Potrebbero piacerti anche

- Chapter 3 Cost of CapitalDocumento30 pagineChapter 3 Cost of CapitalMELAT ROBELNessuna valutazione finora

- Group 4 Assignment Campus Deli 1Documento9 pagineGroup 4 Assignment Campus Deli 1namitasharma1512100% (4)

- BECO110-Assignment1-2012 10 05Documento4 pagineBECO110-Assignment1-2012 10 05Price100% (2)

- Applied Corporate Finance. What is a Company worth?Da EverandApplied Corporate Finance. What is a Company worth?Valutazione: 3 su 5 stelle3/5 (2)

- Excavation Works Cost FactorsDocumento22 pagineExcavation Works Cost FactorsSyakir Sulaiman100% (1)

- Project Report On Marketing Strategy For BbaDocumento78 pagineProject Report On Marketing Strategy For BbaNeera Tomar75% (8)

- International Business and Trade Presentation 1Documento33 pagineInternational Business and Trade Presentation 1PATRICIA ANGELA MERALPEZNessuna valutazione finora

- TOPIC 6c - Cost of Capital and Capital StructureDocumento42 pagineTOPIC 6c - Cost of Capital and Capital StructureYasskidayo Hammyson100% (1)

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingDa EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNessuna valutazione finora

- The Strategy - HHLL: How To Draw The SetupDocumento8 pagineThe Strategy - HHLL: How To Draw The SetupPermanaNessuna valutazione finora

- 26 RSI TrendsDocumento3 pagine26 RSI Trendslowtarhk67% (6)

- Capital StructureDocumento59 pagineCapital StructureRajendra MeenaNessuna valutazione finora

- Summary of Aswath Damodaran's The Little Book of ValuationDa EverandSummary of Aswath Damodaran's The Little Book of ValuationNessuna valutazione finora

- Capital Structure DecisionsDocumento35 pagineCapital Structure DecisionskiruthekaNessuna valutazione finora

- IAS 36 Impairment of AssetsDocumento29 pagineIAS 36 Impairment of AssetsEmms Adelaine TulaganNessuna valutazione finora

- Companion To Neo-Schumpeterian EconomicsDocumento1.229 pagineCompanion To Neo-Schumpeterian EconomicsFAUSTINOESTEBAN100% (2)

- Chap8 Cost of CapitalDocumento75 pagineChap8 Cost of CapitalBaby Khor50% (2)

- R R D DE R E DE R R R D DE: Modigliani-Miller TheoremDocumento13 pagineR R D DE R E DE R R R D DE: Modigliani-Miller TheoremPankaj Kumar BaidNessuna valutazione finora

- Hult Prize. 2016 Case Study - FINALDocumento28 pagineHult Prize. 2016 Case Study - FINALAlvaro PuertasNessuna valutazione finora

- CH 9-The Cost of Capital by IM PandeyDocumento36 pagineCH 9-The Cost of Capital by IM PandeyJyoti Bansal89% (9)

- Capital StructureDocumento41 pagineCapital StructurethejojoseNessuna valutazione finora

- Weighted Average Cost of CapitalDocumento20 pagineWeighted Average Cost of CapitalSamuel NjengaNessuna valutazione finora

- Cost of CapitalDocumento99 pagineCost of CapitalRajesh GovardhanNessuna valutazione finora

- CFM - Lecture 1 - Capital Structure TheoryDocumento116 pagineCFM - Lecture 1 - Capital Structure TheoryJelien TaselaarNessuna valutazione finora

- CapStr 1 NTDocumento40 pagineCapStr 1 NTWong Yong Sheng WongNessuna valutazione finora

- Capital Structure Theory and ApplicationsDocumento288 pagineCapital Structure Theory and ApplicationsGen AbulkhairNessuna valutazione finora

- MFCF - Session 5Documento49 pagineMFCF - Session 5Ondřej HengeričNessuna valutazione finora

- Raising Capital and Capital Structure IDocumento25 pagineRaising Capital and Capital Structure ILee ChiaNessuna valutazione finora

- Cost of Capital LEC3 ACFDocumento5 pagineCost of Capital LEC3 ACFHeart BukkabiNessuna valutazione finora

- Long-Term Analysis of Debt PolicyDocumento77 pagineLong-Term Analysis of Debt PolicyRounakNessuna valutazione finora

- CF Lecture 4 Cost of Capital v1Documento43 pagineCF Lecture 4 Cost of Capital v1Tâm NhưNessuna valutazione finora

- WACC and Company Valuation ChapterDocumento75 pagineWACC and Company Valuation ChapterArneet SarnaNessuna valutazione finora

- Capital Structure and Cost of CapitalDocumento6 pagineCapital Structure and Cost of CapitalSam DevineNessuna valutazione finora

- Final Doc of Management AssignmentDocumento10 pagineFinal Doc of Management AssignmentrasithapradeepNessuna valutazione finora

- Lecture Set 5Documento23 pagineLecture Set 5api-27554485Nessuna valutazione finora

- Fin440 Chapter 14 v.2Documento36 pagineFin440 Chapter 14 v.2Lutfun Nesa AyshaNessuna valutazione finora

- Lecture 11Documento51 pagineLecture 11Janice JingNessuna valutazione finora

- Cap. Structure 5-4-20Documento20 pagineCap. Structure 5-4-20zaid saadNessuna valutazione finora

- The Cost of Capital, Capital Structure and Dividend PolicyuitsDocumento33 pagineThe Cost of Capital, Capital Structure and Dividend PolicyuitsArafath RahmanNessuna valutazione finora

- Chapter 14Documento53 pagineChapter 14Kwesi WiafeNessuna valutazione finora

- Capital StructureDocumento43 pagineCapital Structurebhavya kakumanuNessuna valutazione finora

- Chapter 14 0Documento41 pagineChapter 14 0Thiên CầmNessuna valutazione finora

- FM CH 15 PDFDocumento50 pagineFM CH 15 PDFLayatmika SahooNessuna valutazione finora

- Optimal Capital Structure and Cost of CapitalDocumento16 pagineOptimal Capital Structure and Cost of CapitalYariko ChieNessuna valutazione finora

- Chapte R: Capital Structure: Theory and PolicyDocumento50 pagineChapte R: Capital Structure: Theory and PolicySid SharmaNessuna valutazione finora

- Lecture 10Documento16 pagineLecture 10Kabristan ChokidarNessuna valutazione finora

- Cost of CapitalDocumento15 pagineCost of Capitalসুজয় দত্তNessuna valutazione finora

- FM Ch7 Corporate FinancingDocumento60 pagineFM Ch7 Corporate Financingtemesgen yohannesNessuna valutazione finora

- Capital StructureDocumento28 pagineCapital Structureluvnica6348Nessuna valutazione finora

- Capital Structure TheoriesDocumento17 pagineCapital Structure Theoriesvijayjeo100% (1)

- Week 1 Introduction and Capital Structure in A Perfect MarketDocumento12 pagineWeek 1 Introduction and Capital Structure in A Perfect MarketAndrew NguyenNessuna valutazione finora

- SOF Questions - With - AnswersDocumento33 pagineSOF Questions - With - AnswersКамиль БайбуринNessuna valutazione finora

- Financial Management-Module 2 NewDocumento29 pagineFinancial Management-Module 2 New727822TPMB005 ARAVINTHAN.SNessuna valutazione finora

- Maximizing Firm Value with Optimal Capital StructureDocumento11 pagineMaximizing Firm Value with Optimal Capital StructurebashirNessuna valutazione finora

- Q1) What Is Cost of Capital? How Is It Calculated For Different Sources of Capital? How Is Average Weighted Cost of Capital Measured?Documento18 pagineQ1) What Is Cost of Capital? How Is It Calculated For Different Sources of Capital? How Is Average Weighted Cost of Capital Measured?udayvadapalliNessuna valutazione finora

- Capital Structure Decision - Babcock UniversityDocumento23 pagineCapital Structure Decision - Babcock UniversityTAYO AYODEJI AROWOSEGBENessuna valutazione finora

- My Apv NotesDocumento22 pagineMy Apv NotesAbhishekKumarNessuna valutazione finora

- Capital Structure Decisions Chapter 15 and 16: Financial Policy and Planning (MB 29)Documento14 pagineCapital Structure Decisions Chapter 15 and 16: Financial Policy and Planning (MB 29)sankhajitghoshNessuna valutazione finora

- Financial Management Cost Of Capital ExplainedDocumento17 pagineFinancial Management Cost Of Capital ExplainedKunal GargNessuna valutazione finora

- Cost of CapitalDocumento24 pagineCost of CapitalShounak SarkarNessuna valutazione finora

- Capital StructureDocumento31 pagineCapital StructuresanNessuna valutazione finora

- Overview of WaccDocumento19 pagineOverview of Waccসুজয় দত্তNessuna valutazione finora

- Capital Structure Decisions ExplainedDocumento63 pagineCapital Structure Decisions ExplainedHawraa AlabbasNessuna valutazione finora

- Corporate Finance Assignment 5Documento3 pagineCorporate Finance Assignment 5amitchellpeartNessuna valutazione finora

- Vision Institute of Accountancy: Financial ManagementDocumento13 pagineVision Institute of Accountancy: Financial ManagementtitrasableNessuna valutazione finora

- FM - Chapter 15Documento8 pagineFM - Chapter 15Rahul ShrivastavaNessuna valutazione finora

- Capital Structure TheoriesDocumento14 pagineCapital Structure TheoriesbuddingbachelorNessuna valutazione finora

- Chapter 27 BBDocumento23 pagineChapter 27 BBTaVuKieuNhiNessuna valutazione finora

- Chap 6 BBDocumento66 pagineChap 6 BBTaVuKieuNhiNessuna valutazione finora

- Market Efficiency BBDocumento11 pagineMarket Efficiency BBTaVuKieuNhiNessuna valutazione finora

- Chap 11 (PT 1) BBDocumento43 pagineChap 11 (PT 1) BBTaVuKieuNhiNessuna valutazione finora

- Chapter 24 BBDocumento25 pagineChapter 24 BBTaVuKieuNhiNessuna valutazione finora

- Chap 9 BBDocumento69 pagineChap 9 BBTaVuKieuNhiNessuna valutazione finora

- Chapter 23BBDocumento27 pagineChapter 23BBTaVuKieuNhi100% (1)

- Estimating The Cost of CapitalDocumento50 pagineEstimating The Cost of CapitalTaVuKieuNhiNessuna valutazione finora

- Capital Markets and The Pricing of Risk: Chapter 10 (Part I)Documento43 pagineCapital Markets and The Pricing of Risk: Chapter 10 (Part I)TaVuKieuNhiNessuna valutazione finora

- Chapter 17 BBDocumento48 pagineChapter 17 BBTaVuKieuNhiNessuna valutazione finora

- Chap 11 BB (PT 2 New)Documento59 pagineChap 11 BB (PT 2 New)TaVuKieuNhiNessuna valutazione finora

- Capital Markets and The Pricing of Risk: Chapter 10 (Part 2)Documento66 pagineCapital Markets and The Pricing of Risk: Chapter 10 (Part 2)TaVuKieuNhiNessuna valutazione finora

- Financial Management: Chapter 1 The CorporationDocumento38 pagineFinancial Management: Chapter 1 The CorporationTaVuKieuNhiNessuna valutazione finora

- Introduction To APA Style 6th Ed 2010Documento32 pagineIntroduction To APA Style 6th Ed 2010Wided SassiNessuna valutazione finora

- Formula SheetDocumento3 pagineFormula SheetTaVuKieuNhiNessuna valutazione finora

- Tutorial 1Documento2 pagineTutorial 1TaVuKieuNhi100% (1)

- Chapter 9: Stocks ValuationDocumento35 pagineChapter 9: Stocks ValuationTaVuKieuNhiNessuna valutazione finora

- Introduction To APA Style 6th Ed 2010Documento32 pagineIntroduction To APA Style 6th Ed 2010Wided SassiNessuna valutazione finora

- Leaders Eat LastDocumento6 pagineLeaders Eat LastTaVuKieuNhi25% (4)

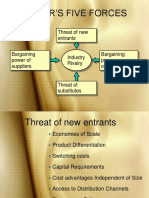

- Porter's Five ForcesDocumento9 paginePorter's Five ForcesTaVuKieuNhiNessuna valutazione finora

- Malaysian Judicial Structure ExplainedDocumento21 pagineMalaysian Judicial Structure ExplainedIz'aan AzalanNessuna valutazione finora

- Econometrics TintnerDocumento17 pagineEconometrics TintnerAlexandreNessuna valutazione finora

- National Income Models with Government and Net ExportsDocumento13 pagineNational Income Models with Government and Net ExportsKratika PandeyNessuna valutazione finora

- Instructors' Manual: Janat Shah Indian Institute of Management BangaloreDocumento9 pagineInstructors' Manual: Janat Shah Indian Institute of Management BangaloregauravNessuna valutazione finora

- India's Reluctant Urbanization - Thinking Beyond-Palgrave Macmillan UK (2015)Documento267 pagineIndia's Reluctant Urbanization - Thinking Beyond-Palgrave Macmillan UK (2015)SuryakantDakshNessuna valutazione finora

- Measuring Price and Quantity ChangesDocumento30 pagineMeasuring Price and Quantity ChangesAfwan AhmedNessuna valutazione finora

- Quiz Gen Math AnnuitiesDocumento1 paginaQuiz Gen Math AnnuitiesJaymark B. UgayNessuna valutazione finora

- International Monetary System PDFDocumento27 pagineInternational Monetary System PDFSuntheng KhieuNessuna valutazione finora

- Business Buying BehaviorDocumento27 pagineBusiness Buying Behaviorkashaf noorNessuna valutazione finora

- ANALYZING FINANCIAL REPORTSDocumento22 pagineANALYZING FINANCIAL REPORTSTia Permata SariNessuna valutazione finora

- BECC-108 2021-22 EnglishDocumento5 pagineBECC-108 2021-22 EnglishSoumya Prasad NayakNessuna valutazione finora

- Exploring the link between opportunity cost and basic economic questionsDocumento3 pagineExploring the link between opportunity cost and basic economic questionsneedmore tendai mararike100% (1)

- CH 07 Tool Kit - Brigham3CeDocumento17 pagineCH 07 Tool Kit - Brigham3CeChad OngNessuna valutazione finora

- Explain Entrepreneurship and Discuss Its ImportanceDocumento3 pagineExplain Entrepreneurship and Discuss Its Importancesn nNessuna valutazione finora

- Full Download Test Bank For Macroeconomics 15th Canadian Edition Christopher T S Ragan PDF Full ChapterDocumento36 pagineFull Download Test Bank For Macroeconomics 15th Canadian Edition Christopher T S Ragan PDF Full Chaptergenevafigueroag9ec100% (19)

- ECON 311 Review Questions For Exam 1/4Documento2 pagineECON 311 Review Questions For Exam 1/4Pierre RodriguezNessuna valutazione finora

- KAIZENDocumento3 pagineKAIZENAmulioto Elijah MuchelleNessuna valutazione finora

- 1.the Advantages and Disadvantages of StatisticsDocumento3 pagine1.the Advantages and Disadvantages of StatisticsMurshid IqbalNessuna valutazione finora

- BEC SYD & DXB Online ScheduleDocumento2 pagineBEC SYD & DXB Online ScheduleMinhChau HoangNessuna valutazione finora

- Impact of Globalization on International Business OperationsDocumento16 pagineImpact of Globalization on International Business OperationsMohit RanaNessuna valutazione finora

- BMO Capital Markets - Treasury Locks, Caps and CollarsDocumento3 pagineBMO Capital Markets - Treasury Locks, Caps and CollarsjgravisNessuna valutazione finora

- Commonly Used Multiples in IndustryDocumento24 pagineCommonly Used Multiples in IndustryRishabh GuptaNessuna valutazione finora