Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Employement CertificateDocumento1 paginaEmployement Certificateemmanuel JohnyNessuna valutazione finora

- Highlight of Union Budget 2011-12Documento11 pagineHighlight of Union Budget 2011-12emmanuel JohnyNessuna valutazione finora

- Material of As 28Documento48 pagineMaterial of As 28emmanuel JohnyNessuna valutazione finora

- Bis-Electrical Code Is - sp.30.2011Documento411 pagineBis-Electrical Code Is - sp.30.2011Seema SharmaNessuna valutazione finora

- Material of As 16Documento21 pagineMaterial of As 16emmanuel JohnyNessuna valutazione finora

- Construction Contracts An AnalysisDocumento29 pagineConstruction Contracts An Analysisemmanuel JohnyNessuna valutazione finora

- RBI MoneyKumar ComicDocumento24 pagineRBI MoneyKumar Comicbhoopathy100% (1)

- Central Plan Outlay by Ministries/Departments (Union Budget 2010-11 Tabular Presenation)Documento4 pagineCentral Plan Outlay by Ministries/Departments (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNessuna valutazione finora

- Highlights of Central Plan 2010-2011 (Union Budget 2010-11 Tabular Presenation)Documento8 pagineHighlights of Central Plan 2010-2011 (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNessuna valutazione finora

- Resources Transferred To States and U.T. Govt (Union Budget 2010-11 Tabular Presenation)Documento2 pagineResources Transferred To States and U.T. Govt (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNessuna valutazione finora

- Revenue Account - ReceiptsDocumento3 pagineRevenue Account - Receiptsemmanuel JohnyNessuna valutazione finora

- Raju and The Money TreeDocumento10 pagineRaju and The Money TreeChandan MundhraNessuna valutazione finora

- Central Plan Outlay by Sectors (Union Budget 2010-11 Tabular Presenation)Documento2 pagineCentral Plan Outlay by Sectors (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNessuna valutazione finora

- Expenditure (Union Budget 2010-11 Tabular Presenation)Documento4 pagineExpenditure (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNessuna valutazione finora

- Central Plan Outlay (Union Budget 2010-11 Tabular Presenation)Documento1 paginaCentral Plan Outlay (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNessuna valutazione finora

- Revenue Account - DisbursementsDocumento3 pagineRevenue Account - Disbursementsemmanuel JohnyNessuna valutazione finora

- Budget at A Glance (Union Budget 2010-11 Tabular Presenation)Documento2 pagineBudget at A Glance (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNessuna valutazione finora

- Receipts (Union Budget 2010-11 Tabular Presenation)Documento2 pagineReceipts (Union Budget 2010-11 Tabular Presenation)emmanuel Johny100% (1)

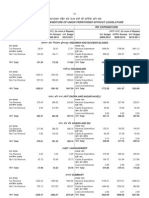

- Receipts and Expenditure of Union Territories Without LegislatureDocumento1 paginaReceipts and Expenditure of Union Territories Without Legislatureemmanuel JohnyNessuna valutazione finora

- Macro Economic Framework Statement 2010 11Documento6 pagineMacro Economic Framework Statement 2010 11emmanuel JohnyNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Examination: Subject ST7 - General Insurance: Reserving and Capital Modelling Specialist TechnicalDocumento6 pagineExamination: Subject ST7 - General Insurance: Reserving and Capital Modelling Specialist Technicaldickson phiriNessuna valutazione finora

- Option Chain (Equity Derivatives)Documento2 pagineOption Chain (Equity Derivatives)sudhakarrrrrrNessuna valutazione finora

- Anthony W Ishii Financial Disclosure Report For 2010Documento6 pagineAnthony W Ishii Financial Disclosure Report For 2010Judicial Watch, Inc.Nessuna valutazione finora

- SEBIDocumento60 pagineSEBIKinjal Rupani90% (10)

- Elder SystemDocumento16 pagineElder Systemhighmail8877100% (4)

- 12 2 11Documento2 pagine12 2 11AshleyNessuna valutazione finora

- Enhanced Gis Revised v.2013 092513Documento9 pagineEnhanced Gis Revised v.2013 092513itsmichikoNessuna valutazione finora

- Commercial Law FaqsDocumento30 pagineCommercial Law FaqsDiane UyNessuna valutazione finora

- List of Shareholders' Unpaid/Unclaimed Dividend Amount For The Financial Year 2010-11Documento278 pagineList of Shareholders' Unpaid/Unclaimed Dividend Amount For The Financial Year 2010-11Prem Prakash PoddarNessuna valutazione finora

- Course Syllabus 01 Technical Analysis Training Course PDFDocumento4 pagineCourse Syllabus 01 Technical Analysis Training Course PDFDHANESH UDDHAV PATIL0% (1)

- Annex "D": Securities and Exchange CommissionDocumento2 pagineAnnex "D": Securities and Exchange Commissionanna marie celociaNessuna valutazione finora

- Smart ExecutionDocumento47 pagineSmart ExecutionYAYA100% (4)

- EC563 Lecture 3 - International FinanceDocumento14 pagineEC563 Lecture 3 - International FinanceOisín Ó CionaoithNessuna valutazione finora

- SS 07 Quiz 2 - AnswersDocumento130 pagineSS 07 Quiz 2 - AnswersVan Le Ha100% (1)

- 28 Solved PCC Cost FM Nov09Documento16 pagine28 Solved PCC Cost FM Nov09Karan Joshi100% (1)

- Tariff of Charges 11022016Documento15 pagineTariff of Charges 11022016minek121Nessuna valutazione finora

- ForexSecrets15min enDocumento19 pagineForexSecrets15min enAtif ChaudhryNessuna valutazione finora

- Study and Review of Mutual Funds PDFDocumento6 pagineStudy and Review of Mutual Funds PDFVenkateswaran SNessuna valutazione finora

- We WorkDocumento169 pagineWe WorkDinheirama.comNessuna valutazione finora

- Career FAQs Investment BankingDocumento170 pagineCareer FAQs Investment Bankingashw258100% (1)

- Syailendra Pendapatan Tetap PremiumDocumento1 paginaSyailendra Pendapatan Tetap PremiumAldo FerlyNessuna valutazione finora

- Abridged Annual Report 2013 14 Reliance CommunicationsDocumento96 pagineAbridged Annual Report 2013 14 Reliance CommunicationsVARBALNessuna valutazione finora

- Fin119 Activities PDFDocumento226 pagineFin119 Activities PDFjamesbookNessuna valutazione finora

- Cyborg FinanceDocumento57 pagineCyborg FinancekurtnewmanNessuna valutazione finora

- Ibt Movie ReviewDocumento7 pagineIbt Movie ReviewNorolhaya Usman100% (1)

- Authority To TravelDocumento14 pagineAuthority To TravelFhikery ArdienteNessuna valutazione finora

- Settlement Instruction: 账户名称 Account Name: 账户号码 Account No.Documento1 paginaSettlement Instruction: 账户名称 Account Name: 账户号码 Account No.thitijv6048Nessuna valutazione finora

- Quick Fire Lessons in Options TradingDocumento101 pagineQuick Fire Lessons in Options Tradinganalystbank100% (1)

- 683sol04 PDFDocumento46 pagine683sol04 PDFJonah MoyoNessuna valutazione finora

- Atlas Battery LTD - AR 2017Documento150 pagineAtlas Battery LTD - AR 2017Ali ImranNessuna valutazione finora