Potrebbero piacerti anche

- Quiz # 2Documento28 pagineQuiz # 2Kking Chung100% (1)

- Research Proposal On Corporate GovernanceDocumento12 pagineResearch Proposal On Corporate GovernanceOlabanjo Shefiu Olamiji60% (5)

- Study of NPA in IndiaDocumento43 pagineStudy of NPA in IndiaKartik UdayarNessuna valutazione finora

- Note Receivable Part 2Documento7 pagineNote Receivable Part 2Carlo VillanNessuna valutazione finora

- Ahzizat SummaryDocumento12 pagineAhzizat Summaryolasmart OluwaleNessuna valutazione finora

- Effect of Budgetary Control and Financial Performance ....Documento9 pagineEffect of Budgetary Control and Financial Performance ....Ewnetu TadesseNessuna valutazione finora

- RECAPITALISATIONDocumento9 pagineRECAPITALISATIONEmmanuel MensahNessuna valutazione finora

- The Impact of Financial Restructuring On The Performance of Pakistani Banks: A DEA ApproachDocumento17 pagineThe Impact of Financial Restructuring On The Performance of Pakistani Banks: A DEA ApproachRehan KhalidNessuna valutazione finora

- Cost Efficiency of Ghana'S Banking Industry: A Panel Data AnalysisDocumento19 pagineCost Efficiency of Ghana'S Banking Industry: A Panel Data AnalysisA TUNessuna valutazione finora

- An Investigation Into The Determinants of Cost Efficiency in The Zambian Banking SectorDocumento45 pagineAn Investigation Into The Determinants of Cost Efficiency in The Zambian Banking SectorKemi OlojedeNessuna valutazione finora

- Impact of CG On Banks Performance in Nigeria PDFDocumento4 pagineImpact of CG On Banks Performance in Nigeria PDFRizka HayatiNessuna valutazione finora

- IndustrialandCommercialBankofChina Research PaperDocumento53 pagineIndustrialandCommercialBankofChina Research PaperSYED TANVEERNessuna valutazione finora

- Rating of Indian Commercial Banks: A DEA Approach: Asish Saha, T.S. RavisankarDocumento17 pagineRating of Indian Commercial Banks: A DEA Approach: Asish Saha, T.S. RavisankarSaurabh SuryavanshiNessuna valutazione finora

- Board Structure and Bank Performance in Ghana-With-Cover-Page-V2Documento14 pagineBoard Structure and Bank Performance in Ghana-With-Cover-Page-V2KatyNessuna valutazione finora

- Impact of NonDocumento30 pagineImpact of NonAmardeep SinghNessuna valutazione finora

- Banking Sector ReformsDocumento6 pagineBanking Sector ReformsvkfzrNessuna valutazione finora

- 02 IntroductionDocumento3 pagine02 Introductionmukherjeeprity52Nessuna valutazione finora

- Financial Performance Evaluation of Some Selected Jordanian Commercial BanksDocumento14 pagineFinancial Performance Evaluation of Some Selected Jordanian Commercial BanksAtiaTahiraNessuna valutazione finora

- Recapitalization and Banks Performance ADocumento17 pagineRecapitalization and Banks Performance AGREEN FIELD AGRO HI- TECH SERVICES SANGAMNER.Nessuna valutazione finora

- Banking Sector Reforms in Bangladesh: Measures and Economic OutcomesDocumento25 pagineBanking Sector Reforms in Bangladesh: Measures and Economic OutcomesFakhrul Islam RubelNessuna valutazione finora

- 2022 Heliyon Blankson - Examining The Determinants of Bank Efficiency in Transition - Empirical Evidence From GhanaDocumento11 pagine2022 Heliyon Blankson - Examining The Determinants of Bank Efficiency in Transition - Empirical Evidence From GhanaWahyutri IndonesiaNessuna valutazione finora

- Banking RegulationDocumento16 pagineBanking RegulationPst W C PetersNessuna valutazione finora

- Camelmodel ProjectDocumento26 pagineCamelmodel ProjectDEVARAJ KGNessuna valutazione finora

- Chapter One 1.0 1.1 Background of The StudyDocumento17 pagineChapter One 1.0 1.1 Background of The StudyEkoh EnduranceNessuna valutazione finora

- Effects of Bank Specific Attributes On Capital Adequency of Listed Commercial Bank in Nigeria Chapter OneDocumento34 pagineEffects of Bank Specific Attributes On Capital Adequency of Listed Commercial Bank in Nigeria Chapter OneUmar FarouqNessuna valutazione finora

- Corporate Governance Mechanisms and Financial Performance of 3ots22pwlzDocumento16 pagineCorporate Governance Mechanisms and Financial Performance of 3ots22pwlzMohammed HamoudNessuna valutazione finora

- Asset Quality As A Determinant of Commercial Banks Financial Performance in KenyaDocumento12 pagineAsset Quality As A Determinant of Commercial Banks Financial Performance in KenyaAsegid GetachewNessuna valutazione finora

- MFS AssignmentDocumento11 pagineMFS AssignmentDevangi PatelNessuna valutazione finora

- Need For A Strong Efficient Financial SystemDocumento5 pagineNeed For A Strong Efficient Financial SystemSindhuja SridharNessuna valutazione finora

- Banking Sector Reforms 23 Dec 06Documento9 pagineBanking Sector Reforms 23 Dec 06shoaibmbaNessuna valutazione finora

- CAPITALSTRUCTUREOFBANK IN GhanaDocumento14 pagineCAPITALSTRUCTUREOFBANK IN Ghananle brunoNessuna valutazione finora

- The Empirical Analysis of The Impact of Bank Capital Regulations On Operating EfficiencyDocumento11 pagineThe Empirical Analysis of The Impact of Bank Capital Regulations On Operating Efficiencyanon_614457836Nessuna valutazione finora

- Root,+Journal+Manager,+11 IRMM+5927+Mawanza+Okey 20180224 V1Documento7 pagineRoot,+Journal+Manager,+11 IRMM+5927+Mawanza+Okey 20180224 V1Lionel Itai MuzondoNessuna valutazione finora

- Chapter One 1.1 Background of The StudyDocumento6 pagineChapter One 1.1 Background of The StudyChidi EmmanuelNessuna valutazione finora

- Article No 4Documento13 pagineArticle No 4Areeba.SulemanNessuna valutazione finora

- Financial Deregulations and Productivity Change in Pakistan Banking IndustryDocumento7 pagineFinancial Deregulations and Productivity Change in Pakistan Banking IndustrykumardattNessuna valutazione finora

- Analisa Performa BankDocumento16 pagineAnalisa Performa BankLevramNessuna valutazione finora

- Liberalisation 1991Documento5 pagineLiberalisation 1991ROKOV ZHASANessuna valutazione finora

- Project Work 2Documento5 pagineProject Work 2Joshua DadzieNessuna valutazione finora

- Banking Sector Reforms Lesson From PakistanDocumento15 pagineBanking Sector Reforms Lesson From PakistanBasit SattarNessuna valutazione finora

- 14 Chapter 6Documento2 pagine14 Chapter 6Chham Chha Virak VccNessuna valutazione finora

- Efficiency and Productivity Growth in Indian Banking: Working Paper No. 199Documento26 pagineEfficiency and Productivity Growth in Indian Banking: Working Paper No. 199deepakpinksuratNessuna valutazione finora

- Africa Financial Sector ReformsDocumento4 pagineAfrica Financial Sector Reformsfeisal10Nessuna valutazione finora

- Comparative Analysis of The Impact of Mergers Andacquisitions On Financial Efficiency of Banks in NigeriaDocumento7 pagineComparative Analysis of The Impact of Mergers Andacquisitions On Financial Efficiency of Banks in NigeriaArdi GunardiNessuna valutazione finora

- Does Corporate Governance Affect Bank Profitability? Evidence From NigeriaDocumento11 pagineDoes Corporate Governance Affect Bank Profitability? Evidence From Nigeriamanishaamba7547Nessuna valutazione finora

- Y V Reddy: Banking Sector Reforms in India - An OverviewDocumento7 pagineY V Reddy: Banking Sector Reforms in India - An OverviewTanimaa MehraNessuna valutazione finora

- Baba Inna PaperDocumento14 pagineBaba Inna PaperMOHAMMED ABDULMALIKNessuna valutazione finora

- The Performances of Commercial Banks in Post-ConsolidationDocumento12 pagineThe Performances of Commercial Banks in Post-ConsolidationharmedluvNessuna valutazione finora

- Conclusions, Summary and Recommendations: Chapter - 9Documento44 pagineConclusions, Summary and Recommendations: Chapter - 9priyanka_gandhi28Nessuna valutazione finora

- "Using As A Tool For Evaluate Banking Performance": Shawkat Abdul Amir Shamir Dr. Qassim Mohammed Al-BaajDocumento13 pagine"Using As A Tool For Evaluate Banking Performance": Shawkat Abdul Amir Shamir Dr. Qassim Mohammed Al-BaajSaint CutesyNessuna valutazione finora

- Credit Risk ManagementDocumento41 pagineCredit Risk Managementkijiba50% (2)

- Article No 5Documento18 pagineArticle No 5Areeba.SulemanNessuna valutazione finora

- Report Information From Proquest: October 31 2015 22:35Documento17 pagineReport Information From Proquest: October 31 2015 22:35Regie AlbeldaNessuna valutazione finora

- Reforms in The Banking Sector - India - Bank ManagementDocumento16 pagineReforms in The Banking Sector - India - Bank ManagementSanju HNessuna valutazione finora

- Effects of Government Regulations On Banks OperationsDocumento23 pagineEffects of Government Regulations On Banks OperationsGabrielNessuna valutazione finora

- The Banking Sector of Bangladesh: A General Discussion On Ten Years' AchievementsDocumento48 pagineThe Banking Sector of Bangladesh: A General Discussion On Ten Years' AchievementsAntor Khan PathanNessuna valutazione finora

- Bank and Improvement ProcessDocumento9 pagineBank and Improvement ProcessYun Fung YAPNessuna valutazione finora

- A Comparison of Financial Performance in The Banking Sector: Some Evidence From Pakistani Commercial BanksDocumento14 pagineA Comparison of Financial Performance in The Banking Sector: Some Evidence From Pakistani Commercial Banks007mbsNessuna valutazione finora

- ProposalDocumento10 pagineProposalSagar KarkiNessuna valutazione finora

- Determinants of Bank Profits and Its Persistence in Indian Banks: A Study in A Dynamic Panel Data FrameworkDocumento12 pagineDeterminants of Bank Profits and Its Persistence in Indian Banks: A Study in A Dynamic Panel Data FrameworkKatyNessuna valutazione finora

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Da EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Nessuna valutazione finora

- Class 2 Syllabus 2012-2013Documento34 pagineClass 2 Syllabus 2012-2013Dromor Tackie-YaoboiNessuna valutazione finora

- Mion Financials 2018Documento12 pagineMion Financials 2018Dromor Tackie-YaoboiNessuna valutazione finora

- Workbook For NurseryDocumento13 pagineWorkbook For NurseryDromor Tackie-YaoboiNessuna valutazione finora

- Code of Conduct For StudentsDocumento12 pagineCode of Conduct For StudentsDromor Tackie-YaoboiNessuna valutazione finora

- Strategies For Effective Lesson PlanningDocumento6 pagineStrategies For Effective Lesson PlanningDromor Tackie-YaoboiNessuna valutazione finora

- Treasury MGTDocumento15 pagineTreasury MGTDromor Tackie-YaoboiNessuna valutazione finora

- Code of Conduct For StudentsDocumento12 pagineCode of Conduct For StudentsDromor Tackie-YaoboiNessuna valutazione finora

- Teaching Approaches and StrategiesDocumento23 pagineTeaching Approaches and StrategiesDromor Tackie-YaoboiNessuna valutazione finora

- SMU's Semester V Assignment For Finance OptionDocumento101 pagineSMU's Semester V Assignment For Finance OptionDromor Tackie-YaoboiNessuna valutazione finora

- CHAPTER ON1 Final WorkDocumento50 pagineCHAPTER ON1 Final WorkDromor Tackie-YaoboiNessuna valutazione finora

- Chapter One 1: 1. Background of The StudyDocumento29 pagineChapter One 1: 1. Background of The StudyDromor Tackie-YaoboiNessuna valutazione finora

- Marketing 1Documento22 pagineMarketing 1Dromor Tackie-YaoboiNessuna valutazione finora

- CH 1 Development Practice QP 2022-23Documento4 pagineCH 1 Development Practice QP 2022-23ARSHAD JAMILNessuna valutazione finora

- FM Project ConclusionDocumento4 pagineFM Project ConclusionIbn NafeesNessuna valutazione finora

- Ecological Economics ConceptsDocumento51 pagineEcological Economics ConceptsDarryl LemNessuna valutazione finora

- Income and Tax Simplified TablesDocumento3 pagineIncome and Tax Simplified TablesNiñoMaurinNessuna valutazione finora

- Income Statement Problem SolvingDocumento12 pagineIncome Statement Problem SolvingMaryjoy CuyosNessuna valutazione finora

- HBL-Vertical & Horizontal AnlyisDocumento10 pagineHBL-Vertical & Horizontal AnlyismughalsairaNessuna valutazione finora

- 20 Actual Writing Task 1 Questions With Sample AnswersDocumento27 pagine20 Actual Writing Task 1 Questions With Sample AnswersNa NaNessuna valutazione finora

- ICARE Preweek FAR by Sir RainDocumento13 pagineICARE Preweek FAR by Sir Rainjohn paulNessuna valutazione finora

- Quiz - Income Tax For CorporationsDocumento3 pagineQuiz - Income Tax For Corporationskim mindoroNessuna valutazione finora

- Market Sizing ExerciseDocumento11 pagineMarket Sizing ExerciseAjayNessuna valutazione finora

- Jimma Institute of Technology School of Chemical Engineering Project of EnterprneurshipDocumento19 pagineJimma Institute of Technology School of Chemical Engineering Project of Enterprneurshipsirno yonasNessuna valutazione finora

- Chapter 14 Documentary Stamp TaxDocumento3 pagineChapter 14 Documentary Stamp TaxEngel Racraquin BristolNessuna valutazione finora

- GR No. 78133Documento1 paginaGR No. 78133ElleNessuna valutazione finora

- Answers To Practice Test (Acctg 1, Chapters 3,4)Documento2 pagineAnswers To Practice Test (Acctg 1, Chapters 3,4)HassleBustNessuna valutazione finora

- Financial Accounting Libby 7th Edition Solutions ManualDocumento36 pagineFinancial Accounting Libby 7th Edition Solutions Manualwalerfluster9egfh3100% (39)

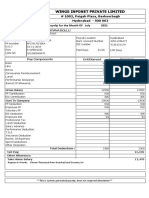

- Wings Infonet Private Limited: # 1002, Paigah Plaza, Basheerbagh Hyderabad - 500 063 2021Documento1 paginaWings Infonet Private Limited: # 1002, Paigah Plaza, Basheerbagh Hyderabad - 500 063 2021Venkatanarayana BolluNessuna valutazione finora

- Vinamilk: Business Analysis Presentation - Assignment 1 SGS-G02-AccountingDocumento49 pagineVinamilk: Business Analysis Presentation - Assignment 1 SGS-G02-AccountingLy NguyễnNessuna valutazione finora

- Financial Reporting in Hyperinflationary Economies: AssetsDocumento4 pagineFinancial Reporting in Hyperinflationary Economies: AssetsKian GaboroNessuna valutazione finora

- Acc 124Documento35 pagineAcc 124Ikang CabreraNessuna valutazione finora

- Exercises - Individual IT - TLDocumento1 paginaExercises - Individual IT - TLClyde SaulNessuna valutazione finora

- TLE-HE 6 - Q2 - Mod1Documento20 pagineTLE-HE 6 - Q2 - Mod1trishajilliene nacisNessuna valutazione finora

- Economics 20th Edition Mcconnell Solutions ManualDocumento15 pagineEconomics 20th Edition Mcconnell Solutions Manuallaurasheppardxntfyejmsr100% (30)

- BNBR - Final Report Billingual December 31 2022 PDFDocumento135 pagineBNBR - Final Report Billingual December 31 2022 PDFVal IntanNessuna valutazione finora

- Calculative Questions - Chapter 10 Measuring A Nations IncomeDocumento13 pagineCalculative Questions - Chapter 10 Measuring A Nations IncomePhuong Vy PhamNessuna valutazione finora

- The Accounting Cycle: Reporting Financial Results: Mcgraw-Hill/IrwinDocumento28 pagineThe Accounting Cycle: Reporting Financial Results: Mcgraw-Hill/Irwinazee inmixNessuna valutazione finora

- Chapter 2. Understanding The Income Statement A. QuestionsDocumento2 pagineChapter 2. Understanding The Income Statement A. QuestionsThị Kim TrầnNessuna valutazione finora

- Budget Tracking Tool - TMOAP Google Sheets Official Version 4.1Documento172 pagineBudget Tracking Tool - TMOAP Google Sheets Official Version 4.1Sarah Mae RomanoNessuna valutazione finora

- Literature Review On Selection Criteria of Store Location Based On Performance MeasuresDocumento16 pagineLiterature Review On Selection Criteria of Store Location Based On Performance MeasuresNIMMANAGANTI RAMAKRISHNANessuna valutazione finora