Potrebbero piacerti anche

- Balance Sheet Analysis of Maruti SuzukiDocumento63 pagineBalance Sheet Analysis of Maruti Suzukikeyur5867% (6)

- Balance SheetDocumento30 pagineBalance SheetBhuvan GuptaNessuna valutazione finora

- Balance Sheet AnalysisDocumento42 pagineBalance Sheet Analysismusadhiq_yavarNessuna valutazione finora

- Segment AnalysisDocumento53 pagineSegment AnalysisamanNessuna valutazione finora

- Ratio Analysis - Tata and M Amp MDocumento38 pagineRatio Analysis - Tata and M Amp MNani BhupalamNessuna valutazione finora

- Comparative Ratio Analysis of Two Companies: Bata & Apex 2011-14Documento21 pagineComparative Ratio Analysis of Two Companies: Bata & Apex 2011-14Arnab Upal100% (2)

- Handout # 1 Solutions (L)Documento10 pagineHandout # 1 Solutions (L)Prabhawati prasadNessuna valutazione finora

- 4.1-Hortizontal/Trends Analysis: Chapter No # 4Documento32 pagine4.1-Hortizontal/Trends Analysis: Chapter No # 4Sadi ShahzadiNessuna valutazione finora

- Balance Sheet AnalysisDocumento18 pagineBalance Sheet Analysisrajat ranjanNessuna valutazione finora

- Types Financial RatiosDocumento8 pagineTypes Financial RatiosRohit Chaudhari100% (1)

- Chapter 7 Notes Question Amp SolutionsDocumento7 pagineChapter 7 Notes Question Amp SolutionsPankhuri SinghalNessuna valutazione finora

- Ratio Analysis: Theory and ProblemsDocumento51 pagineRatio Analysis: Theory and ProblemsAnit Jacob Philip100% (1)

- Bond ImmunisationDocumento29 pagineBond ImmunisationVaidyanathan RavichandranNessuna valutazione finora

- Value Based Management BCG ApproachDocumento14 pagineValue Based Management BCG ApproachAvi AhujaNessuna valutazione finora

- Ratio AnalysisDocumento12 pagineRatio AnalysisSachinNessuna valutazione finora

- Financial Statement Analysis and Valuation (Penman) FA2013Documento5 pagineFinancial Statement Analysis and Valuation (Penman) FA2013Saurabh VashistNessuna valutazione finora

- Advantages of Accounting RatiosDocumento3 pagineAdvantages of Accounting RatiosNeha BatraNessuna valutazione finora

- Modern Pharma Is Considering The Manufacture of A New Drug, Floxin, For Which The FollowingDocumento7 pagineModern Pharma Is Considering The Manufacture of A New Drug, Floxin, For Which The FollowingbansalparthNessuna valutazione finora

- Relative Valuation JaiDocumento29 pagineRelative Valuation JaiGarima SinghNessuna valutazione finora

- SynopsisDocumento7 pagineSynopsisAnchalNessuna valutazione finora

- ICAI Corporate ValuationDocumento47 pagineICAI Corporate Valuationqamaraleem1_25038318Nessuna valutazione finora

- Company AnalysisDocumento11 pagineCompany AnalysisRamesh Chandra DasNessuna valutazione finora

- Continuous Assignments: Ram Kumar KakaniDocumento10 pagineContinuous Assignments: Ram Kumar KakaniKabeer KarnaniNessuna valutazione finora

- Valuing Real Assets in The Presence of Risk: Strategic Financial ManagementDocumento15 pagineValuing Real Assets in The Presence of Risk: Strategic Financial ManagementAnish Mittal100% (1)

- 3 Financial RatiosDocumento29 pagine3 Financial RatiosAB12P1 Sanchez Krisly AngelNessuna valutazione finora

- Accounting Standard IndiaDocumento114 pagineAccounting Standard IndiakprakashmmNessuna valutazione finora

- Receivable Management KanchanDocumento12 pagineReceivable Management KanchanSanchita NaikNessuna valutazione finora

- Financial Analysis TATA STEElDocumento18 pagineFinancial Analysis TATA STEElneha mundraNessuna valutazione finora

- CH 09Documento34 pagineCH 09Azhar SeptariNessuna valutazione finora

- Final Project Format For Profitability Ratio Analysis of Company A, Company B and Company C in Same Industry For FY 20X1 20X2 20X3Documento15 pagineFinal Project Format For Profitability Ratio Analysis of Company A, Company B and Company C in Same Industry For FY 20X1 20X2 20X3janimeetmeNessuna valutazione finora

- Investment Valuation RatiosDocumento18 pagineInvestment Valuation RatiosVicknesan AyapanNessuna valutazione finora

- FM - 1 AssignmentDocumento6 pagineFM - 1 AssignmentBHAVEN ASHOK SINGHNessuna valutazione finora

- Business Valuation PresentationDocumento43 pagineBusiness Valuation PresentationNitin Pal SinghNessuna valutazione finora

- Unit 6 Financial Statements Analysis and InterpretationDocumento58 pagineUnit 6 Financial Statements Analysis and Interpretationdaniel rajkumarNessuna valutazione finora

- Dabur IndiaDocumento37 pagineDabur IndiaBandaru NarendrababuNessuna valutazione finora

- Chapter 11 Valuation Using MultiplesDocumento22 pagineChapter 11 Valuation Using MultiplesUmar MansuriNessuna valutazione finora

- BCG ApproachDocumento2 pagineBCG ApproachAdhityaNessuna valutazione finora

- Financial Ratio Analysis Dec 2013 PDFDocumento13 pagineFinancial Ratio Analysis Dec 2013 PDFHạng VũNessuna valutazione finora

- Capital Budgeting Illustrative NumericalsDocumento6 pagineCapital Budgeting Illustrative NumericalsPriyanka Dargad100% (1)

- Chap 12Documento23 pagineChap 12Maria SyNessuna valutazione finora

- PHT and KooistraDocumento4 paginePHT and KooistraNilesh PrajapatiNessuna valutazione finora

- 03 Financial AnalyticsDocumento11 pagine03 Financial AnalyticsII MBA 2021Nessuna valutazione finora

- CH 10Documento18 pagineCH 10prashantgargindia_93Nessuna valutazione finora

- SFM - Forex - QuestionsDocumento23 pagineSFM - Forex - QuestionsVishal SutarNessuna valutazione finora

- Case QuestionsDocumento5 pagineCase Questionsaditi_sharma_65Nessuna valutazione finora

- Lecture5 6 Ratio Analysis 13Documento39 pagineLecture5 6 Ratio Analysis 13Cristina IonescuNessuna valutazione finora

- Vegetron ExcelDocumento21 pagineVegetron Excelanirudh03467% (3)

- Analysis and Interpretation of Financial StatementsDocumento23 pagineAnalysis and Interpretation of Financial StatementsJohn HolmesNessuna valutazione finora

- A Note On Valuation in Entrepreneurial SettingsDocumento4 pagineA Note On Valuation in Entrepreneurial SettingsUsmanNessuna valutazione finora

- 395 37 Solutions Case Studies 4 Time Value Money Case Solutions Chapter 4 FMDocumento13 pagine395 37 Solutions Case Studies 4 Time Value Money Case Solutions Chapter 4 FMblazeweaver67% (3)

- A PPT On Money MarketDocumento25 pagineA PPT On Money MarketBrinder SinghNessuna valutazione finora

- Cost of CapitalDocumento8 pagineCost of CapitalAreeb BaqaiNessuna valutazione finora

- Financial Ratios and Their InterpretationDocumento10 pagineFinancial Ratios and Their InterpretationPriyanka_Bhans_7838100% (3)

- BR Act, 1949Documento7 pagineBR Act, 1949aki16288Nessuna valutazione finora

- ALM PPT FinalDocumento49 pagineALM PPT FinalNishant SinhaNessuna valutazione finora

- Bfm-Mod - D PDFDocumento18 pagineBfm-Mod - D PDFparul yadavNessuna valutazione finora

- Meaning of A Balance Sheet of A Bank: 2) Liabilities of The Commercial BanksDocumento4 pagineMeaning of A Balance Sheet of A Bank: 2) Liabilities of The Commercial BanksShilpan ShahNessuna valutazione finora

- A Study of Non Performing Assets in Bank of BarodaDocumento68 pagineA Study of Non Performing Assets in Bank of BarodaMohamed Tousif81% (21)

- Chapter 5Documento36 pagineChapter 5Baby KhorNessuna valutazione finora

- Chapter 2Documento127 pagineChapter 2Dung Hoàng Khưu VõNessuna valutazione finora

- Foreign Exchange Operations of Jamuna BankDocumento43 pagineForeign Exchange Operations of Jamuna BankHole StudioNessuna valutazione finora

- JAIIB Paper 4 RBWM Module C Support Services Marketing of Banking Services Products PDFDocumento39 pagineJAIIB Paper 4 RBWM Module C Support Services Marketing of Banking Services Products PDFAssr MurtyNessuna valutazione finora

- 15624702052231UoGssBO9TQOUnD5 PDFDocumento5 pagine15624702052231UoGssBO9TQOUnD5 PDFvenkateshbitraNessuna valutazione finora

- Delhi Co-Operative Housing Finance Corporation LTDDocumento6 pagineDelhi Co-Operative Housing Finance Corporation LTDLalit SharmaNessuna valutazione finora

- 9 Sebi, S M (P #1-C) : Hare Arket IllarDocumento19 pagine9 Sebi, S M (P #1-C) : Hare Arket IllarVCITYNessuna valutazione finora

- A BadulaDocumento4 pagineA Badulanotapernota101Nessuna valutazione finora

- Metrobank FoundationDocumento11 pagineMetrobank FoundationAbigail LeronNessuna valutazione finora

- European Central BankDocumento2 pagineEuropean Central BanknairpranavNessuna valutazione finora

- Accounting Peculiarity of CoopDocumento6 pagineAccounting Peculiarity of CoopRoann AguirreNessuna valutazione finora

- IBPS Po 2012 Exam Question Papers & AnswersDocumento12 pagineIBPS Po 2012 Exam Question Papers & AnswersVenkey Goud100% (2)

- Foreign Currency ValuationDocumento12 pagineForeign Currency ValuationAhmed ElhawaryNessuna valutazione finora

- BRM ProjectDocumento23 pagineBRM Projectrbhatter007Nessuna valutazione finora

- Module - 2 Banking System and Operations: Rajneesh MishraDocumento51 pagineModule - 2 Banking System and Operations: Rajneesh MishramarianmadhurNessuna valutazione finora

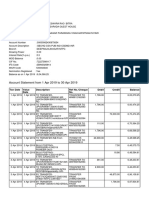

- Bank StatementDocumento1 paginaBank Statementcodex hdNessuna valutazione finora

- POA Section 7 Part 1Documento4 paginePOA Section 7 Part 1kxng ultimateNessuna valutazione finora

- RE Financiers ListDocumento15 pagineRE Financiers ListAhmed Mobashshir SamaniNessuna valutazione finora

- 01Documento2 pagine01ishtee894Nessuna valutazione finora

- Prudential Bank Vs IAC - G.R. No. 74886. December 8, 1992Documento13 paginePrudential Bank Vs IAC - G.R. No. 74886. December 8, 1992Ebbe DyNessuna valutazione finora

- MTech QROR InterviewDocumento3 pagineMTech QROR InterviewMohammadChharchhodawalaNessuna valutazione finora

- Loan Pricing 916Documento22 pagineLoan Pricing 916Gonçalo MadalenoNessuna valutazione finora

- Partnership Resolution SampleDocumento2 paginePartnership Resolution SamplePatrick John Salalila Paguio89% (9)

- Disbursement HandbookDocumento152 pagineDisbursement Handbookasf100% (1)

- Problem 3Documento3 pagineProblem 3Joyce GijsenNessuna valutazione finora

- Arbes Obs enDocumento12 pagineArbes Obs enAndy PhuongNessuna valutazione finora

- NomadGuide CHIANG MAI Guide Book PreviewDocumento33 pagineNomadGuide CHIANG MAI Guide Book PreviewMichael John Hughes100% (1)

- WL WL: Irctcs E Ticketing Service Electronic Reservation Slip (Personal User)Documento1 paginaWL WL: Irctcs E Ticketing Service Electronic Reservation Slip (Personal User)amrit90320Nessuna valutazione finora

- SLM-19667-BBA - Fiancial Markets and InstitutionsDocumento155 pagineSLM-19667-BBA - Fiancial Markets and InstitutionsMadhusudanNessuna valutazione finora

- SidbiDocumento26 pagineSidbiAnand JoshiNessuna valutazione finora

- History of EurobondsDocumento2 pagineHistory of Eurobondsterigand50% (2)

- D.V.V. Satya Prasad and Ors. vs. The Government of AndhraDocumento42 pagineD.V.V. Satya Prasad and Ors. vs. The Government of AndhrapraveenaNessuna valutazione finora