Potrebbero piacerti anche

- Theory of A FirmDocumento25 pagineTheory of A FirmShashi Tripathi100% (2)

- 8 Profit Maximisation TR TC AVG COSTSDocumento28 pagine8 Profit Maximisation TR TC AVG COSTSEsha ChaudharyNessuna valutazione finora

- Theory of The Firm 1Documento19 pagineTheory of The Firm 1Syed Ali TurabNessuna valutazione finora

- How Firms Make DecisionsDocumento31 pagineHow Firms Make DecisionsMikhaell TibunsayNessuna valutazione finora

- Unit 2.3 2016 Students PDFDocumento15 pagineUnit 2.3 2016 Students PDFTumi MothusiNessuna valutazione finora

- Colander Ch11 Perfect CompetitionDocumento84 pagineColander Ch11 Perfect CompetitionVishal JoshiNessuna valutazione finora

- AQA Economics Unit 3Documento38 pagineAQA Economics Unit 3dawoudnNessuna valutazione finora

- Applied Economics Firm Behavior: Chapters 8-9Documento25 pagineApplied Economics Firm Behavior: Chapters 8-9cristianaNessuna valutazione finora

- Project Cost Management - CHAPTER 4Documento28 pagineProject Cost Management - CHAPTER 4Abata BageyuNessuna valutazione finora

- Chapter 8 Production, Costs Markets SECONDDocumento25 pagineChapter 8 Production, Costs Markets SECONDSoha HassanNessuna valutazione finora

- Competition & Pure MonopolyDocumento36 pagineCompetition & Pure MonopolyChadi AboukrrroumNessuna valutazione finora

- 1) ANS: Profit Maximization Objective of A Firm: Total Revenue (TR) - Total Cost (TC) ApproachDocumento6 pagine1) ANS: Profit Maximization Objective of A Firm: Total Revenue (TR) - Total Cost (TC) ApproachAhim Raj JoshiNessuna valutazione finora

- SMA - Chapter Seven - Cost-Volume-Profit AnalysisDocumento35 pagineSMA - Chapter Seven - Cost-Volume-Profit Analysisngandu0% (1)

- LectureDocumento15 pagineLectureVivek MishraNessuna valutazione finora

- Unit IVDocumento53 pagineUnit IVS1626Nessuna valutazione finora

- Profit Maximization and Other Objectives of Industrial FirmsDocumento26 pagineProfit Maximization and Other Objectives of Industrial FirmsAnu PariharNessuna valutazione finora

- What Objectives Do Firms Have?Documento53 pagineWhat Objectives Do Firms Have?adnan muridiNessuna valutazione finora

- 03 NotesDocumento5 pagine03 NotesMahendra JarwalNessuna valutazione finora

- 08-LECTURE NOTES - Difference Between Economic and Accounting Profit - MANAGERIAL ECONOMICSDocumento11 pagine08-LECTURE NOTES - Difference Between Economic and Accounting Profit - MANAGERIAL ECONOMICSreagan blaireNessuna valutazione finora

- Managerial Economics 2nd Lecture Notes 2022Documento30 pagineManagerial Economics 2nd Lecture Notes 2022Samantha CruzNessuna valutazione finora

- Firms in The Competitive MarketDocumento40 pagineFirms in The Competitive MarketDeniseNessuna valutazione finora

- Unit 6 - Lesson 9 - Goals of The FirmDocumento9 pagineUnit 6 - Lesson 9 - Goals of The Firmapi-260512563Nessuna valutazione finora

- Theory of The Firm (HL) NotesDocumento24 pagineTheory of The Firm (HL) NotesKumarevel SidaarthNessuna valutazione finora

- BEPDocumento25 pagineBEPujjwalNessuna valutazione finora

- Profit Maxim Is at Ion IEM LABDocumento18 pagineProfit Maxim Is at Ion IEM LABAbhishek ShringiNessuna valutazione finora

- Managerial Economics:: Perfect CompetitionDocumento43 pagineManagerial Economics:: Perfect CompetitionPhong VũNessuna valutazione finora

- Lecture Outline - 9-B - Market Structure - Perfect CompetitionDocumento9 pagineLecture Outline - 9-B - Market Structure - Perfect CompetitionDhanushka RajapakshaNessuna valutazione finora

- Econ202 ch21Documento37 pagineEcon202 ch21Kenny LohNessuna valutazione finora

- Cost-Volume-Profit AnalysisDocumento5 pagineCost-Volume-Profit AnalysisRaiza BarbasNessuna valutazione finora

- Micro and Macro EconomicsDocumento22 pagineMicro and Macro EconomicsKarenMariasusaiNessuna valutazione finora

- Cost AnalysisDocumento42 pagineCost AnalysisrathnakotariNessuna valutazione finora

- Theories of Firm: Dr. Mohsina HayatDocumento46 pagineTheories of Firm: Dr. Mohsina HayatFaizan QudsiNessuna valutazione finora

- Break Even AnalysisDocumento29 pagineBreak Even AnalysisGautam BindlishNessuna valutazione finora

- Market Structure: Chapter FiveDocumento22 pagineMarket Structure: Chapter FiveOromay EliasNessuna valutazione finora

- Chapter 20 NotesDocumento17 pagineChapter 20 NotesRahila RafiqNessuna valutazione finora

- Introduction To Economics 2E / Lieberman & Hallchapter 6 / How Firms Make Decisions: Profit Maximization ©2005, South-Western/Thomson LearningDocumento17 pagineIntroduction To Economics 2E / Lieberman & Hallchapter 6 / How Firms Make Decisions: Profit Maximization ©2005, South-Western/Thomson LearningCristea LaniNessuna valutazione finora

- Market StructureDocumento19 pagineMarket StructureNazmul HudaNessuna valutazione finora

- Microeconomics Principles and Applications 6Th Edition Hall Solutions Manual Full Chapter PDFDocumento32 pagineMicroeconomics Principles and Applications 6Th Edition Hall Solutions Manual Full Chapter PDFVeronicaKellykcqb100% (9)

- Microeconomics Principles and Applications 6th Edition Hall Solutions ManualDocumento11 pagineMicroeconomics Principles and Applications 6th Edition Hall Solutions Manualclubhandbranwq8100% (25)

- Group Report. Perfect CompetitionDocumento31 pagineGroup Report. Perfect CompetitionMary Ann Manalo PanopioNessuna valutazione finora

- Microeconomics Chapter 5Documento8 pagineMicroeconomics Chapter 5Alejandra jpNessuna valutazione finora

- MBA 290-Strategic AnalysisDocumento110 pagineMBA 290-Strategic AnalysisAbhishek SoniNessuna valutazione finora

- CVP AnalysisDocumento16 pagineCVP AnalysisPushkar SharmaNessuna valutazione finora

- CAIE O Level Firms, Cost, Revenue & Objectives PDFDocumento28 pagineCAIE O Level Firms, Cost, Revenue & Objectives PDFDayaan Ameen100% (1)

- MGMT-5245 Managerial Economics: Market Power: MonopolyDocumento22 pagineMGMT-5245 Managerial Economics: Market Power: MonopolyYining LiuNessuna valutazione finora

- Profit "Profit Is Return To The Entrepreneur For The Use of His Ability."Documento6 pagineProfit "Profit Is Return To The Entrepreneur For The Use of His Ability."tunga computer net centerNessuna valutazione finora

- Cost Volume Profit (CVP) AnalysisDocumento60 pagineCost Volume Profit (CVP) AnalysisEtsub SamuelNessuna valutazione finora

- Chapter OneDocumento36 pagineChapter OnemathewosNessuna valutazione finora

- Profit MaximisationDocumento42 pagineProfit MaximisationIrfan Jamal100% (1)

- Advanced Strategic ManagementDocumento110 pagineAdvanced Strategic ManagementDr Rushen SinghNessuna valutazione finora

- 08me-Managerial Theories of The FirmDocumento8 pagine08me-Managerial Theories of The FirmRajiv KarNessuna valutazione finora

- 7b5f53 Analysis of Cost and Revenue 25-04Documento21 pagine7b5f53 Analysis of Cost and Revenue 25-04Shamsuddin SheikhNessuna valutazione finora

- The Goal of Profit MaximizationDocumento18 pagineThe Goal of Profit MaximizationAnton ArponNessuna valutazione finora

- 4 - Market StructureDocumento17 pagine4 - Market Structuremonica rajuNessuna valutazione finora

- Profitmaximization 150318101305 Conversion Gate01Documento9 pagineProfitmaximization 150318101305 Conversion Gate01Glenn Cacho GarceNessuna valutazione finora

- LChpt18 CVPadjDocumento43 pagineLChpt18 CVPadjJacqueline LieNessuna valutazione finora

- Diploma in Management Studies Microeconomics ECO001Documento52 pagineDiploma in Management Studies Microeconomics ECO001babylovelylovelyNessuna valutazione finora

- Economic Concept of Cost - Production and Cost - Short Run Cost Function - Long Run Cost FunctionDocumento23 pagineEconomic Concept of Cost - Production and Cost - Short Run Cost Function - Long Run Cost FunctionAkshatNessuna valutazione finora

- The Balanced Scorecard: Turn your data into a roadmap to successDa EverandThe Balanced Scorecard: Turn your data into a roadmap to successValutazione: 3.5 su 5 stelle3.5/5 (4)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageDa EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageValutazione: 5 su 5 stelle5/5 (1)

- Using Personality Traits To Understand Behavior: For Personality Puzzle 4 Edition Ch. 7Documento7 pagineUsing Personality Traits To Understand Behavior: For Personality Puzzle 4 Edition Ch. 7Aman Singh RajputNessuna valutazione finora

- Chapter 8Documento28 pagineChapter 8Aman Singh RajputNessuna valutazione finora

- Keynes and The Evolution of MacroeconomicsDocumento70 pagineKeynes and The Evolution of MacroeconomicsAman Singh Rajput100% (1)

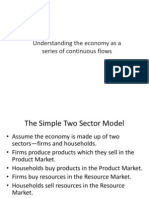

- Understanding The Economy As A Series of Continuous FlowsDocumento12 pagineUnderstanding The Economy As A Series of Continuous FlowsAman Singh RajputNessuna valutazione finora

- Income Determination in Short Run: Basic Model: Ae Y AE (C+I) Ae YDocumento31 pagineIncome Determination in Short Run: Basic Model: Ae Y AE (C+I) Ae YAman Singh RajputNessuna valutazione finora

- MIS PresentationDocumento11 pagineMIS PresentationAman Singh RajputNessuna valutazione finora

- What Is Macroeconomics? Its OriginDocumento55 pagineWhat Is Macroeconomics? Its OriginAman Singh RajputNessuna valutazione finora

- Demand ForecastingDocumento15 pagineDemand ForecastingAman Singh RajputNessuna valutazione finora

- Product Line Pricing or Multi Product PricingDocumento2 pagineProduct Line Pricing or Multi Product PricingAman Singh RajputNessuna valutazione finora

- Baumol and Morris ModelsDocumento10 pagineBaumol and Morris ModelsAman Singh RajputNessuna valutazione finora

- Baumols TheoryDocumento35 pagineBaumols TheoryAman Singh Rajput100% (1)

- New Product PricingDocumento18 pagineNew Product PricingAman Singh RajputNessuna valutazione finora

- MIS PresentationDocumento11 pagineMIS PresentationAman Singh RajputNessuna valutazione finora

- Managing in Competitive, Monopolistic and Monopolistically Competitive MarketsDocumento48 pagineManaging in Competitive, Monopolistic and Monopolistically Competitive MarketseeaadssdfNessuna valutazione finora

- Perfect CompetitionDocumento43 paginePerfect CompetitionMohammad Raihanul HasanNessuna valutazione finora

- Chapter 01: The Role and Objective of Financial Management: Answer: ADocumento17 pagineChapter 01: The Role and Objective of Financial Management: Answer: AKyla Ramos DiamsayNessuna valutazione finora

- Aesthetic Practitioner As A Physician andDocumento5 pagineAesthetic Practitioner As A Physician andmariana sanguinettiNessuna valutazione finora

- Managerial Economics: 14 EditionDocumento41 pagineManagerial Economics: 14 EditionahmadNessuna valutazione finora

- CBM Quiz 1 4Documento6 pagineCBM Quiz 1 4victonsNessuna valutazione finora

- CAT 1 AND 2 EconomicsDocumento4 pagineCAT 1 AND 2 EconomicsIbrahim Mohamed IbrahimNessuna valutazione finora

- COMPETITIVE MARKETS Chapter 10Documento33 pagineCOMPETITIVE MARKETS Chapter 10Ami Mira100% (1)

- Microeconomics Handouts UpdatedDocumento27 pagineMicroeconomics Handouts UpdatedKhalil FanousNessuna valutazione finora

- Solution Problem 1 Problems Handouts MicroDocumento25 pagineSolution Problem 1 Problems Handouts MicrokokokoNessuna valutazione finora

- Sample Final Exam Fall 2019: Name: Class: DateDocumento14 pagineSample Final Exam Fall 2019: Name: Class: DateElovset OrucovNessuna valutazione finora

- Economics For Managers Global Edition 3rd Edition Farnham Solutions ManualDocumento12 pagineEconomics For Managers Global Edition 3rd Edition Farnham Solutions Manualtusseh.itemm0lh100% (28)

- Chapter 6 - Theory of Firm 1 - CambridgeDocumento18 pagineChapter 6 - Theory of Firm 1 - CambridgeHieptaNessuna valutazione finora

- Consider Again The Two Ways in Which We Can ViewDocumento2 pagineConsider Again The Two Ways in Which We Can Viewtrilocksp SinghNessuna valutazione finora

- Managerial Economics - Lecture 4Documento18 pagineManagerial Economics - Lecture 4Fizza MasroorNessuna valutazione finora

- Practice Questions - Monopoly - AnswersDocumento12 paginePractice Questions - Monopoly - AnswersHazel Jean DeteralaNessuna valutazione finora

- For The Multiple-Choice Questions:: MidtermDocumento5 pagineFor The Multiple-Choice Questions:: MidtermDiego soriaNessuna valutazione finora

- Entry, Capacity, Investment and Oligopolistic Pricing (A J) 1977Documento12 pagineEntry, Capacity, Investment and Oligopolistic Pricing (A J) 1977pedronuno20Nessuna valutazione finora

- Managerial Decisions For Firms With Market Power: Essential ConceptsDocumento8 pagineManagerial Decisions For Firms With Market Power: Essential ConceptsRohit SinhaNessuna valutazione finora

- 2019 H2 Y5 CT 1 - Examiner - S Report (Final)Documento20 pagine2019 H2 Y5 CT 1 - Examiner - S Report (Final)19Y5C12 ZHANG YIXIANGNessuna valutazione finora

- Madorodee Economics AssignmentDocumento9 pagineMadorodee Economics AssignmentDIVINE MADORONessuna valutazione finora

- 100-F2014 Assignment 6 Perfect Competition, Monopoly and Consumer Choice TheoryDocumento6 pagine100-F2014 Assignment 6 Perfect Competition, Monopoly and Consumer Choice TheoryKristina Phillpotts-BrownNessuna valutazione finora

- S M C L: Aint Ichael'S Ollege of AgunaDocumento3 pagineS M C L: Aint Ichael'S Ollege of AgunaAnjo Espela VelascoNessuna valutazione finora

- Group Assignment For The Course Introduction To Economics May 9Documento4 pagineGroup Assignment For The Course Introduction To Economics May 9yohannes lemiNessuna valutazione finora

- Ap Micro Chapter 5Documento37 pagineAp Micro Chapter 5henryliguansenNessuna valutazione finora

- Managerial Economics 7th Edition Keat Test BankDocumento14 pagineManagerial Economics 7th Edition Keat Test Bankaureliaeirayetu6s100% (26)

- The Welfare Economics of Competition and MonopolyDocumento21 pagineThe Welfare Economics of Competition and MonopolyEduardo FreitasNessuna valutazione finora

- The Shutdown Point: Scenario 1Documento10 pagineThe Shutdown Point: Scenario 1Carla Mae F. DaduralNessuna valutazione finora

- On The Equivalency of Profit Maximization and Cost MinimizationDocumento7 pagineOn The Equivalency of Profit Maximization and Cost MinimizationRikNessuna valutazione finora

- Module 5 Steve Mendoza Bsentrep 1a Microeconomics Ecc 122Documento6 pagineModule 5 Steve Mendoza Bsentrep 1a Microeconomics Ecc 122Steve MendozaNessuna valutazione finora