Potrebbero piacerti anche

- Value Chain Management Capability A Complete Guide - 2020 EditionDa EverandValue Chain Management Capability A Complete Guide - 2020 EditionNessuna valutazione finora

- Report On LPU CAVITE OJTDocumento10 pagineReport On LPU CAVITE OJTChristian Daniel CotonerNessuna valutazione finora

- Social Justice Standards - Unpacking Social JusticeDocumento9 pagineSocial Justice Standards - Unpacking Social JusticeAmLensNewsNessuna valutazione finora

- Social Justice Standards - Unpacking ActionDocumento8 pagineSocial Justice Standards - Unpacking ActionAmLensNewsNessuna valutazione finora

- Module 2 General Functions of CreditDocumento41 pagineModule 2 General Functions of CreditCaroline Grace Enteria MellaNessuna valutazione finora

- LO1 Select and Classify Hand Tools and EquipmentDocumento61 pagineLO1 Select and Classify Hand Tools and EquipmentLilibeth Roldan100% (2)

- The Financial System: Prepared By:-Pandya Kiran Parmar Ranjit Patel Jignesh Bhayani SanjayDocumento18 pagineThe Financial System: Prepared By:-Pandya Kiran Parmar Ranjit Patel Jignesh Bhayani SanjayAbhishek FanseNessuna valutazione finora

- Syllabus MKT 511 Marketing ManagementDocumento2 pagineSyllabus MKT 511 Marketing ManagementprashantNessuna valutazione finora

- Short-Term Financial PlanningDocumento64 pagineShort-Term Financial PlanningSheila Mae LaputNessuna valutazione finora

- Week 3 - Functions of CreditDocumento8 pagineWeek 3 - Functions of CreditJeayel RelatadoNessuna valutazione finora

- Introduction To Operations Management: Mcgraw-Hill/IrwinDocumento43 pagineIntroduction To Operations Management: Mcgraw-Hill/Irwinvasusingla100% (1)

- Cradle Top Learning School Case Study AnalysisDocumento13 pagineCradle Top Learning School Case Study AnalysisMarjorie Mae Cruzat0% (1)

- Qualitiesofahighperformance Finance Executive:: An Aggregation of SkillsDocumento9 pagineQualitiesofahighperformance Finance Executive:: An Aggregation of Skillsvinni_30Nessuna valutazione finora

- Code of EthicsDocumento32 pagineCode of Ethicsאנג' ליקהNessuna valutazione finora

- CH01 - Introduction To Operations Management Rev.01Documento44 pagineCH01 - Introduction To Operations Management Rev.01Izzaty Riang RiaNessuna valutazione finora

- POM SyllabusDocumento2 paginePOM SyllabusMehul JainNessuna valutazione finora

- POM 102 SyllabusDocumento8 paginePOM 102 SyllabusmarkangeloarceoNessuna valutazione finora

- What Is An Entrepreneur?: - Are Individuals Acting Independently or As Part of An OrganizationDocumento40 pagineWhat Is An Entrepreneur?: - Are Individuals Acting Independently or As Part of An OrganizationDipika ShahNessuna valutazione finora

- Operations Management - Final ExamDocumento3 pagineOperations Management - Final ExamZain khan100% (1)

- Chapter 2 Quality and Global CompetitivenessDocumento13 pagineChapter 2 Quality and Global CompetitivenessZainab GhaddarNessuna valutazione finora

- Recording TransactionDocumento8 pagineRecording TransactionIan BelmonteNessuna valutazione finora

- Report Planning and ControllershipDocumento23 pagineReport Planning and ControllershipANDELYN100% (1)

- Natural Remedies: Causes of Typhoid FeverDocumento3 pagineNatural Remedies: Causes of Typhoid FeversakuarNessuna valutazione finora

- Basic Accounting For BSBA: Chapter 1Documento9 pagineBasic Accounting For BSBA: Chapter 1Cyro Kam SaragponNessuna valutazione finora

- Finaaaaaaal FeasibDocumento53 pagineFinaaaaaaal FeasibCharles TanNessuna valutazione finora

- Operations Management A Research OverviewDocumento65 pagineOperations Management A Research OverviewNguyễn Trần Hoàng100% (1)

- Cadbury EthicsDocumento2 pagineCadbury Ethicsapi-505775092Nessuna valutazione finora

- Financial Accounting PAA198 Student ManualDocumento170 pagineFinancial Accounting PAA198 Student Manualthexplorer008100% (1)

- Chapter 1Documento11 pagineChapter 1Areef Mahmood IqbalNessuna valutazione finora

- Frichicks Swot and Case StudyDocumento6 pagineFrichicks Swot and Case StudyNaoman ChNessuna valutazione finora

- Chapter 1 Principle of Marketing SlidesDocumento36 pagineChapter 1 Principle of Marketing SlidesMirza JunaidNessuna valutazione finora

- Business ResearchDocumento15 pagineBusiness ResearchCunanan, Malakhai JeuNessuna valutazione finora

- Format For ProposalsDocumento5 pagineFormat For ProposalssalllllNessuna valutazione finora

- Activity Guide and Evaluation Rubric - Unit 2 - Phase 3 - Characterize The Logistics Network of A Company Using A Reference Model PDFDocumento9 pagineActivity Guide and Evaluation Rubric - Unit 2 - Phase 3 - Characterize The Logistics Network of A Company Using A Reference Model PDFMary CaicedoNessuna valutazione finora

- The Great Wave of KanagawaDocumento1 paginaThe Great Wave of KanagawaAlman MacasindilNessuna valutazione finora

- Developing A Business PlanDocumento28 pagineDeveloping A Business Plan11-CG14 Jao, Kathleen Maye E.Nessuna valutazione finora

- Financing Feasibility Analysis - PresentationDocumento42 pagineFinancing Feasibility Analysis - PresentationabulyaleeNessuna valutazione finora

- University of Khartoum Faculty of Engineering MEM Total Quality Management and Continuous Improvement LEC 4,5 (TQM)Documento33 pagineUniversity of Khartoum Faculty of Engineering MEM Total Quality Management and Continuous Improvement LEC 4,5 (TQM)Aryan Khairmem KhanNessuna valutazione finora

- Principle Marketin-1Documento102 paginePrinciple Marketin-1bikilahussen100% (1)

- Customer Relation SyllabusDocumento14 pagineCustomer Relation SyllabusYuuki Touya CaloniaNessuna valutazione finora

- QualityDocumento14 pagineQualityEzwan RazmanNessuna valutazione finora

- Unesco TvetDocumento141 pagineUnesco TvetSeli adalah Saya100% (1)

- Water Is A Basic Needs of Individuals It Is Very Essential To Our Health and Our LivesDocumento16 pagineWater Is A Basic Needs of Individuals It Is Very Essential To Our Health and Our Livesnimfa cielo toribioNessuna valutazione finora

- Chapter 2Documento31 pagineChapter 2Roseanne Yumang100% (1)

- Andragogy and PedagogyDocumento3 pagineAndragogy and PedagogyaldyerNessuna valutazione finora

- Strategy ManagementDocumento25 pagineStrategy ManagementAbdul Mateen100% (1)

- Market FeasibilityDocumento73 pagineMarket FeasibilityNiloy SarkarNessuna valutazione finora

- Functional Level Strategy Hill and JonesDocumento34 pagineFunctional Level Strategy Hill and JonesAmi KallalNessuna valutazione finora

- Lovelock PPT Chapter 05Documento27 pagineLovelock PPT Chapter 05Nidhi Gaba Sachdeva100% (1)

- Let The Market Know You BetterDocumento20 pagineLet The Market Know You BetterRutchelNessuna valutazione finora

- 2nd Reaction Paper (Renato L. Egang, JR.)Documento4 pagine2nd Reaction Paper (Renato L. Egang, JR.)Renato Egang JrNessuna valutazione finora

- Purchasing and Payment Policy and Procedures: Responsible University OfficialsDocumento31 paginePurchasing and Payment Policy and Procedures: Responsible University Officialsnitika sehrawatNessuna valutazione finora

- The Business Plan: Michael Karl M. Barnuevo, MBADocumento14 pagineThe Business Plan: Michael Karl M. Barnuevo, MBAWilnerNessuna valutazione finora

- Stevenson 13e Chapter 1Documento40 pagineStevenson 13e Chapter 1NABO IRISHA DIANNENessuna valutazione finora

- Week 3 - Ethics in EntrepreneurshipDocumento5 pagineWeek 3 - Ethics in EntrepreneurshipFon XingNessuna valutazione finora

- Jit Key ElementDocumento35 pagineJit Key ElementshfqshaikhNessuna valutazione finora

- The U.S Postal Service Case Study Q1Documento2 pagineThe U.S Postal Service Case Study Q1NagarajanRK100% (1)

- Advance Accounting Chapter 8Documento52 pagineAdvance Accounting Chapter 8febrythiodorNessuna valutazione finora

- Chapter One: Mcgraw-Hill/IrwinDocumento17 pagineChapter One: Mcgraw-Hill/Irwintyg1992Nessuna valutazione finora

- AccoutingDocumento22 pagineAccoutingmeisi anastasiaNessuna valutazione finora

- Syllabus BlawDocumento11 pagineSyllabus BlawJuan Andres MarquezNessuna valutazione finora

- SyllabusDocumento10 pagineSyllabusJuan Andres MarquezNessuna valutazione finora

- CH.7 Plant Assets, Natural Resources, & IntangiblesDocumento98 pagineCH.7 Plant Assets, Natural Resources, & IntangiblesJuan Andres MarquezNessuna valutazione finora

- Chapter 1: What Is A Business?: Basic Rights in A Private Enterprise SystemDocumento2 pagineChapter 1: What Is A Business?: Basic Rights in A Private Enterprise SystemJuan Andres MarquezNessuna valutazione finora

- Chapter 6: Entrepreneurship: Make Their Business GrowDocumento1 paginaChapter 6: Entrepreneurship: Make Their Business GrowJuan Andres MarquezNessuna valutazione finora

- FIRST EXAM, Fall 2014 MKT 3013.001, IBC Principles of Marketing Chapters 1, 2, 9, 10 & 14 InstructionsDocumento12 pagineFIRST EXAM, Fall 2014 MKT 3013.001, IBC Principles of Marketing Chapters 1, 2, 9, 10 & 14 InstructionsJuan Andres MarquezNessuna valutazione finora

- Finals - Inventories Exercises WithoutDocumento10 pagineFinals - Inventories Exercises WithoutA.B AmpuanNessuna valutazione finora

- jl-18 Bmt1018 TH Sjt626 Vl2017181002984 Reference Material I Exim 04bDocumento15 paginejl-18 Bmt1018 TH Sjt626 Vl2017181002984 Reference Material I Exim 04bPulkit JainNessuna valutazione finora

- Discuss The Four Categories of Trade Term Under The Incoterm 2010Documento8 pagineDiscuss The Four Categories of Trade Term Under The Incoterm 2010Farhana ShahiraNessuna valutazione finora

- Intermediate Accounting 1 Inventories - AssignmentDocumento3 pagineIntermediate Accounting 1 Inventories - AssignmentGabriel Adrian Obungen0% (1)

- Fabm1 Lesson 2Documento21 pagineFabm1 Lesson 2JoshuaNessuna valutazione finora

- 5-3-Buyer and Seller EntriesDocumento3 pagine5-3-Buyer and Seller EntriesRaymond BarbosaNessuna valutazione finora

- Fundamentals of Accountancy, Business and Management 1 Accounting Cycle of A Merchandising BusinessDocumento15 pagineFundamentals of Accountancy, Business and Management 1 Accounting Cycle of A Merchandising BusinessVeniceNessuna valutazione finora

- Auditing InventoriesDocumento8 pagineAuditing InventoriesSabel FordNessuna valutazione finora

- Marine Underwriting & ClausesDocumento74 pagineMarine Underwriting & ClausessemereNessuna valutazione finora

- Special Areas in Accounting 1. Inventory 2. Receivables 3. Fixed AssetsDocumento17 pagineSpecial Areas in Accounting 1. Inventory 2. Receivables 3. Fixed AssetsLivin VargheseNessuna valutazione finora

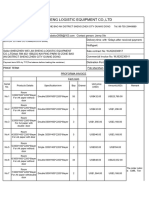

- Shenzhen Wei Jia Sheng Logistic Equipment Co.,Ltd: Payment Term:50% by T/T (The Balance Before Loading The Container)Documento50 pagineShenzhen Wei Jia Sheng Logistic Equipment Co.,Ltd: Payment Term:50% by T/T (The Balance Before Loading The Container)teffoarmand133Nessuna valutazione finora

- Supplemental Sheet: More Than 3,800Kcal/Kg Less Than 3,600 Kcal/Kg Above 4,200Kcal/Kg Below 4,000 Kcal/KgDocumento4 pagineSupplemental Sheet: More Than 3,800Kcal/Kg Less Than 3,600 Kcal/Kg Above 4,200Kcal/Kg Below 4,000 Kcal/KgJody SubiyantoroNessuna valutazione finora

- Payment and Other TermsDocumento11 paginePayment and Other TermsNguyệtt HươnggNessuna valutazione finora

- Practice Homework CH 5 FA21Documento5 paginePractice Homework CH 5 FA21Thomas TermoteNessuna valutazione finora

- EXPORT PROJECT Pre ShipmentDocumento14 pagineEXPORT PROJECT Pre ShipmentMeena SinghNessuna valutazione finora

- K2 Commercial Hardware 2012 Price BookDocumento140 pagineK2 Commercial Hardware 2012 Price BookSecurity Lock DistributorsNessuna valutazione finora

- Japan Motors Trading CoDocumento2 pagineJapan Motors Trading CoBernard Nii Amaa100% (3)

- POPULAR INDUSTRIES LIMITED V EASTERN GARMENT MANUFACTURING SDN BHD, (1989) 3 MLJ 360Documento14 paginePOPULAR INDUSTRIES LIMITED V EASTERN GARMENT MANUFACTURING SDN BHD, (1989) 3 MLJ 360nurulashikin mursid0% (1)

- Ferretería TransmissionConnectorsFull PDFDocumento296 pagineFerretería TransmissionConnectorsFull PDFGabriela VeronelliNessuna valutazione finora

- Tender For Import of Low Ash Metallurgical (Lam) Coke: Email: NKM@MMTC - Nic.inDocumento13 pagineTender For Import of Low Ash Metallurgical (Lam) Coke: Email: NKM@MMTC - Nic.inFouad OuazzaniNessuna valutazione finora

- Glossary Logistics and Supply Chain ManagementDocumento34 pagineGlossary Logistics and Supply Chain ManagementJaime Andrés Cruz ChalacanNessuna valutazione finora

- Biovail Case Study Analysis and SolutionDocumento3 pagineBiovail Case Study Analysis and SolutionHervino WinandaNessuna valutazione finora

- Obligations of The VendorDocumento37 pagineObligations of The VendorElsNessuna valutazione finora

- Saginaw Enclosures Catalog 12Documento345 pagineSaginaw Enclosures Catalog 12QuantumAutomationNessuna valutazione finora

- Mannual 2004Documento213 pagineMannual 2004RajaVikrantNessuna valutazione finora

- SS 2 SlidesDocumento31 pagineSS 2 SlidesDart BaneNessuna valutazione finora

- On December 31, 20x1, ABC Has Total Expenses of P1,000,000 Before Possible Adjustment For The FollowingDocumento12 pagineOn December 31, 20x1, ABC Has Total Expenses of P1,000,000 Before Possible Adjustment For The FollowingKim Cristian MaañoNessuna valutazione finora

- RFBT Sales SorianoDocumento14 pagineRFBT Sales SorianoRexie Tan0% (1)

- Nanjing YJ SJSL51 Air-Strand Twin Screw Extruder Pelletizing LineDocumento9 pagineNanjing YJ SJSL51 Air-Strand Twin Screw Extruder Pelletizing LineOSCAR CORREANessuna valutazione finora

- CH 05Documento77 pagineCH 05Minh ThưNessuna valutazione finora