Potrebbero piacerti anche

- Business Economics: Business Strategy & Competitive AdvantageDa EverandBusiness Economics: Business Strategy & Competitive AdvantageNessuna valutazione finora

- Fundamentals of Business Economics Study Resource: CIMA Study ResourcesDa EverandFundamentals of Business Economics Study Resource: CIMA Study ResourcesNessuna valutazione finora

- Inflation AccountingDocumento2 pagineInflation AccountingmehulNessuna valutazione finora

- MBA - AFM - Inflation AccountingDocumento20 pagineMBA - AFM - Inflation AccountingVijayaraj JeyabalanNessuna valutazione finora

- Inflation AccountingDocumento7 pagineInflation AccountingDisha DesaiNessuna valutazione finora

- IAS 29 - NotesDocumento29 pagineIAS 29 - NotesJyNessuna valutazione finora

- Inflation AccountingDocumento4 pagineInflation AccountinganjalikapoorNessuna valutazione finora

- ACCOUNTING: Inflation AccountingDocumento34 pagineACCOUNTING: Inflation Accountingmehul100% (2)

- Inflation Accounting: A Presentation by - ITM XMBA - 33 Dinesh M Manghani Sharon RodriguesDocumento15 pagineInflation Accounting: A Presentation by - ITM XMBA - 33 Dinesh M Manghani Sharon RodriguesDinesh Manghani100% (1)

- C C C CC CCCC CCCCCCCC C C C C C CC CCCCC CCC CC CCC CCC C C C C C CC C C C CC C C C ! C C C C ! C CDocumento4 pagineC C C CC CCCC CCCCCCCC C C C C C CC CCCCC CCC CC CCC CCC C C C C C CC C C C CC C C C ! C C C C ! C CHemanshu MehtaNessuna valutazione finora

- (Sesi 8) (Jurnal) - Accounting For Changing Prices - Will A Lasting Solution Be FoundDocumento7 pagine(Sesi 8) (Jurnal) - Accounting For Changing Prices - Will A Lasting Solution Be Foundmarrifa angelicaNessuna valutazione finora

- 2020 Price Level and Inflation AccountingDocumento2 pagine2020 Price Level and Inflation AccountingKesa MetsiNessuna valutazione finora

- Hra Unit 4Documento19 pagineHra Unit 4World is GoldNessuna valutazione finora

- Inflation AccountingDocumento4 pagineInflation AccountingAnand SalotNessuna valutazione finora

- Application of Inflation AccountingDocumento21 pagineApplication of Inflation AccountingRajesh WariseNessuna valutazione finora

- Impact of Inflation On The Financial StatementsDocumento22 pagineImpact of Inflation On The Financial StatementsabbyplexxNessuna valutazione finora

- Inflation and Monetary PolicyDocumento32 pagineInflation and Monetary PolicyHads LunaNessuna valutazione finora

- Accounting For Price Level ChangesDocumento8 pagineAccounting For Price Level ChangesSonal RathhiNessuna valutazione finora

- On A Study On Inflation AccountingDocumento13 pagineOn A Study On Inflation AccountingomNessuna valutazione finora

- Business Environment Unit 5Documento27 pagineBusiness Environment Unit 5Kainos GreyNessuna valutazione finora

- Inflation AccountingDocumento8 pagineInflation AccountingbhargavNessuna valutazione finora

- Money and Inf MakomboreroDocumento16 pagineMoney and Inf Makomborerotaona madanhireNessuna valutazione finora

- Macro Lecture 4 PDFDocumento40 pagineMacro Lecture 4 PDFpulkit guptaNessuna valutazione finora

- Business CycleDocumento4 pagineBusiness Cycleatharva1760Nessuna valutazione finora

- Inflation AccountingDocumento10 pagineInflation AccountingKunal ModiNessuna valutazione finora

- Inflation Bba20Documento24 pagineInflation Bba20ssd200123Nessuna valutazione finora

- Forensic AccountingDocumento24 pagineForensic AccountingtemedebereNessuna valutazione finora

- Business Cycles: The TheoryDocumento39 pagineBusiness Cycles: The TheorySagar IndranNessuna valutazione finora

- Chapter 4 - Inflation and UnemploymentDocumento18 pagineChapter 4 - Inflation and UnemploymentFirdaus IsmailNessuna valutazione finora

- Long Term Fiscal PolicyDocumento16 pagineLong Term Fiscal PolicyWynne Moses FernandesNessuna valutazione finora

- Inflation AccountingDocumento13 pagineInflation AccountingtrinabhagatNessuna valutazione finora

- IPSAS 10 PresentationDocumento31 pagineIPSAS 10 PresentationTiya AmuNessuna valutazione finora

- MECO Lecture3Documento17 pagineMECO Lecture3saif ur rehmanNessuna valutazione finora

- Lecture - Accounting Concepts - Week 5Documento33 pagineLecture - Accounting Concepts - Week 5presleyramoala81Nessuna valutazione finora

- Notes - Chapter 3Documento4 pagineNotes - Chapter 3Walaa Al-BayaaNessuna valutazione finora

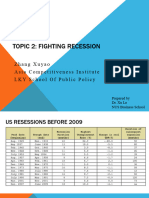

- Week 2 Fighting RecessionDocumento42 pagineWeek 2 Fighting Recessiondaisyruyu2001Nessuna valutazione finora

- Accounting Theory and Alternative Methods For Asset ValuationDocumento25 pagineAccounting Theory and Alternative Methods For Asset ValuationAkshay RawatNessuna valutazione finora

- Macro Classes 1-3Documento35 pagineMacro Classes 1-3Shajidur RashidNessuna valutazione finora

- Types, Causes and Measures To Control InflationDocumento18 pagineTypes, Causes and Measures To Control InflationJagadeesh PutturuNessuna valutazione finora

- Current at The End of The Reporting Period. Comparative Figures For Prior Period(s) Shall Also Be RestatedDocumento3 pagineCurrent at The End of The Reporting Period. Comparative Figures For Prior Period(s) Shall Also Be RestatedJustine VeralloNessuna valutazione finora

- Engineering Economics Lect 4.Documento21 pagineEngineering Economics Lect 4.Furqan ChaudhryNessuna valutazione finora

- Macroeconomics1:: Inflation: Its Causes and Costs (Chapter 30)Documento32 pagineMacroeconomics1:: Inflation: Its Causes and Costs (Chapter 30)Donghun ShinNessuna valutazione finora

- Lecture 15 InflationDocumento13 pagineLecture 15 InflationDevyansh GuptaNessuna valutazione finora

- U5 - Inflation, Business Cycle & Profit TheoriesDocumento11 pagineU5 - Inflation, Business Cycle & Profit Theoriessinhapalak1002Nessuna valutazione finora

- Inflation: Definitions Inflation: Definitions: The Penguin Dictionary of EconomicsDocumento9 pagineInflation: Definitions Inflation: Definitions: The Penguin Dictionary of EconomicsSakshi AroraNessuna valutazione finora

- CE 309 FINANCIAL STATEMENT ANALYSIS Lecture Sept 2013Documento98 pagineCE 309 FINANCIAL STATEMENT ANALYSIS Lecture Sept 2013kundayi shavaNessuna valutazione finora

- Money Growth and InflationDocumento22 pagineMoney Growth and Inflationyurai.kazeNessuna valutazione finora

- 12EPP Chapter 13Documento108 pagine12EPP Chapter 13Mr RamNessuna valutazione finora

- Capitulo 19 en Ingles Libro CelesteDocumento57 pagineCapitulo 19 en Ingles Libro CelesteGinneth Jiménez MadrigalNessuna valutazione finora

- ECO - Chaps - 11-18Documento38 pagineECO - Chaps - 11-18Tawhid QurisheNessuna valutazione finora

- Managerial EconomicsDocumento41 pagineManagerial EconomicsKrishna Chandran PallippuramNessuna valutazione finora

- L 7 8 EconDocumento7 pagineL 7 8 EconAngela Ericka CabanesNessuna valutazione finora

- MECO121 UM S2024 Session14Documento35 pagineMECO121 UM S2024 Session14rizwanf026Nessuna valutazione finora

- CORPORATE ACCOUNTING IA2-pdf 2Documento12 pagineCORPORATE ACCOUNTING IA2-pdf 2Surya GowdaNessuna valutazione finora

- Project Investment Evaluation: Chethan S.GowdaDocumento70 pagineProject Investment Evaluation: Chethan S.GowdaTodesa HinkosaNessuna valutazione finora

- Course Title: Accounting For Managers Course: MBA 18102 CR Session: Spring 2020 Unit IV. Inflation Accounting Faculty: Dr. Gousia ShahDocumento14 pagineCourse Title: Accounting For Managers Course: MBA 18102 CR Session: Spring 2020 Unit IV. Inflation Accounting Faculty: Dr. Gousia ShahLeo SaimNessuna valutazione finora

- Lesson Week 7 ADAS .PPTX - My NotesDocumento49 pagineLesson Week 7 ADAS .PPTX - My NotesMartin van der VlistNessuna valutazione finora

- InflationDocumento25 pagineInflationsyedrahman88Nessuna valutazione finora

- Price Level Accounting by Rekha - 5212Documento30 paginePrice Level Accounting by Rekha - 5212Khesari Lal YadavNessuna valutazione finora

- Inflation-Conscious Investments: Avoid the most common investment pitfallsDa EverandInflation-Conscious Investments: Avoid the most common investment pitfallsNessuna valutazione finora

- Union Test Prep Nclex Study GuideDocumento115 pagineUnion Test Prep Nclex Study GuideBradburn Nursing100% (2)

- Iaea Tecdoc 1092Documento287 pagineIaea Tecdoc 1092Andres AracenaNessuna valutazione finora

- Guidelines For Prescription Drug Marketing in India-OPPIDocumento23 pagineGuidelines For Prescription Drug Marketing in India-OPPINeelesh Bhandari100% (2)

- Electronic Spin Inversion: A Danger To Your HealthDocumento4 pagineElectronic Spin Inversion: A Danger To Your Healthambertje12Nessuna valutazione finora

- Mozal Finance EXCEL Group 15dec2013Documento15 pagineMozal Finance EXCEL Group 15dec2013Abhijit TailangNessuna valutazione finora

- Predator U7135 ManualDocumento36 paginePredator U7135 Manualr17g100% (1)

- Faa Data On B 777 PDFDocumento104 pagineFaa Data On B 777 PDFGurudutt PaiNessuna valutazione finora

- ENT 300 Individual Assessment-Personal Entrepreneurial CompetenciesDocumento8 pagineENT 300 Individual Assessment-Personal Entrepreneurial CompetenciesAbu Ammar Al-hakimNessuna valutazione finora

- Switching Simulation in GNS3 - GNS3Documento3 pagineSwitching Simulation in GNS3 - GNS3Jerry Fourier KemeNessuna valutazione finora

- Report FinalDocumento48 pagineReport FinalSantosh ChaudharyNessuna valutazione finora

- Math 9 Quiz 4Documento3 pagineMath 9 Quiz 4Lin SisombounNessuna valutazione finora

- Please Refer Tender Document and Annexures For More DetailsDocumento1 paginaPlease Refer Tender Document and Annexures For More DetailsNAYANMANI NAMASUDRANessuna valutazione finora

- 2-1. Drifting & Tunneling Drilling Tools PDFDocumento9 pagine2-1. Drifting & Tunneling Drilling Tools PDFSubhash KediaNessuna valutazione finora

- CLG418 (Dcec) PM 201409022-EnDocumento1.143 pagineCLG418 (Dcec) PM 201409022-EnMauricio WijayaNessuna valutazione finora

- Wwii TictactoeDocumento2 pagineWwii Tictactoeapi-557780348Nessuna valutazione finora

- 19c Upgrade Oracle Database Manually From 12C To 19CDocumento26 pagine19c Upgrade Oracle Database Manually From 12C To 19Cjanmarkowski23Nessuna valutazione finora

- Maritime Academy of Asia and The Pacific-Kamaya Point Department of AcademicsDocumento7 pagineMaritime Academy of Asia and The Pacific-Kamaya Point Department of Academicsaki sintaNessuna valutazione finora

- Recruitment SelectionDocumento11 pagineRecruitment SelectionMOHAMMED KHAYYUMNessuna valutazione finora

- Virtual Assets Act, 2022Documento18 pagineVirtual Assets Act, 2022Rapulu UdohNessuna valutazione finora

- Bcci ScandalDocumento6 pagineBcci ScandalNausaf AhmedNessuna valutazione finora

- Measuring Temperature - Platinum Resistance ThermometersDocumento3 pagineMeasuring Temperature - Platinum Resistance Thermometersdark*nightNessuna valutazione finora

- Cam 18 Test 3 ListeningDocumento6 pagineCam 18 Test 3 ListeningKhắc Trung NguyễnNessuna valutazione finora

- Open Source NetworkingDocumento226 pagineOpen Source NetworkingyemenlinuxNessuna valutazione finora

- Poetry UnitDocumento212 paginePoetry Unittrovatore48100% (2)

- Draft JV Agreement (La Mesa Gardens Condominiums - Amparo Property)Documento13 pagineDraft JV Agreement (La Mesa Gardens Condominiums - Amparo Property)Patrick PenachosNessuna valutazione finora

- Notes On Antibodies PropertiesDocumento3 pagineNotes On Antibodies PropertiesBidur Acharya100% (1)

- 52 - JB CHP Trigen - V01Documento33 pagine52 - JB CHP Trigen - V01July E. Maldonado M.Nessuna valutazione finora

- Battery Guide - 2021Documento27 pagineBattery Guide - 2021Mario LaurieNessuna valutazione finora

- 5066452Documento53 pagine5066452jlcheefei9258Nessuna valutazione finora

- MME 52106 - Optimization in Matlab - NN ToolboxDocumento14 pagineMME 52106 - Optimization in Matlab - NN ToolboxAdarshNessuna valutazione finora