Potrebbero piacerti anche

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- PWC Aptitude Test Past Questions and Solutions-1-1Documento98 paginePWC Aptitude Test Past Questions and Solutions-1-1adde67% (9)

- Vault Guide To Investment ManagementDocumento126 pagineVault Guide To Investment ManagementMarius George Ciubotariu100% (1)

- FRM Currency FutureDocumento48 pagineFRM Currency FutureParvez KhanNessuna valutazione finora

- Forex VolatilityDocumento25 pagineForex VolatilityNoufal AnsariNessuna valutazione finora

- Week10-Elgin F. Hunt, David C. Colander - Social Science - An Introduction To The Study of Society-Routledge (2016) (Dragged)Documento24 pagineWeek10-Elgin F. Hunt, David C. Colander - Social Science - An Introduction To The Study of Society-Routledge (2016) (Dragged)MuhammetNessuna valutazione finora

- Comp-XM Examination GuideDocumento15 pagineComp-XM Examination GuideJacquesMeyer100% (2)

- Leuchtturm Catalog Numismatics 2009 by KibelaDocumento75 pagineLeuchtturm Catalog Numismatics 2009 by KibelaLuka Mitrovic100% (1)

- International Parity Relationship: Topic 4Documento32 pagineInternational Parity Relationship: Topic 4sittmoNessuna valutazione finora

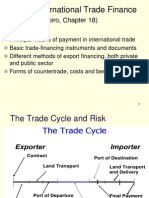

- Topic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)Documento15 pagineTopic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)sittmoNessuna valutazione finora

- AFC3240 Topic 01 S2 2010Documento18 pagineAFC3240 Topic 01 S2 2010sittmoNessuna valutazione finora

- Topic Determination of Exchange Rate: Balance of Payments (BOP)Documento27 pagineTopic Determination of Exchange Rate: Balance of Payments (BOP)sittmoNessuna valutazione finora

- AFC3240 Topic 08 S1 2011Documento24 pagineAFC3240 Topic 08 S1 2011sittmoNessuna valutazione finora

- Section 2 Section 2 Intervention in Markets Intervention in MarketsDocumento18 pagineSection 2 Section 2 Intervention in Markets Intervention in MarketssittmoNessuna valutazione finora

- Sec 04Documento32 pagineSec 04sittmoNessuna valutazione finora

- Solving Inhomogenous Recurrence RelationsDocumento3 pagineSolving Inhomogenous Recurrence Relationssittmo0% (1)

- Solving Inhomogenous Recurrence Relations 2Documento2 pagineSolving Inhomogenous Recurrence Relations 2sittmoNessuna valutazione finora

- BI SourcesDocumento2 pagineBI SourcesAna JovanovićNessuna valutazione finora

- Finance Pq1Documento33 pagineFinance Pq1pakhok3Nessuna valutazione finora

- Solution: Thomson Greenhouse Questions and SolutionsDocumento5 pagineSolution: Thomson Greenhouse Questions and SolutionsMark Jason AguilarNessuna valutazione finora

- Newsday's List Nassau County Top WagesDocumento1 paginaNewsday's List Nassau County Top WagesNewsdayNessuna valutazione finora

- 2013-10 Avolon - Funding The FutureDocumento18 pagine2013-10 Avolon - Funding The Futureawang90Nessuna valutazione finora

- Monetary Law 2002Documento16 pagineMonetary Law 2002gaurav3145Nessuna valutazione finora

- 2015 Annual Report ANZDocumento200 pagine2015 Annual Report ANZgfdsa121Nessuna valutazione finora

- The San Juan International Airport PrivatizationDocumento22 pagineThe San Juan International Airport Privatizationdarwinbondgraham100% (1)

- 2009Q4MDADocumento14 pagine2009Q4MDALuisMendiolaNessuna valutazione finora

- Foreign Exchange ManagementDocumento11 pagineForeign Exchange ManagementVinit MehtaNessuna valutazione finora

- Grech and Others v. MaltaDocumento16 pagineGrech and Others v. MaltaAnaGeoNessuna valutazione finora

- Lecture 6 AcademicDocumento11 pagineLecture 6 AcademicSherkhan IsmanbekovNessuna valutazione finora

- Biographical Note: Address For CorrespondenceDocumento11 pagineBiographical Note: Address For CorrespondenceDebasish BatabyalNessuna valutazione finora

- Euro Bond MarketDocumento14 pagineEuro Bond MarketManjesh Kumar100% (1)

- Cae Software PDFDocumento9 pagineCae Software PDFShyam KrishnanNessuna valutazione finora

- SintexInd Sunidhi 211014Documento7 pagineSintexInd Sunidhi 211014MLastTryNessuna valutazione finora

- International Payment Methods UUZDocumento2 pagineInternational Payment Methods UUZDareje Wabee100% (1)

- Corn Bear ArgumentDocumento11 pagineCorn Bear ArgumentPellucidigmNessuna valutazione finora

- Derivatives and Risk Management Class 1: A. Course IntroductionDocumento2 pagineDerivatives and Risk Management Class 1: A. Course IntroductionasjkdnadjknNessuna valutazione finora

- Appendix To TenderDocumento2 pagineAppendix To TenderAlexandr Trubca100% (1)

- International Financial Management: 12 EditionDocumento47 pagineInternational Financial Management: 12 EditionTania ParvinNessuna valutazione finora

- CH 03Documento17 pagineCH 03Shahab AzizNessuna valutazione finora

- International Finance Assignment 2Documento13 pagineInternational Finance Assignment 2M.A. TanvirNessuna valutazione finora