Potrebbero piacerti anche

- Inventories - TheoriesDocumento9 pagineInventories - TheoriesIrisNessuna valutazione finora

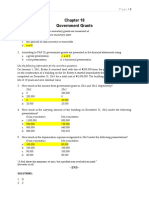

- Government Grants: Use The Following Information For The Next Three QuestionsDocumento2 pagineGovernment Grants: Use The Following Information For The Next Three QuestionsJEFFERSON CUTENessuna valutazione finora

- FAR REVIEWER Part 1Documento7 pagineFAR REVIEWER Part 1jessamae gundanNessuna valutazione finora

- Provisions, Contingent Liabilities and Contingent AssetDocumento37 pagineProvisions, Contingent Liabilities and Contingent AssetAbdulhafiz100% (1)

- Pas 32 Financial InstrumentsDocumento15 paginePas 32 Financial Instrumentsaly salvatierraNessuna valutazione finora

- ReceivablesDocumento4 pagineReceivablesKentaro Panergo NumasawaNessuna valutazione finora

- PAS 38 Intangible Assets PowerpointDocumento18 paginePAS 38 Intangible Assets PowerpointYassi CurtisNessuna valutazione finora

- Merchadising MOCK QUIZDocumento5 pagineMerchadising MOCK QUIZCarl Dhaniel Garcia SalenNessuna valutazione finora

- Property, Plant and EquipmentDocumento40 pagineProperty, Plant and EquipmentNatalie SerranoNessuna valutazione finora

- Conceptual-Framework-and-Accounting-Standards-REVIEW-SERIES Part 1Documento135 pagineConceptual-Framework-and-Accounting-Standards-REVIEW-SERIES Part 1leahlynsantos14100% (1)

- Chapter 21 - Reclassification of Financial Asset PDFDocumento9 pagineChapter 21 - Reclassification of Financial Asset PDFTurksNessuna valutazione finora

- Test Bank For Cornerstones of Cost Management 2nd Edition by Hansen PDFDocumento23 pagineTest Bank For Cornerstones of Cost Management 2nd Edition by Hansen PDFJyasmine Aura V. AgustinNessuna valutazione finora

- Chapter 33 - Financial Asset at Amortized Cost (Fair Value Option)Documento1 paginaChapter 33 - Financial Asset at Amortized Cost (Fair Value Option)Ianna ManieboNessuna valutazione finora

- Module 5. Part 1 PPEDocumento64 pagineModule 5. Part 1 PPElord kwantoniumNessuna valutazione finora

- Activity-Based Costing True-False StatementsDocumento5 pagineActivity-Based Costing True-False StatementsSuman Paul ChowdhuryNessuna valutazione finora

- Chapter 26 Land and BuildingDocumento17 pagineChapter 26 Land and BuildingKendall JennerNessuna valutazione finora

- AE 18 Financial Market Prelim ExamDocumento3 pagineAE 18 Financial Market Prelim ExamWenjunNessuna valutazione finora

- CFAS PPT 25 - PAS 40 (Investment Property)Documento23 pagineCFAS PPT 25 - PAS 40 (Investment Property)Asheh DinsuatNessuna valutazione finora

- AIS 01 - Handout - 1Documento7 pagineAIS 01 - Handout - 1Melchie RepospoloNessuna valutazione finora

- Direct Method or Cost of Goods Sold MethodDocumento2 pagineDirect Method or Cost of Goods Sold MethodNa Dem DolotallasNessuna valutazione finora

- Chapter 10 - Intermediate AccountingDocumento4 pagineChapter 10 - Intermediate AccountingPrincess PriyaNessuna valutazione finora

- Borrowing Cost DrillDocumento2 pagineBorrowing Cost DrillJasmin Rabon0% (1)

- JIT SystemDocumento2 pagineJIT SystemJona FranciscoNessuna valutazione finora

- Accounting For Special TransactionsDocumento13 pagineAccounting For Special Transactionsviva nazarenoNessuna valutazione finora

- Chapter 28 - Gross Profit and Retail Method: ANSWER 28-1Documento12 pagineChapter 28 - Gross Profit and Retail Method: ANSWER 28-1Cyrus IsanaNessuna valutazione finora

- Lecture Notes On Biological Assets and Agricultural Produce - 000Documento5 pagineLecture Notes On Biological Assets and Agricultural Produce - 000judel ArielNessuna valutazione finora

- Finished Goods Inventory: Exercise 1-1 (True or False)Documento16 pagineFinished Goods Inventory: Exercise 1-1 (True or False)Isaiah BatucanNessuna valutazione finora

- IAcctg1 Accounts Receivable ActivitiesDocumento10 pagineIAcctg1 Accounts Receivable ActivitiesYulrir Alesteyr HiroshiNessuna valutazione finora

- LCNRV - SolutionDocumento3 pagineLCNRV - SolutionMagadia Mark JeffNessuna valutazione finora

- Cost of Goods Manufactured Income Statement Norton IndustriesDocumento2 pagineCost of Goods Manufactured Income Statement Norton IndustriesAmit PandeyNessuna valutazione finora

- FAR.2904 - Accounting For Agricultural Activity.Documento5 pagineFAR.2904 - Accounting For Agricultural Activity.John Nathan Kingly100% (1)

- Chapter 1-Basic-Concepts-and-Job-Order-Cost-CycleDocumento21 pagineChapter 1-Basic-Concepts-and-Job-Order-Cost-CycleRhodoraNessuna valutazione finora

- Friendship CoDocumento3 pagineFriendship CoKeahlyn BoticarioNessuna valutazione finora

- Quiz 4 - Unit 4 - Investment in Equity Securities Quiz InstructionsDocumento22 pagineQuiz 4 - Unit 4 - Investment in Equity Securities Quiz InstructionsCharmaine Mari OlmosNessuna valutazione finora

- Pricing Decision and Cost MGMNT QuizDocumento2 paginePricing Decision and Cost MGMNT QuizEwelina ChabowskaNessuna valutazione finora

- Question 6: Ias 38 Intangible Assets: Page 1 of 2Documento2 pagineQuestion 6: Ias 38 Intangible Assets: Page 1 of 2tazil shahNessuna valutazione finora

- MidtermsDocumento8 pagineMidtermsRhea BadanaNessuna valutazione finora

- Acc 124 - Week 13-14 - Ulob - Investment in Equity Securities - Assignment - CainDocumento2 pagineAcc 124 - Week 13-14 - Ulob - Investment in Equity Securities - Assignment - Cainslow dancerNessuna valutazione finora

- First Time Adoption of PFRSDocumento5 pagineFirst Time Adoption of PFRSPia ArellanoNessuna valutazione finora

- Intermediate Accounting 1: Brief Discussion On Notes Receivable and Other Receivable ConceptsDocumento26 pagineIntermediate Accounting 1: Brief Discussion On Notes Receivable and Other Receivable ConceptsMckenzieNessuna valutazione finora

- INTACC1 Inventory ProblemsDocumento3 pagineINTACC1 Inventory ProblemsButterfly 0719Nessuna valutazione finora

- MGT 209 - CH 13 NotesDocumento6 pagineMGT 209 - CH 13 NotesAmiel Christian MendozaNessuna valutazione finora

- 211 EO Finals REVIEWERDocumento9 pagine211 EO Finals REVIEWERmarites yuNessuna valutazione finora

- Activity - Allocation of Service Department Problem 1: Total Cost For FOH Rate ComputationDocumento2 pagineActivity - Allocation of Service Department Problem 1: Total Cost For FOH Rate ComputationNick ivan AlvaresNessuna valutazione finora

- Bfar ReviewerDocumento6 pagineBfar Reviewerraimefaye seduconNessuna valutazione finora

- Mon Exam.21221sDocumento2 pagineMon Exam.21221sNicole Anne Santiago SibuloNessuna valutazione finora

- 07 Lecture Notes - Gross Profit and Retail Method PDFDocumento1 pagina07 Lecture Notes - Gross Profit and Retail Method PDFJobelle Gallardo AgasNessuna valutazione finora

- Revaluation QUIZ PDFDocumento12 pagineRevaluation QUIZ PDFMina LouveryNessuna valutazione finora

- Lecture Notes On Borrowing Costs - 000Documento3 pagineLecture Notes On Borrowing Costs - 000judel ArielNessuna valutazione finora

- Week 4 - Lesson 4 Cash and Cash EquivalentsDocumento21 pagineWeek 4 - Lesson 4 Cash and Cash EquivalentsRose RaboNessuna valutazione finora

- C14 - PAS 2 InventoriesDocumento20 pagineC14 - PAS 2 InventoriesAllaine ElfaNessuna valutazione finora

- CFAS FinalsDocumento7 pagineCFAS FinalsMarriel Fate CullanoNessuna valutazione finora

- Quiz - Chapter 10 - Investments in Debt Securities - Ia 1 - 2020 EditionDocumento3 pagineQuiz - Chapter 10 - Investments in Debt Securities - Ia 1 - 2020 EditionJennifer RelosoNessuna valutazione finora

- Midterms Conceptual Framework and Accounting StandardsDocumento9 pagineMidterms Conceptual Framework and Accounting StandardsMay Anne MenesesNessuna valutazione finora

- Cfas - Chapter 8: Pas 1 - Presentation of Financial STATEMENTS (Statement of Financial Position)Documento2 pagineCfas - Chapter 8: Pas 1 - Presentation of Financial STATEMENTS (Statement of Financial Position)agm25Nessuna valutazione finora

- Prelim Exam - Intermediate Accounting Part 1Documento13 paginePrelim Exam - Intermediate Accounting Part 1Vincent AbellaNessuna valutazione finora

- Ias 38 Intangible AssetsDocumento4 pagineIas 38 Intangible AssetsYogesh BhattaraiNessuna valutazione finora

- Ias 38Documento7 pagineIas 38Researcher BrianNessuna valutazione finora

- IAS 38 - Intangible AssetsDocumento27 pagineIAS 38 - Intangible AssetsArshad BhuttaNessuna valutazione finora

- IAS#38Documento43 pagineIAS#38Shah KamalNessuna valutazione finora

- Answers To All Multiple-Choice Questions From The Textbook (Messier Et Al. 8)Documento30 pagineAnswers To All Multiple-Choice Questions From The Textbook (Messier Et Al. 8)natiNessuna valutazione finora

- Non Current Asset Held For Sale Final-1Documento29 pagineNon Current Asset Held For Sale Final-1nati100% (4)

- AU Section 350 - Audit SamplingDocumento5 pagineAU Section 350 - Audit SamplingnatiNessuna valutazione finora

- Course Name: Communication Theories Instructor: Emrakeb AssefaDocumento20 pagineCourse Name: Communication Theories Instructor: Emrakeb AssefanatiNessuna valutazione finora

- Shsssort For PreseDocumento24 pagineShsssort For PresenatiNessuna valutazione finora

- Joint Arrangement & Investment in Associate, Suger 2ndDocumento36 pagineJoint Arrangement & Investment in Associate, Suger 2ndnatiNessuna valutazione finora

- Liablities Provision and Contingences Suger FactoryDocumento49 pagineLiablities Provision and Contingences Suger FactorynatiNessuna valutazione finora

- ImpairmentDocumento45 pagineImpairmentnati100% (1)

- Table 3: Optional Exemptions From Retrospective ApplicationDocumento3 pagineTable 3: Optional Exemptions From Retrospective ApplicationnatiNessuna valutazione finora

- IntroductionDocumento83 pagineIntroductionnatiNessuna valutazione finora

- LeasesDocumento57 pagineLeasesnati50% (2)

- IFRS 15 New FridayDocumento73 pagineIFRS 15 New Fridaynati67% (3)

- IFRS 1 - For PresDocumento27 pagineIFRS 1 - For Presnati67% (3)

- Income TaxDocumento36 pagineIncome Taxnati100% (1)

- IAS - 23 - Borrowing - Costs For EditedDocumento23 pagineIAS - 23 - Borrowing - Costs For Editednati100% (1)

- Events After The Reporting Period Final 6 KiloDocumento13 pagineEvents After The Reporting Period Final 6 Kilonati100% (1)

- Fair ValueDocumento44 pagineFair Valuenati100% (1)

- Government GrantDocumento14 pagineGovernment GrantnatiNessuna valutazione finora

- Employee BenefitDocumento32 pagineEmployee BenefitnatiNessuna valutazione finora

- IAS - 23 - Borrowing - Costs Edited 6 KiloDocumento19 pagineIAS - 23 - Borrowing - Costs Edited 6 KilonatiNessuna valutazione finora

- Cash & ReceivablesDocumento53 pagineCash & Receivablesnati100% (1)

- Case Study For Discussion Borrowing CostsDocumento2 pagineCase Study For Discussion Borrowing Costsnati100% (1)

- Biological Assets RivisedDocumento45 pagineBiological Assets Rivisednati100% (2)

- Employee BenefitDocumento32 pagineEmployee BenefitnatiNessuna valutazione finora

- Cash and Receivables - 6Documento52 pagineCash and Receivables - 6natiNessuna valutazione finora

- Accounting PolicyDocumento50 pagineAccounting Policynati100% (2)

- Indigo AirlineDocumento23 pagineIndigo AirlineSayali DiwateNessuna valutazione finora

- Pricing ModelsDocumento9 paginePricing ModelshimanshiNessuna valutazione finora

- October10 March11 - 7 21 11final 1Documento351 pagineOctober10 March11 - 7 21 11final 1jc247977Nessuna valutazione finora

- ICF SEA ICF RegionalIslamic Crowdfunding in SEAArticle Islamic Crowd Funding in Singapore and IndonesiaDocumento7 pagineICF SEA ICF RegionalIslamic Crowdfunding in SEAArticle Islamic Crowd Funding in Singapore and IndonesiaKetoisophorone WongNessuna valutazione finora

- Chapter 2Documento15 pagineChapter 2lordaiztrandNessuna valutazione finora

- Ge Six SigmaDocumento14 pagineGe Six SigmagauravnanjaniNessuna valutazione finora

- ISA 260 Revised 1Documento24 pagineISA 260 Revised 1dzenita5beciragic5kaNessuna valutazione finora

- IAS 10 Events After The Reporting Period-A Closer LookDocumento7 pagineIAS 10 Events After The Reporting Period-A Closer LookFahmi AbdullaNessuna valutazione finora

- MAT App.8.17.16Documento465 pagineMAT App.8.17.16Anonymous 1BWhWDBNessuna valutazione finora

- Casos Practics 2011-2012Documento136 pagineCasos Practics 2011-2012robertomazoarrNessuna valutazione finora

- Meaning Bank GuaranteeDocumento12 pagineMeaning Bank GuaranteemydeanzNessuna valutazione finora

- State Bank of India - Wikipedia, The Free EncyclopediaDocumento9 pagineState Bank of India - Wikipedia, The Free EncyclopediaSai BabaNessuna valutazione finora

- AbdulQuaderAmshan (10 0)Documento4 pagineAbdulQuaderAmshan (10 0)suku_mcaNessuna valutazione finora

- Poea Requirements ChecklistDocumento1 paginaPoea Requirements ChecklistChristine Pestano SakaiNessuna valutazione finora

- Tutorial 4Documento2 pagineTutorial 4aly0% (1)

- Infibeam RHPDocumento397 pagineInfibeam RHPJenil ShahNessuna valutazione finora

- chapter 3 - 題庫Documento35 paginechapter 3 - 題庫lo030275% (4)

- Teenage Mutant Ninja Turtles Classics, Vol. 7 PreviewDocumento14 pagineTeenage Mutant Ninja Turtles Classics, Vol. 7 PreviewGraphic Policy67% (3)

- CMI Energy Reference ListDocumento24 pagineCMI Energy Reference Listthanhtbk2000Nessuna valutazione finora

- Merger Cases PDFDocumento51 pagineMerger Cases PDFmayur kulkarniNessuna valutazione finora

- Strategic Risk Management: The New Competitive EdgeDocumento11 pagineStrategic Risk Management: The New Competitive EdgesammirtoNessuna valutazione finora

- Comparative Study of Life Time Plans at Airtel by Zamir KaziDocumento58 pagineComparative Study of Life Time Plans at Airtel by Zamir Kaziraghuram952Nessuna valutazione finora

- Unit 4 - Institutional Support To Small and Medium EnterprisesDocumento24 pagineUnit 4 - Institutional Support To Small and Medium EnterprisesYash GargNessuna valutazione finora

- Boynton SM Ch.19Documento22 pagineBoynton SM Ch.19Eza R100% (1)

- 42 47 ListDocumento6 pagine42 47 ListMartha DewaNessuna valutazione finora

- Sample 25M LinkedinDocumento6 pagineSample 25M LinkedinAakash MaratheNessuna valutazione finora

- Stages of InternationalizationDocumento28 pagineStages of Internationalizationpujaadi100% (3)

- HRM Case PPT FinalDocumento14 pagineHRM Case PPT FinalVaibhav Kumar0% (1)

- IncomeTax CalculatorDocumento2 pagineIncomeTax Calculatormurarirahul100% (3)

- Strategic Control and Corporate GovernanceDocumento18 pagineStrategic Control and Corporate GovernanceDavid Ako100% (2)