Potrebbero piacerti anche

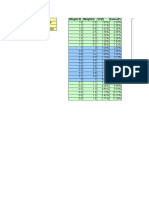

- Efficient Frontier: Bond Stock Weight (B) Weight (S) SD (P) Return (P)Documento2 pagineEfficient Frontier: Bond Stock Weight (B) Weight (S) SD (P) Return (P)ozgunlimanNessuna valutazione finora

- Financial AnalysisDocumento21 pagineFinancial AnalysisozgunlimanNessuna valutazione finora

- Risk ReturnDocumento40 pagineRisk ReturnozgunlimanNessuna valutazione finora

- Case Report GuidelinesDocumento2 pagineCase Report GuidelinesozgunlimanNessuna valutazione finora

- Risk ReturnDocumento40 pagineRisk ReturnozgunlimanNessuna valutazione finora

- Jones QuestionsDocumento1 paginaJones QuestionsozgunlimanNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Overview of Oracle Project BillingDocumento125 pagineOverview of Oracle Project Billingmukesh697100% (2)

- Audit of LiabilitiesDocumento6 pagineAudit of LiabilitiesEdmar HalogNessuna valutazione finora

- TAB Whitepaper R13 18 05Documento49 pagineTAB Whitepaper R13 18 05Kishan Bussa100% (1)

- LectureNotesOnCash and Accrual AccountingDocumento2 pagineLectureNotesOnCash and Accrual AccountingApril Joy ObedozaNessuna valutazione finora

- Solutions - Chapter 2Documento29 pagineSolutions - Chapter 2Dre ThathipNessuna valutazione finora

- Financial Accounting - Chapter 4Documento57 pagineFinancial Accounting - Chapter 4Hamza PagaNessuna valutazione finora

- ING Bank Vs CIRDocumento28 pagineING Bank Vs CIRiamchurkyNessuna valutazione finora

- Cohen Finance Workbook FALL 2013Documento124 pagineCohen Finance Workbook FALL 2013Nayef AbdullahNessuna valutazione finora

- Case Digest PDFDocumento4 pagineCase Digest PDFJustine Jay Casas LopeNessuna valutazione finora

- Chapter 1: Overview of Government Accounting: Exam ReviewerDocumento22 pagineChapter 1: Overview of Government Accounting: Exam ReviewerStudent 101Nessuna valutazione finora

- Prin CH 4 - 6Documento18 paginePrin CH 4 - 6Gizachew NadewNessuna valutazione finora

- PROBLEMSDocumento19 paginePROBLEMSlalalalaNessuna valutazione finora

- Chapter17 Incomplete RecordsDocumento24 pagineChapter17 Incomplete Recordsmustafakarim100% (1)

- Acc 418Documento379 pagineAcc 418sigirya100% (2)

- Chapter 2 Accounting For Accruals and Deferrals: Fundamental Financial Accounting Concepts, 10e (Edmonds)Documento45 pagineChapter 2 Accounting For Accruals and Deferrals: Fundamental Financial Accounting Concepts, 10e (Edmonds)brockNessuna valutazione finora

- The Accounting Cycle: Accruals and DeferralsDocumento70 pagineThe Accounting Cycle: Accruals and DeferralsNajat Abizeid SamahaNessuna valutazione finora

- Chapter 11 Balance SheetDocumento12 pagineChapter 11 Balance SheetSha HussainNessuna valutazione finora

- Bos 54380 CP 6Documento198 pagineBos 54380 CP 6Sourabh YadavNessuna valutazione finora

- Designing Billing Extensions in OracleDocumento24 pagineDesigning Billing Extensions in OracleYugwan MittalNessuna valutazione finora

- Ch01 Liabilities ProblemsDocumento6 pagineCh01 Liabilities ProblemsJessica AllyNessuna valutazione finora

- Accounting GuideDocumento153 pagineAccounting Guidebam04100% (1)

- T0 2022-2023 MS FA - Offenbach - SolutionDocumento7 pagineT0 2022-2023 MS FA - Offenbach - SolutionPAURUSH GUPTANessuna valutazione finora

- FAR NotesDocumento163 pagineFAR NotesClaire Antonette Limpangog100% (1)

- Philippine International Trading Corporation vs. COADocumento9 paginePhilippine International Trading Corporation vs. COAAKnownKneeMouseeNessuna valutazione finora

- BAAN ERP User Guide Analyze AcrDocumento57 pagineBAAN ERP User Guide Analyze Acrkoos_engelbrechtNessuna valutazione finora

- Accruals and PrepaymentsDocumento2 pagineAccruals and PrepaymentsPriya NairNessuna valutazione finora

- Chapter 1 Financial AccountingDocumento10 pagineChapter 1 Financial AccountingMarcelo Iuki HirookaNessuna valutazione finora

- FAR1 - Lecture 04 Adjusting Entries - Step 5Documento6 pagineFAR1 - Lecture 04 Adjusting Entries - Step 5Patricia Camille AustriaNessuna valutazione finora

- Global Absence FastFormula User Guide 20201123Documento119 pagineGlobal Absence FastFormula User Guide 20201123Sachiin ShiirkeNessuna valutazione finora

- Adjustment On Income and ExpensesDocumento26 pagineAdjustment On Income and ExpensesSharanya SharaNessuna valutazione finora