento6 pagineJ. J. Tabarek, Dale E. Klein and James R. Fair Center For Energy Studies The University Aftexas at Austin Austin, Texas 78712José Blanco MosqueraNessuna valutazione finora

- Chapter 4 Standards 2021Documento19 pagineChapter 4 Standards 2021Bamrung SungnoenNessuna valutazione finora

- CourseBOOKv5 PDFDocumento132 pagineCourseBOOKv5 PDFantilelosNessuna valutazione finora

- IT - PVS800 - FW - A - With Update Notice - 12 - 2011Documento148 pagineIT - PVS800 - FW - A - With Update Notice - 12 - 2011Deiva KNessuna valutazione finora

- Circulating Fluidized Bed Reactor Design and TheoryDocumento28 pagineCirculating Fluidized Bed Reactor Design and TheoryMehran Rasheed Goraya100% (3)

- Fault Contribution of Grid Connected InvertersDocumento5 pagineFault Contribution of Grid Connected InverterssimonNessuna valutazione finora

- Handbook For Developing Micro Hydro in British Columbia: March 23, 2004Documento69 pagineHandbook For Developing Micro Hydro in British Columbia: March 23, 2004Armand Doru DomutaNessuna valutazione finora

- Satcon PVS 250 PV-Inverter Manual PM00457R1man (250kW UL Dec 08)Documento126 pagineSatcon PVS 250 PV-Inverter Manual PM00457R1man (250kW UL Dec 08)nicklionsNessuna valutazione finora

- GT HistoryDocumento12 pagineGT HistoryBrosGeeNessuna valutazione finora

- Effect of Coal Moisture On Denitration Efficiency and Boiler EconomyDocumento7 pagineEffect of Coal Moisture On Denitration Efficiency and Boiler EconomyRc TuppalNessuna valutazione finora

- Epa 2039Documento1 paginaEpa 2039tomas riojasNessuna valutazione finora

- Prophi PDFDocumento2 pagineProphi PDFfrostestNessuna valutazione finora

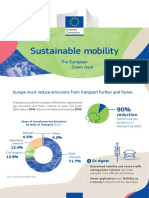

- Sustainable Mobility: The European Green DealDocumento2 pagineSustainable Mobility: The European Green DealZhen Kai OngNessuna valutazione finora

- LNG Journal 2018 01 January0Documento36 pagineLNG Journal 2018 01 January0Karima BelbraikNessuna valutazione finora

- Steca Solarix PRS Instruction English - Uputstvo Solarni PaneliDocumento10 pagineSteca Solarix PRS Instruction English - Uputstvo Solarni PaneliAleksandar StankovićNessuna valutazione finora

- Canlubo - Worksheet 3 NSTP 2Documento2 pagineCanlubo - Worksheet 3 NSTP 2Alyssa CanluboNessuna valutazione finora

- RT W48100 - RT W48200 Powerwall Lithium Ion Phosphate Battery User Manual - 20221109 - 2Documento16 pagineRT W48100 - RT W48200 Powerwall Lithium Ion Phosphate Battery User Manual - 20221109 - 2BLAZE TECHNessuna valutazione finora

- Laporan Praktik Mesin ListrikDocumento4 pagineLaporan Praktik Mesin ListrikFatimah azzahraNessuna valutazione finora