Potrebbero piacerti anche

- Custom DutyDocumento40 pagineCustom DutyVijayasarathi VenugopalNessuna valutazione finora

- Unit V: Export IncentivesDocumento37 pagineUnit V: Export IncentivesthensureshNessuna valutazione finora

- An Approach To How To Trade in Commodities Market 13052013Documento6 pagineAn Approach To How To Trade in Commodities Market 13052013sskr1307Nessuna valutazione finora

- Forex Business Plan.01Documento8 pagineForex Business Plan.01Kelvin Tafara SamboNessuna valutazione finora

- Day 2 - Sample-Trade-PlanDocumento3 pagineDay 2 - Sample-Trade-PlanJager HunterNessuna valutazione finora

- Order Execution Policy PDFDocumento20 pagineOrder Execution Policy PDFJennifer TimtimNessuna valutazione finora

- Critical Steps to Forex Trading Success for BeginnersDa EverandCritical Steps to Forex Trading Success for BeginnersNessuna valutazione finora

- Compounding SheetDocumento4 pagineCompounding SheetMouzam AliNessuna valutazione finora

- Advanced Forex Breakouts Preview Peter July 2012Documento92 pagineAdvanced Forex Breakouts Preview Peter July 2012aasdasdfNessuna valutazione finora

- The Lost Secret of ForexDocumento3 pagineThe Lost Secret of Forexlroyal23Nessuna valutazione finora

- Building A Trading PlanDocumento2 pagineBuilding A Trading PlanGeorge KangasNessuna valutazione finora

- MultiBank Company Profile English 2022Documento24 pagineMultiBank Company Profile English 2022Anonymous CQ4rbzLVENessuna valutazione finora

- Sales Tax On Services in PakistanDocumento98 pagineSales Tax On Services in Pakistansaudhassan100% (1)

- Director Trade Compliance in USA Resume John McElroyDocumento2 pagineDirector Trade Compliance in USA Resume John McElroyJohnMcElroy100% (1)

- Memorandum Articles of Association enDocumento24 pagineMemorandum Articles of Association enrahmajdNessuna valutazione finora

- FXST Business ManualDocumento25 pagineFXST Business ManualPDDY20002981100% (2)

- Intravest Forex Trading JournalDocumento26 pagineIntravest Forex Trading JournalEDWIN100% (1)

- Counter TradeDocumento30 pagineCounter TradeBharti VirmaniNessuna valutazione finora

- Foreign Exchange1Documento84 pagineForeign Exchange1Ashwin WasnikNessuna valutazione finora

- Piyush PPT of ZRAMDocumento16 paginePiyush PPT of ZRAMPiyush SharmaNessuna valutazione finora

- Introducing A Forex Trading BreakthroughDocumento12 pagineIntroducing A Forex Trading Breakthroughrajronson6938Nessuna valutazione finora

- Stock-Option-Trading-Tips-Provided-By-Theequicom-For Today-24-September-2014Documento7 pagineStock-Option-Trading-Tips-Provided-By-Theequicom-For Today-24-September-2014Riya VermaNessuna valutazione finora

- Autochartist enDocumento6 pagineAutochartist enAnonymous fE2l3DzlNessuna valutazione finora

- FOREXDocumento15 pagineFOREXmanoranjanpatra100% (3)

- Mental Training For Trading Success: CoachingDocumento5 pagineMental Training For Trading Success: CoachingAjith Moses0% (1)

- CCTV MAF and WarrantyDocumento2 pagineCCTV MAF and WarrantyChendu Camila ZangpoNessuna valutazione finora

- Chapter 1 Spot Exchange MarketDocumento20 pagineChapter 1 Spot Exchange Marketchaman_shrestha100% (2)

- Companies Involved in Online TradingDocumento10 pagineCompanies Involved in Online TradingAzaruddin Shaik B PositiveNessuna valutazione finora

- View Our You Tube Video To Know How To Trade Using Below LevelsDocumento3 pagineView Our You Tube Video To Know How To Trade Using Below LevelsNANDHA KUMARNessuna valutazione finora

- Market Fishers (The FiboTrend Strategy)Documento29 pagineMarket Fishers (The FiboTrend Strategy)TZ Mokoena100% (1)

- Trade Details: Half-Position of GBPDocumento4 pagineTrade Details: Half-Position of GBPImre GamsNessuna valutazione finora

- Unit-4 - Trading, Clearing and SettlementDocumento35 pagineUnit-4 - Trading, Clearing and SettlementK DIVYANessuna valutazione finora

- Fundamental and Technical AnalysisDocumento19 pagineFundamental and Technical AnalysisKarthi KeyanNessuna valutazione finora

- 6 Psychology Rules in TradingDocumento6 pagine6 Psychology Rules in Tradingfaiziiik2004Nessuna valutazione finora

- How To Spot Trading ChannelsDocumento54 pagineHow To Spot Trading ChannelsSundaresan SubramanianNessuna valutazione finora

- IgniteDocumento4 pagineIgniteTarunVarmaNessuna valutazione finora

- ActiveTrader User GuideDocumento50 pagineActiveTrader User GuideAhmed SaeedNessuna valutazione finora

- WWW BabypipsDocumento2 pagineWWW BabypipsSourabh BodkeNessuna valutazione finora

- Starbucks Corporation (SBUX) Balance SheetDocumento2 pagineStarbucks Corporation (SBUX) Balance Sheetstevan joeNessuna valutazione finora

- Jurnal Trading - TP - CLDocumento3 pagineJurnal Trading - TP - CLTrader Kaki LimaNessuna valutazione finora

- Annual ReportDocumento160 pagineAnnual ReportSivaNessuna valutazione finora

- Build You Own Trading StrategyDocumento5 pagineBuild You Own Trading StrategyTajudeen Adebayo100% (1)

- How To Open A Deriv Forex Account. PDF-4Documento30 pagineHow To Open A Deriv Forex Account. PDF-4moatlhodiNessuna valutazione finora

- How To Use IGCS in Your Trading PDFDocumento11 pagineHow To Use IGCS in Your Trading PDFNil DorcaNessuna valutazione finora

- Marketing PPT AssignmentDocumento13 pagineMarketing PPT AssignmentBogdan TomaNessuna valutazione finora

- Handbook of Procedures 2023Documento212 pagineHandbook of Procedures 2023Doond adminNessuna valutazione finora

- Commodities TradingDocumento2 pagineCommodities TradingAdityaKumarNessuna valutazione finora

- CRYPTO SCALPING STRATEGY - The Prop TraderDocumento2 pagineCRYPTO SCALPING STRATEGY - The Prop Traderyoussner327Nessuna valutazione finora

- Introduction To Forex ManagementDocumento6 pagineIntroduction To Forex ManagementDivakara Reddy100% (1)

- Financial Statement AnalysisDocumento48 pagineFinancial Statement Analysisroygaurav142Nessuna valutazione finora

- Options Introduction - TsugiTradesDocumento5 pagineOptions Introduction - TsugiTradeshassanomer2122Nessuna valutazione finora

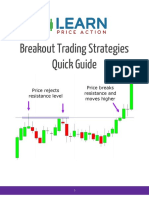

- Breakout Trading Strategies Quick GuideDocumento10 pagineBreakout Trading Strategies Quick GuideKiran KrishnaNessuna valutazione finora

- How To Use IG Client SentimentDocumento7 pagineHow To Use IG Client SentimentRJ Zeshan AwanNessuna valutazione finora

- FX GOAT SessionsDocumento6 pagineFX GOAT Sessionsjames johnNessuna valutazione finora

- Appendix A - Trading Plan Template: Financial GoalDocumento3 pagineAppendix A - Trading Plan Template: Financial GoalBrian KohlerNessuna valutazione finora

- Forex For Beginners: "Rapid Quick Start Manual" by Brian CampbellDocumento10 pagineForex For Beginners: "Rapid Quick Start Manual" by Brian CampbellBudi MulyonoNessuna valutazione finora

- How To Catch BlockbusterstocksDocumento12 pagineHow To Catch Blockbusterstocksdr.kabirdev100% (1)

- Learn Import Export Business From Industry ExpertsDocumento8 pagineLearn Import Export Business From Industry ExpertsImpex FedNessuna valutazione finora

- IIFL Amey Kulkarni PDFDocumento48 pagineIIFL Amey Kulkarni PDFPALLAVI KAMBLENessuna valutazione finora

- New Microsoft Office Word Document 220815Documento5 pagineNew Microsoft Office Word Document 220815Abhishek AgarwalNessuna valutazione finora

- Hindi: V VK B BZ M Å - , , S Vks Vks Va V &&&&&&&&& BZ &&&&&&&&&& VK &&&&&&&&& M &&&&&&&&&& B &&&&&&&&& Å &&&&&&&&&&Documento4 pagineHindi: V VK B BZ M Å - , , S Vks Vks Va V &&&&&&&&& BZ &&&&&&&&&& VK &&&&&&&&& M &&&&&&&&&& B &&&&&&&&& Å &&&&&&&&&&Abhishek AgarwalNessuna valutazione finora

- Gaana Plus Subscription - 6 Months: Grand Total 0.00Documento2 pagineGaana Plus Subscription - 6 Months: Grand Total 0.00Abhishek AgarwalNessuna valutazione finora

- Ym+Dk) Ksim+H) Ia (KK) V (KJKSVDocumento6 pagineYm+Dk) Ksim+H) Ia (KK) V (KJKSVAbhishek AgarwalNessuna valutazione finora

- New Microsoft Office Word Document FinalDocumento105 pagineNew Microsoft Office Word Document FinalAbhishek AgarwalNessuna valutazione finora

- Inventory Management System: Project Report OnDocumento1 paginaInventory Management System: Project Report OnAbhishek AgarwalNessuna valutazione finora

- Table Contents FinalDocumento2 pagineTable Contents FinalAbhishek AgarwalNessuna valutazione finora

- Redico ProjectDocumento94 pagineRedico ProjectAbhishek AgarwalNessuna valutazione finora

- Submitted in The Partial Fulfillment For The Degree of Master of Business "Administration" (Affiliated To Utter Pradesh Technical University, Lucknow)Documento74 pagineSubmitted in The Partial Fulfillment For The Degree of Master of Business "Administration" (Affiliated To Utter Pradesh Technical University, Lucknow)Abhishek AgarwalNessuna valutazione finora

- Sherkhan ProjectDocumento96 pagineSherkhan ProjectAbhishek AgarwalNessuna valutazione finora

- Custom Tambola Housie Tickets PDFDocumento5 pagineCustom Tambola Housie Tickets PDFAbhishek AgarwalNessuna valutazione finora

- Covering Letter: ComputerDocumento4 pagineCovering Letter: ComputerAbhishek AgarwalNessuna valutazione finora

- MIMR IndianBkgSys2 2011Documento71 pagineMIMR IndianBkgSys2 2011Abhishek AgarwalNessuna valutazione finora

- Country Analysis-BRAZILDocumento36 pagineCountry Analysis-BRAZILAbhishek AgarwalNessuna valutazione finora

- Mergers & Acquisitions Presentation On Mauritius: Group MembersDocumento37 pagineMergers & Acquisitions Presentation On Mauritius: Group MembersAbhishek AgarwalNessuna valutazione finora

- Liability of Third Person To PrincipalDocumento34 pagineLiability of Third Person To PrincipalKate CyrilNessuna valutazione finora

- 2021-06-07 Yoe Suárez Case UpdateDocumento1 pagina2021-06-07 Yoe Suárez Case UpdateGlobal Liberty AllianceNessuna valutazione finora

- Letter of IntentDocumento3 pagineLetter of Intentthe next miamiNessuna valutazione finora

- Raw Jute Consumption Reconciliation For 2019 2020 Product Wise 07.9.2020Documento34 pagineRaw Jute Consumption Reconciliation For 2019 2020 Product Wise 07.9.2020Swastik MaheshwaryNessuna valutazione finora

- Crimson Skies (2000) ManualDocumento37 pagineCrimson Skies (2000) ManualJing CaiNessuna valutazione finora

- Noise BookletDocumento8 pagineNoise BookletRuth Viotti SaldanhaNessuna valutazione finora

- CivproDocumento60 pagineCivprodeuce scriNessuna valutazione finora

- Chemical Bonding & Molecular Structure QuestionsDocumento5 pagineChemical Bonding & Molecular Structure QuestionssingamroopaNessuna valutazione finora

- Ramiro, Lorren - Money MarketsDocumento4 pagineRamiro, Lorren - Money Marketslorren ramiroNessuna valutazione finora

- Compania - General - de - Tabacos - de - Filipinas - V.20180926-5466-1aysvyyDocumento16 pagineCompania - General - de - Tabacos - de - Filipinas - V.20180926-5466-1aysvyyKier Christian Montuerto InventoNessuna valutazione finora

- OSG Reply - Republic V SerenoDocumento64 pagineOSG Reply - Republic V SerenoOffice of the Solicitor General - Republic of the Philippines100% (2)

- Merger Final 1Documento18 pagineMerger Final 1vgh nhytfNessuna valutazione finora

- Mockbar 2018 Criminal-Law GarciaDocumento9 pagineMockbar 2018 Criminal-Law GarciasmileycroixNessuna valutazione finora

- Legal Basis of International RelationsDocumento22 pagineLegal Basis of International RelationsCyra ArquezNessuna valutazione finora

- Project Report ON Ladies Garments (Tailoring-Unit)Documento4 pagineProject Report ON Ladies Garments (Tailoring-Unit)Global Law FirmNessuna valutazione finora

- FTP Chart1Documento1 paginaFTP Chart1api-286531621Nessuna valutazione finora

- MD Sirajul Haque Vs The State and OrsDocumento7 pagineMD Sirajul Haque Vs The State and OrsA.B.M. Imdadul Haque KhanNessuna valutazione finora

- Unit 1 - The Crisis of The Ancien Régime and The EnlightenmentDocumento2 pagineUnit 1 - The Crisis of The Ancien Régime and The EnlightenmentRebecca VazquezNessuna valutazione finora

- Petron Vs CaberteDocumento2 paginePetron Vs CabertejohneurickNessuna valutazione finora

- Saida DahirDocumento1 paginaSaida Dahirapi-408883036Nessuna valutazione finora

- Exhaution of Administrative Remedies and The Doctrine of Primary JurisdictionDocumento3 pagineExhaution of Administrative Remedies and The Doctrine of Primary JurisdictionSebastian BorcesNessuna valutazione finora

- Binani Industries Ltd. V. Bank of Baroda and Another - An AnalysisDocumento4 pagineBinani Industries Ltd. V. Bank of Baroda and Another - An AnalysisJeams ZiaurNessuna valutazione finora

- JWB Thesis 05 04 2006Documento70 pagineJWB Thesis 05 04 2006Street Vendor ProjectNessuna valutazione finora

- Assignment On Business PlanDocumento28 pagineAssignment On Business PlanFauzia AfrozaNessuna valutazione finora

- Contract Act 4 PDFDocumento18 pagineContract Act 4 PDFyisjoxaNessuna valutazione finora

- Department of Labor: Kaiser Permanente Bridge ProgramDocumento1 paginaDepartment of Labor: Kaiser Permanente Bridge ProgramUSA_DepartmentOfLaborNessuna valutazione finora

- Pestano V Sumayang, SandovalDocumento2 paginePestano V Sumayang, SandovalTricia SandovalNessuna valutazione finora

- God'S Order For Family Life: 1. God Created Man (Male/Female) in His Own Image (Documento7 pagineGod'S Order For Family Life: 1. God Created Man (Male/Female) in His Own Image (Divino Henrique SantanaNessuna valutazione finora

- Lecture 2 Partnership FormationDocumento58 pagineLecture 2 Partnership FormationSherwin Benedict SebastianNessuna valutazione finora

- MOU Barangay CuliananDocumento4 pagineMOU Barangay CuliananAldrinAbdurahimNessuna valutazione finora