Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

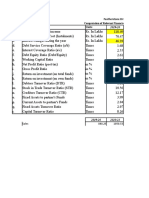

- Jindal Steel Ratio AnalysisDocumento1 paginaJindal Steel Ratio Analysismir danish anwarNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Pre Defined ReportDocumento43 paginePre Defined ReportkjkeNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Fsa - Formula SheetDocumento2 pagineFsa - Formula SheetJustine JacksonNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Fabm Module5Documento20 pagineFabm Module5Paulo VisitacionNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Fundamentals of Accountancy Business and Management II Module 2Documento5 pagineFundamentals of Accountancy Business and Management II Module 2Rafael RetubisNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Use The Following Information For The Next Two QuestionsDocumento25 pagineUse The Following Information For The Next Two QuestionsJovel Paycana100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Classroom Exercises On Consolidation With Intercompany Sale of InventoryDocumento7 pagineClassroom Exercises On Consolidation With Intercompany Sale of InventoryRedNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Featherstone Dry Mix Pvt. Ltd. Serial Particulars Units: Sales 848.25 1050.53Documento39 pagineFeatherstone Dry Mix Pvt. Ltd. Serial Particulars Units: Sales 848.25 1050.53saubhik goswamiNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- M03 Gitman50803X 14 MF C03Documento65 pagineM03 Gitman50803X 14 MF C03layan123456Nessuna valutazione finora

- Test Bank For Financial Reporting 3rd Edition Janice Loftus Ken Leo Sorin Daniliuc Noel Boys Belinda Luke Hong Nee Ang Karyn Byrnes DownloadDocumento12 pagineTest Bank For Financial Reporting 3rd Edition Janice Loftus Ken Leo Sorin Daniliuc Noel Boys Belinda Luke Hong Nee Ang Karyn Byrnes Downloadtonyafosternmzdfpwtgb100% (22)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- FSA IFRS Test QuestionsDocumento51 pagineFSA IFRS Test QuestionsArmand Hajdaraj33% (3)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Assets - Transferable Securi ... Etc.Documento51 pagineAssets - Transferable Securi ... Etc.orizontasNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Chap 8Documento63 pagineChap 8Jose Martin Castillo PatiñoNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Answer Key Prelim ExamDocumento11 pagineAnswer Key Prelim ExamJerald Jardeliza100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- For Filing - Emp 1h 2022 Complete SetDocumento45 pagineFor Filing - Emp 1h 2022 Complete SetBORDALLO JAYMHARKNessuna valutazione finora

- HKICPA QP Exam (Module A) Feb2008 AnswerDocumento10 pagineHKICPA QP Exam (Module A) Feb2008 Answercynthia tsui100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- SALWA Business PlanDocumento62 pagineSALWA Business Planسلوئ اءزواني عبدالله سحىمىNessuna valutazione finora

- Situation 8 11Documento8 pagineSituation 8 11GuinevereNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- SMEsDocumento3 pagineSMEsLayJohn LacadenNessuna valutazione finora

- Cost Accounting A Managerial Emphasis Canadian 15th Edition Horngren Test BankDocumento7 pagineCost Accounting A Managerial Emphasis Canadian 15th Edition Horngren Test Bankatwovarusbbn8d96% (25)

- Statement of Financial Position: Fundamental of Accountancy, Business, and Management 2 ABM12Documento53 pagineStatement of Financial Position: Fundamental of Accountancy, Business, and Management 2 ABM12Mercy P. YbanezNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- 61809bos50279 cp7 U1Documento61 pagine61809bos50279 cp7 U1Sukhmeet Singh100% (1)

- Fac4862 2021 TL 102 0 BDocumento125 pagineFac4862 2021 TL 102 0 BSphamandla MakalimaNessuna valutazione finora

- Bus MathsDocumento22 pagineBus MathsReal JoyNessuna valutazione finora

- ACCOUNTS QuestionsDocumento14 pagineACCOUNTS QuestionsBrit MorganNessuna valutazione finora

- Ratio Analysis Memo and Presentation: ACCA 500Documento8 pagineRatio Analysis Memo and Presentation: ACCA 500Awrangzeb AwrangNessuna valutazione finora

- Advanced Accounting PDFDocumento14 pagineAdvanced Accounting PDFMarie Christine RamosNessuna valutazione finora

- Depreciation of Non-Current AssetsDocumento2 pagineDepreciation of Non-Current AssetsLilian OngNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Advanced Accounting ProblemsDocumento4 pagineAdvanced Accounting ProblemsAjay Sharma0% (1)

- TUTORIAL 7 Capital BudgetingDocumento2 pagineTUTORIAL 7 Capital BudgetingBrenda BernardNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)