Potrebbero piacerti anche

- The List of Components Which You Can Use For Salary BreakupDocumento8 pagineThe List of Components Which You Can Use For Salary BreakupAnonymous VhqxrXNessuna valutazione finora

- Template - Restructuring-Tax Computation-BER-Salary Tracker For FY 2015-16 - CKDocumento9 pagineTemplate - Restructuring-Tax Computation-BER-Salary Tracker For FY 2015-16 - CKajaykrsinghpintuNessuna valutazione finora

- Genpact Vs InfosysDocumento3 pagineGenpact Vs InfosysNidhi MishraNessuna valutazione finora

- What Is A Flexible Benefit Plan in A Salary Breakup? - QuoraDocumento8 pagineWhat Is A Flexible Benefit Plan in A Salary Breakup? - QuoraSiNessuna valutazione finora

- Income Under The Head "Salaries": Shubhangi Gupta Roll No. 11 Financial Management Bhartiya Vidya BhavanDocumento44 pagineIncome Under The Head "Salaries": Shubhangi Gupta Roll No. 11 Financial Management Bhartiya Vidya Bhavanhny0910Nessuna valutazione finora

- Provident Fund Steps - UANDocumento38 pagineProvident Fund Steps - UANSandip ChaudhuriNessuna valutazione finora

- Daksh Leave Policy (India)Documento12 pagineDaksh Leave Policy (India)ajithk75733Nessuna valutazione finora

- Online Registration of Establishment With DSC: User ManualDocumento39 pagineOnline Registration of Establishment With DSC: User ManualroseNessuna valutazione finora

- RegistrationDocumento15 pagineRegistrationpratikdhond100% (3)

- Overtime AllowanceDocumento3 pagineOvertime AllowanceKumudha Devi100% (1)

- Compliance Manual F.Y. 2020 21 A.Y.2021 22 PDFDocumento52 pagineCompliance Manual F.Y. 2020 21 A.Y.2021 22 PDFTHERMAL TECH ENGINEERINGNessuna valutazione finora

- FY08 Car Lease Document V2Documento3 pagineFY08 Car Lease Document V2Swanidhi SinghNessuna valutazione finora

- Family Pension SchemeDocumento15 pagineFamily Pension SchemeJitu Choudhary100% (1)

- Retirement Benefits TaxDocumento18 pagineRetirement Benefits TaxArpit GoyalNessuna valutazione finora

- Kar Shops Commercial Forms FormatDocumento16 pagineKar Shops Commercial Forms FormatbelvaisudheerNessuna valutazione finora

- Salary and Income Tax Heads of Income SalaryfDocumento6 pagineSalary and Income Tax Heads of Income SalaryfMUTHUSAMY RNessuna valutazione finora

- Salary AdministrationDocumento17 pagineSalary AdministrationMae Ann GonzalesNessuna valutazione finora

- HR ComplianceDocumento4 pagineHR ComplianceAchuthan RamanNessuna valutazione finora

- Salary, Net Salary, Gross Salary, Cost To Company Are They Same or Different. For Most People It IsDocumento6 pagineSalary, Net Salary, Gross Salary, Cost To Company Are They Same or Different. For Most People It IsAnonymous CwxsRiwNessuna valutazione finora

- FBP To-Be Process - April 1 India ReleaseDocumento24 pagineFBP To-Be Process - April 1 India Releaseraghava_cseNessuna valutazione finora

- CTS Marriage Loan PolicyDocumento5 pagineCTS Marriage Loan PolicyshaannivasNessuna valutazione finora

- USSP User Manual v1.0Documento18 pagineUSSP User Manual v1.0Siva ChNessuna valutazione finora

- EPF Provident Fund CalculatorDocumento6 pagineEPF Provident Fund CalculatorUtkal SolankiNessuna valutazione finora

- Statutory ComplianceDocumento2 pagineStatutory Compliancemax997Nessuna valutazione finora

- CCS LTC RULES PPT 20210617141434Documento28 pagineCCS LTC RULES PPT 20210617141434Kumar KumarNessuna valutazione finora

- Compliance PDFDocumento20 pagineCompliance PDFSUBHANKAR PALNessuna valutazione finora

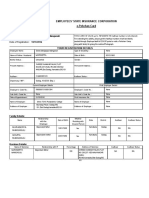

- Employees' State Insurance Corporation E-Pehchan Card: Insured Person: Insurance No.: Date of RegistrationDocumento3 pagineEmployees' State Insurance Corporation E-Pehchan Card: Insured Person: Insurance No.: Date of RegistrationGoutam HotaNessuna valutazione finora

- PF Pension Settlement Form-TCSDocumento4 paginePF Pension Settlement Form-TCSSridhara Krishna BodavulaNessuna valutazione finora

- DeputationDocumento2 pagineDeputationsuryadtp suryadtpNessuna valutazione finora

- Salary Increment PolicyDocumento1 paginaSalary Increment PolicyMd. Muhinur Islam AdnanNessuna valutazione finora

- Esic ChallanDocumento7 pagineEsic Challanrgsr2008Nessuna valutazione finora

- Leave EncashmentDocumento1 paginaLeave EncashmentParamita SarkarNessuna valutazione finora

- FAQ (Flexi) PDFDocumento4 pagineFAQ (Flexi) PDFDivyansh Chand BansalNessuna valutazione finora

- Income Tax DepartmentDocumento19 pagineIncome Tax DepartmentSharathNessuna valutazione finora

- Induction TrainingDocumento17 pagineInduction TrainingShaan BalchandaniNessuna valutazione finora

- Employee Benefits IndiaDocumento2 pagineEmployee Benefits Indiabaskarbaju1Nessuna valutazione finora

- Higher Pension As Per SC Decision With Calculation - Synopsis1Documento13 pagineHigher Pension As Per SC Decision With Calculation - Synopsis1hariveerNessuna valutazione finora

- Local Conveyance PolicyDocumento4 pagineLocal Conveyance PolicyNazneen KhanNessuna valutazione finora

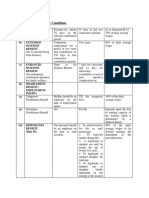

- Benefits & Contributory Conditions: (I) (A) Sickness BenefitDocumento4 pagineBenefits & Contributory Conditions: (I) (A) Sickness BenefitKunwar Sa Amit SinghNessuna valutazione finora

- Guidelines Mediclaim L&TDocumento5 pagineGuidelines Mediclaim L&Tnidnitrkl051296Nessuna valutazione finora

- Annexure - Flexible Benefit PlanDocumento3 pagineAnnexure - Flexible Benefit PlanpvkmanoharNessuna valutazione finora

- Pension CalculationDocumento1 paginaPension Calculationulmilu15Nessuna valutazione finora

- PSB Promotion GuidelinesDocumento24 paginePSB Promotion GuidelinesPranav RaiNessuna valutazione finora

- Dearness Allowance: by Alpi Sharma Kavya Krishnan KDocumento15 pagineDearness Allowance: by Alpi Sharma Kavya Krishnan KKavya KrishnanNessuna valutazione finora

- Pay SlipDocumento50 paginePay SlipSushil Shrestha100% (1)

- MyBenefits@Philips LeafletDocumento2 pagineMyBenefits@Philips Leafletsubodhtaneja100% (1)

- Relevant Dates: 15-Apr QuarterlyDocumento6 pagineRelevant Dates: 15-Apr Quarterlysanyu1208Nessuna valutazione finora

- PSC Circular 52 - Graduate Trainee Scheme Policy in The Public Service PDFDocumento9 paginePSC Circular 52 - Graduate Trainee Scheme Policy in The Public Service PDFManoa Nagatalevu TupouNessuna valutazione finora

- Contract Labour RegisterDocumento34 pagineContract Labour Registerravinder.singh19853857Nessuna valutazione finora

- PF TransferDocumento11 paginePF TransfersinniNessuna valutazione finora

- R.R. Ispat (A Unit of Gpil) : Recruitment PolicyDocumento3 pagineR.R. Ispat (A Unit of Gpil) : Recruitment PolicyVinod KumarNessuna valutazione finora

- AgricultureDocumento4 pagineAgriculturemohan rathoreNessuna valutazione finora

- Karnataka Shops and Commercial Establishments Act, 1961Documento44 pagineKarnataka Shops and Commercial Establishments Act, 1961Latest Laws TeamNessuna valutazione finora

- ECMS User Manual - : PAN IndiaDocumento70 pagineECMS User Manual - : PAN IndiaKrishNessuna valutazione finora

- CompensationDocumento28 pagineCompensationSomalKantNessuna valutazione finora

- Employees' State Insurance Corporation E-Pehchan Card: Insured Person: Insurance No.: Date of RegistrationDocumento2 pagineEmployees' State Insurance Corporation E-Pehchan Card: Insured Person: Insurance No.: Date of RegistrationTontadarya PolytechnicNessuna valutazione finora

- LTA PolicyDocumento2 pagineLTA PolicyAnuradha ParasaramNessuna valutazione finora

- Whichever Is Lower Is Exempt From Tax. For ExampleDocumento13 pagineWhichever Is Lower Is Exempt From Tax. For ExampleJags NagwekarNessuna valutazione finora

- Cost To The CompanyDocumento15 pagineCost To The CompanyrockNessuna valutazione finora

- Income Tax Exemptions For The Year 2010Documento4 pagineIncome Tax Exemptions For The Year 2010Homework PingNessuna valutazione finora

- Abhi18 PDFDocumento8 pagineAbhi18 PDFNasir AhmedNessuna valutazione finora

- Quotation For Light WeightDocumento2 pagineQuotation For Light WeightNasir AhmedNessuna valutazione finora

- Loan To Non Member BranchID Dump1001Documento250 pagineLoan To Non Member BranchID Dump1001Nasir AhmedNessuna valutazione finora

- Tracker December 01 To 12TH 2020Documento12 pagineTracker December 01 To 12TH 2020Nasir AhmedNessuna valutazione finora

- Neet Code A Question PaperDocumento41 pagineNeet Code A Question PaperRohit Kumar JenaNessuna valutazione finora

- Arabian Consultants Pvt. LTDDocumento6 pagineArabian Consultants Pvt. LTDNasir AhmedNessuna valutazione finora

- Details of Verified Recruiting AgenciesDocumento90 pagineDetails of Verified Recruiting AgenciesNasir AhmedNessuna valutazione finora

- The Following Detailed of The Product Specification: Civil Engineering Grade BentoniteDocumento2 pagineThe Following Detailed of The Product Specification: Civil Engineering Grade BentoniteNasir AhmedNessuna valutazione finora

- Á Àä Æã/ Æ Gádpàä Àiágà Vàazé À Àgád ºàauàgàv, Àaiàä Àäì: - Gzéæåãuà: Àå Àºágà Á: C Àgázà (©) Vá.F. Uàä® Uáð Àiáqàä À Àæ Àiát Àvàæ J ÉazàgéDocumento1 paginaÁ Àä Æã/ Æ Gádpàä Àiágà Vàazé À Àgád ºàauàgàv, Àaiàä Àäì: - Gzéæåãuà: Àå Àºágà Á: C Àgázà (©) Vá.F. Uàä® Uáð Àiáqàä À Àæ Àiát Àvàæ J ÉazàgéNasir AhmedNessuna valutazione finora

- AF21417 - Business Development Manager - Open Day Recruitment - Orient - UAEDocumento14 pagineAF21417 - Business Development Manager - Open Day Recruitment - Orient - UAENasir AhmedNessuna valutazione finora

- Challan 199664 19022015 212553Documento1 paginaChallan 199664 19022015 212553Nasir AhmedNessuna valutazione finora

- VCS BrochureDocumento13 pagineVCS BrochureNasir AhmedNessuna valutazione finora

- Dam Maya Magar 509 Sumita Tamang: Hamsa Kalathil Valappil Muhammed Kalathil Valappil Siddique MuhammedDocumento1 paginaDam Maya Magar 509 Sumita Tamang: Hamsa Kalathil Valappil Muhammed Kalathil Valappil Siddique MuhammedNasir AhmedNessuna valutazione finora

- Online Application For Gazetted Probationers Preliminary Examination - 2014Documento2 pagineOnline Application For Gazetted Probationers Preliminary Examination - 2014Nasir AhmedNessuna valutazione finora

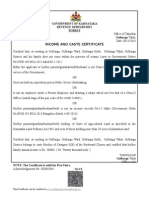

- Income and Caste Certificate: Government of Karnataka Revenue Derpartmet Form-F Gulbarga TalukDocumento2 pagineIncome and Caste Certificate: Government of Karnataka Revenue Derpartmet Form-F Gulbarga TalukNasir AhmedNessuna valutazione finora

- Curriculum Vitae: FebruaryDocumento2 pagineCurriculum Vitae: FebruaryNasir AhmedNessuna valutazione finora

- Online Application For Gazetted Probationers Preliminary Examination - 2014Documento2 pagineOnline Application For Gazetted Probationers Preliminary Examination - 2014Nasir AhmedNessuna valutazione finora

- Um CitizenDocumento28 pagineUm CitizenNasir AhmedNessuna valutazione finora

- RTI Call Centre & Portal ProjectDocumento94 pagineRTI Call Centre & Portal ProjectNasir AhmedNessuna valutazione finora

- Feroz BB ExchangeDocumento5 pagineFeroz BB ExchangeNasir AhmedNessuna valutazione finora

- The Right To Information Act, 2005Documento6 pagineThe Right To Information Act, 2005Nasir AhmedNessuna valutazione finora

- Business Type: Main Products: Location: Year Established: Number of EmployeesDocumento3 pagineBusiness Type: Main Products: Location: Year Established: Number of EmployeesNasir AhmedNessuna valutazione finora