Potrebbero piacerti anche

- Induction ProgrammeDocumento3 pagineInduction Programmeabose06Nessuna valutazione finora

- Retail NewsDocumento3 pagineRetail Newsabose06Nessuna valutazione finora

- Retail NewsDocumento3 pagineRetail Newsabose06Nessuna valutazione finora

- Spanish Basic GrammarDocumento37 pagineSpanish Basic Grammarabose06100% (1)

- SWOT Analysis for Future Growth and Competitive PricingDocumento1 paginaSWOT Analysis for Future Growth and Competitive Pricingabose06Nessuna valutazione finora

- Pay ModelDocumento18 paginePay ModelChaitali Patel100% (1)

- 21 Day Bikini BodyDocumento4 pagine21 Day Bikini BodydocumentexchangeonlyNessuna valutazione finora

- Stevenson Twenty Cases Suggestive of ReincarnationDocumento420 pagineStevenson Twenty Cases Suggestive of ReincarnationAdela Patiu100% (1)

- Dishonour of ChequesDocumento15 pagineDishonour of Chequesabose06Nessuna valutazione finora

- How To Launch An Employee Induction ProcessDocumento3 pagineHow To Launch An Employee Induction ProcessSylvester SirvelNessuna valutazione finora

- HR Reading MaterialDocumento1 paginaHR Reading Materialabose06Nessuna valutazione finora

- Stevenson Twenty Cases Suggestive of ReincarnationDocumento420 pagineStevenson Twenty Cases Suggestive of ReincarnationAdela Patiu100% (1)

- Learning by Experience For AdultsDocumento1 paginaLearning by Experience For Adultsabose06Nessuna valutazione finora

- CRM at Big BazaarDocumento16 pagineCRM at Big Bazaarabose06Nessuna valutazione finora

- Disaster Statistics - Brazil - Americas - Countries & Regions - PreventionWebDocumento5 pagineDisaster Statistics - Brazil - Americas - Countries & Regions - PreventionWebabose06Nessuna valutazione finora

- Learning by Experience For AdultsDocumento1 paginaLearning by Experience For Adultsabose06Nessuna valutazione finora

- Why Is Induction So Important - HR PulseDocumento3 pagineWhy Is Induction So Important - HR Pulseabose06Nessuna valutazione finora

- India The Rise of Asian GiantDocumento4 pagineIndia The Rise of Asian Giantabose06Nessuna valutazione finora

- TPI TheoryDocumento1 paginaTPI Theoryabose06Nessuna valutazione finora

- India's Super Economy Tag Is Clearly A LaughDocumento5 pagineIndia's Super Economy Tag Is Clearly A Laughabose06Nessuna valutazione finora

- Flag and IntroDocumento1 paginaFlag and Introabose06Nessuna valutazione finora

- Moody's Upgrades Brazil To Baa3 and Assigns A Positive OutlookDocumento3 pagineMoody's Upgrades Brazil To Baa3 and Assigns A Positive Outlookabose06Nessuna valutazione finora

- 4g PDFDocumento3 pagine4g PDFabose06Nessuna valutazione finora

- Brazil Unctad ReportDocumento3 pagineBrazil Unctad Reportabose06Nessuna valutazione finora

- Brazil Unctad ReportDocumento3 pagineBrazil Unctad Reportabose06Nessuna valutazione finora

- HRM AssDocumento6 pagineHRM Assabose06Nessuna valutazione finora

- HRMDocumento31 pagineHRMtalhaqmNessuna valutazione finora

- THOMAS HARDY’S PESSIMISM EXPOSED THROUGH HIS NOVELSDocumento23 pagineTHOMAS HARDY’S PESSIMISM EXPOSED THROUGH HIS NOVELSabose06100% (1)

- Brazil Unctad ReportDocumento3 pagineBrazil Unctad Reportabose06Nessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5782)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (72)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Exam History Transcript 5354100720293787408Documento2 pagineExam History Transcript 5354100720293787408Ali HussainNessuna valutazione finora

- Accounting Standards For Deferred TaxDocumento17 pagineAccounting Standards For Deferred TaxRishi AgnihotriNessuna valutazione finora

- Customer Relationship Management and Patronage in Service Industry (A Study of Hotel)Documento76 pagineCustomer Relationship Management and Patronage in Service Industry (A Study of Hotel)chukwu solomon100% (1)

- UNIT 1 Talent ManagementDocumento15 pagineUNIT 1 Talent ManagementTapasya JainNessuna valutazione finora

- Laxmi AdhimulamDocumento5 pagineLaxmi Adhimulamja liNessuna valutazione finora

- Consumer Behaviour in Tourism Part 1Documento9 pagineConsumer Behaviour in Tourism Part 1NHU LE THI QUYNHNessuna valutazione finora

- Mgu - 3 - Jurnal - Posting REVDocumento30 pagineMgu - 3 - Jurnal - Posting REVOrrindwirsNessuna valutazione finora

- Works Done: Intern Name: Mamtha Eswari K Guided By: Parul ChopraDocumento155 pagineWorks Done: Intern Name: Mamtha Eswari K Guided By: Parul ChopraMamtha KumarNessuna valutazione finora

- Aligning Rewards To Organizational Goals A Multinational's ExperienceDocumento10 pagineAligning Rewards To Organizational Goals A Multinational's Experienceyanto azie setya100% (2)

- Syllabus of INTERNATIONAL HUMAN RESOURCE MANAGEMENTDocumento49 pagineSyllabus of INTERNATIONAL HUMAN RESOURCE MANAGEMENTSavita RaoNessuna valutazione finora

- Brigham Powerpoint ch01Documento17 pagineBrigham Powerpoint ch01AhsanNessuna valutazione finora

- Data Strategy - Case AnalysisDocumento2 pagineData Strategy - Case AnalysisMissCatLoverNessuna valutazione finora

- Legal Compliance ProcedureDocumento6 pagineLegal Compliance ProcedureSanjeet SinghNessuna valutazione finora

- Module: Competing in The Network EconomyDocumento32 pagineModule: Competing in The Network EconomyKirti KiranNessuna valutazione finora

- Maximize revenue from acquisition and activation budgetsDocumento3 pagineMaximize revenue from acquisition and activation budgetsAnkit ChauhanNessuna valutazione finora

- Business Plan TheatreDocumento17 pagineBusiness Plan TheatreLeila MichelleNessuna valutazione finora

- 3.SMS Manual PDFDocumento222 pagine3.SMS Manual PDFKingsely.shu100% (2)

- Status of Primary Market Response in Nepal: Jas Bahadur GurungDocumento13 pagineStatus of Primary Market Response in Nepal: Jas Bahadur GurungSonam ShahNessuna valutazione finora

- Coca Cola Enterprises - The Value of Automating Order Management - tcm121-70669Documento20 pagineCoca Cola Enterprises - The Value of Automating Order Management - tcm121-70669Rahul SachdevaNessuna valutazione finora

- Logistics Execution Process AgendaDocumento30 pagineLogistics Execution Process AgendaAbhijit Patil50% (2)

- AL Form Individual RevisedDocumento3 pagineAL Form Individual RevisedMicaela ImperialNessuna valutazione finora

- Mansa Building CaseDocumento5 pagineMansa Building CaseshreeshNessuna valutazione finora

- Competitive Advantage of Corporate PhilanthropyDocumento2 pagineCompetitive Advantage of Corporate PhilanthropyJona Mae Milla100% (1)

- Broker System SRS Group 2Documento16 pagineBroker System SRS Group 2mhaaland97Nessuna valutazione finora

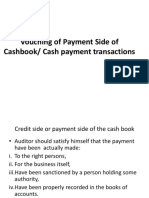

- Vouching of The Payment Side of CashbookDocumento28 pagineVouching of The Payment Side of Cashbooksanthosh prabhu mNessuna valutazione finora

- ACC205 Intermediate Accounting 1 AssignmentsDocumento21 pagineACC205 Intermediate Accounting 1 AssignmentsClarence Allen MasicatNessuna valutazione finora

- Tetra PakDocumento25 pagineTetra PakArslan Aftab50% (2)

- IFRS 15 (Questions)Documento9 pagineIFRS 15 (Questions)adeelkacaNessuna valutazione finora

- Swift Payment, CBPR+ & ISO 20022 Syllabus PDFDocumento5 pagineSwift Payment, CBPR+ & ISO 20022 Syllabus PDFEducative TVNessuna valutazione finora

- G12 Q1 Abm Entrep M 4Documento5 pagineG12 Q1 Abm Entrep M 4Cathleenbeth MorialNessuna valutazione finora