Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- GT Ref Guide 2012Documento40 pagineGT Ref Guide 2012Cayle Pua100% (3)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The22ImmutableLawsOfBranding BIZDocumento16 pagineThe22ImmutableLawsOfBranding BIZRaja Sufyan MinhasNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Dismantling The American Dream: How Multinational Corporations Undermine American ProsperityDocumento33 pagineDismantling The American Dream: How Multinational Corporations Undermine American ProsperityCharlene KronstedtNessuna valutazione finora

- Gold and Silver Club EbookDocumento22 pagineGold and Silver Club Ebookmfaisalidreis100% (1)

- Marketting Plan - Car LeasingDocumento7 pagineMarketting Plan - Car LeasingRavindra DananeNessuna valutazione finora

- Guide To Using Internationa 2Documento321 pagineGuide To Using Internationa 2Friista Aulia LabibaNessuna valutazione finora

- Divisional Performance ManagementDocumento31 pagineDivisional Performance ManagementiishahbazNessuna valutazione finora

- Dolmen Shopping Festival.Documento1 paginaDolmen Shopping Festival.iishahbazNessuna valutazione finora

- Retail QuestionnaireDocumento2 pagineRetail QuestionnaireiishahbazNessuna valutazione finora

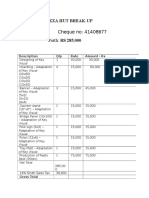

- Cheque No: 41408677 Worth: RS 285,000: Pizza Hut Break-UpDocumento2 pagineCheque No: 41408677 Worth: RS 285,000: Pizza Hut Break-UpiishahbazNessuna valutazione finora

- Cost ManagementDocumento17 pagineCost ManagementiishahbazNessuna valutazione finora

- Standard Costing 2Documento16 pagineStandard Costing 2iishahbazNessuna valutazione finora

- Anti Microbial Activity of Garlic 1Documento6 pagineAnti Microbial Activity of Garlic 1iishahbazNessuna valutazione finora

- Process CostingDocumento7 pagineProcess CostingiishahbazNessuna valutazione finora

- Capital Investment DecisionsDocumento1 paginaCapital Investment DecisionsiishahbazNessuna valutazione finora

- GD SampleDocumento2 pagineGD SampleiishahbazNessuna valutazione finora

- The Budgeting ProcessesDocumento9 pagineThe Budgeting ProcessesiishahbazNessuna valutazione finora

- PLEST Analysis of Global Automotive IndustryDocumento2 paginePLEST Analysis of Global Automotive IndustryiishahbazNessuna valutazione finora

- Photobooth PropsDocumento14 paginePhotobooth PropsiishahbazNessuna valutazione finora

- The Rapid Advancement in Technology Coupled With The Increasing Awareness On Health IssuesDocumento2 pagineThe Rapid Advancement in Technology Coupled With The Increasing Awareness On Health IssuesiishahbazNessuna valutazione finora

- Time Sheet For Teaching AssistantDocumento1 paginaTime Sheet For Teaching AssistantiishahbazNessuna valutazione finora

- Financial Analysis of MitchellsDocumento17 pagineFinancial Analysis of MitchellsiishahbazNessuna valutazione finora

- Principles of Accounting I Assignment # 4: (Type Text)Documento2 paginePrinciples of Accounting I Assignment # 4: (Type Text)iishahbazNessuna valutazione finora

- Equity Options Strategy: Naked PutDocumento2 pagineEquity Options Strategy: Naked PutpkkothariNessuna valutazione finora

- Summer Training Project TopicDocumento24 pagineSummer Training Project Topichoneygoel13Nessuna valutazione finora

- USW1 DDBA 8161 Week03 RivalryStrategyToolDocumento1 paginaUSW1 DDBA 8161 Week03 RivalryStrategyToolfiercelemon1Nessuna valutazione finora

- Titan Case StudyDocumento5 pagineTitan Case StudyKeerthivasa TNessuna valutazione finora

- Microeconomics II Chapter on MonopolyDocumento16 pagineMicroeconomics II Chapter on Monopolyvillaarbaminch0% (1)

- Ch15 SG BLTS 8eDocumento31 pagineCh15 SG BLTS 8eHolli Boyd-White100% (1)

- Hemh108 PDFDocumento20 pagineHemh108 PDFhoneygarg1986Nessuna valutazione finora

- Order Details - Carter'sDocumento4 pagineOrder Details - Carter'sSura SeyidovaNessuna valutazione finora

- Multiple Choice Questions 1 The Short Run Supply Curve of ADocumento2 pagineMultiple Choice Questions 1 The Short Run Supply Curve of Atrilocksp SinghNessuna valutazione finora

- Appendix - 15 (R) University of MadrasDocumento255 pagineAppendix - 15 (R) University of MadrasMonica KshirsagarNessuna valutazione finora

- My Trading StrategyDocumento10 pagineMy Trading StrategyYiunam LeungNessuna valutazione finora

- LP Batch 2 Business MathDocumento22 pagineLP Batch 2 Business MathSEAN ANDREI TORRESNessuna valutazione finora

- Name: E-Mail: Cell Phone Number:: Balance Sheet Initial 1st MonthDocumento3 pagineName: E-Mail: Cell Phone Number:: Balance Sheet Initial 1st MonthEmiliano Mancilla SilvaNessuna valutazione finora

- Consolidated SOFP of Sing and DanceDocumento36 pagineConsolidated SOFP of Sing and DanceVicky Fan67% (3)

- Tetra Pak: Defining Markets and Competitive AdvantageDocumento11 pagineTetra Pak: Defining Markets and Competitive Advantagemazzaw12Nessuna valutazione finora

- Spon's Civil Engineering and Highway Works Price B... - (PART 2 On Costs and Profit)Documento6 pagineSpon's Civil Engineering and Highway Works Price B... - (PART 2 On Costs and Profit)mohamedNessuna valutazione finora

- Gashub - 2018Documento23 pagineGashub - 2018Ricky PrasetyaNessuna valutazione finora

- NFCPAR-Auditing Problems: Description Machinery Others NotesDocumento1 paginaNFCPAR-Auditing Problems: Description Machinery Others NotesSano ManjiroNessuna valutazione finora

- Project On Rural MarketDocumento38 pagineProject On Rural MarketSmita Keluskar100% (1)

- Homework Solution - Week 10 - Relevant Costing - GarrisonDocumento6 pagineHomework Solution - Week 10 - Relevant Costing - GarrisonGloria WongNessuna valutazione finora

- 1 - The Investment SettingDocumento48 pagine1 - The Investment SettingYash Raj SinghNessuna valutazione finora

- Productivity CompressDocumento10 pagineProductivity CompresstayerNessuna valutazione finora

- Graeber Summary Chapter 11Documento5 pagineGraeber Summary Chapter 11api-291732914Nessuna valutazione finora

- MaterialDocumento5 pagineMaterialQuestionscastle FriendNessuna valutazione finora

- NH-24 Tenders - ExtractsDocumento4 pagineNH-24 Tenders - Extractsshravan38Nessuna valutazione finora