Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Pav CourseDocumento30 paginePav CoursetenglumlowNessuna valutazione finora

- GST 02 - Application For Group or Joint Venture RegistrationDocumento8 pagineGST 02 - Application For Group or Joint Venture RegistrationtenglumlowNessuna valutazione finora

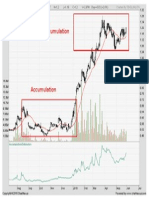

- Analyzing Gaps For Profitable Trading StrategiesDocumento31 pagineAnalyzing Gaps For Profitable Trading StrategiestenglumlowNessuna valutazione finora

- Gst-01c - Details of Overseas PrincipalDocumento7 pagineGst-01c - Details of Overseas PrincipaltenglumlowNessuna valutazione finora

- Gst-01 - Application For Goods and Services Tax Registration Revised 3 Okt 2014Documento9 pagineGst-01 - Application For Goods and Services Tax Registration Revised 3 Okt 2014tenglumlowNessuna valutazione finora

- White Card Online - CPCCOHS1001A - WhiteCard Online - Narbil White CardDocumento3 pagineWhite Card Online - CPCCOHS1001A - WhiteCard Online - Narbil White CardtenglumlowNessuna valutazione finora

- Strategy Note - Must-Own Stocks For Long-Term InvestingDocumento139 pagineStrategy Note - Must-Own Stocks For Long-Term InvestingtenglumlowNessuna valutazione finora

- Royal Malaysian Customs: Guide Approved Trader SchemeDocumento16 pagineRoyal Malaysian Customs: Guide Approved Trader SchemetenglumlowNessuna valutazione finora

- 1MDB Wants Money To Come Back To Malaysia But What Kind of Returns Would The Investments Have Yielded - Business News - The Star OnlineDocumento13 pagine1MDB Wants Money To Come Back To Malaysia But What Kind of Returns Would The Investments Have Yielded - Business News - The Star OnlinetenglumlowNessuna valutazione finora

- SSM Illustration of FS MFRSDocumento76 pagineSSM Illustration of FS MFRStenglumlowNessuna valutazione finora

- Cop Safely Remove AsbestosDocumento72 pagineCop Safely Remove AsbestostenglumlowNessuna valutazione finora

- Royal Malaysian Customs: Guide Approved Toll Manufacturer SchemeDocumento15 pagineRoyal Malaysian Customs: Guide Approved Toll Manufacturer SchemetenglumlowNessuna valutazione finora

- Guidebook Import Export 1Documento279 pagineGuidebook Import Export 1tenglumlowNessuna valutazione finora

- DoorsDocumento18 pagineDoorstenglumlow100% (1)

- EvergreenDocumento1 paginaEvergreentenglumlowNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- City Government of San Pablo V ReyesDocumento2 pagineCity Government of San Pablo V ReyesNikita BayotNessuna valutazione finora

- Canadian Conventions in FI Markets - Release 1.1Documento58 pagineCanadian Conventions in FI Markets - Release 1.1fengnNessuna valutazione finora

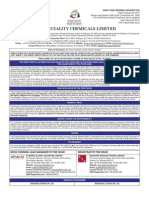

- Omkar Speciality Chemicals Ltd.Documento259 pagineOmkar Speciality Chemicals Ltd.adhavvikasNessuna valutazione finora

- Servlet ControllerDocumento1 paginaServlet ControllerDeepthi SonuNessuna valutazione finora

- Royal AholdDocumento13 pagineRoyal AholdgayatrichaudharyNessuna valutazione finora

- W 8 BenDocumento1 paginaW 8 Bendavid_valentine_184% (19)

- Richard S. Robie v. Edwin I. Ofgant, 306 F.2d 656, 1st Cir. (1962)Documento6 pagineRichard S. Robie v. Edwin I. Ofgant, 306 F.2d 656, 1st Cir. (1962)Scribd Government DocsNessuna valutazione finora

- CFO Chief Financial Officer in Southern CA Resume Richard DrinkwardDocumento3 pagineCFO Chief Financial Officer in Southern CA Resume Richard DrinkwardRichardDrinkwardNessuna valutazione finora

- Case Studies of Good Corporate GovernanceDocumento288 pagineCase Studies of Good Corporate GovernanceIFC Sustainability75% (12)

- Radha Sridhar - 2 - 2019-2020Documento2 pagineRadha Sridhar - 2 - 2019-2020Radha SridharNessuna valutazione finora

- Cash and Accrual BasisDocumento10 pagineCash and Accrual BasisNoeme LansangNessuna valutazione finora

- MIRA 101, English, v14.1 PDFDocumento4 pagineMIRA 101, English, v14.1 PDFNaee ARNessuna valutazione finora

- Super Stockist FormDocumento4 pagineSuper Stockist Formfriendztoall43510% (1)

- 4 HR 5 EMA SystemDocumento10 pagine4 HR 5 EMA SystemBaljeet Singh100% (1)

- Paper - 4: Taxation Section A: Income Tax Law Part - II: Receipts PaymentsDocumento29 paginePaper - 4: Taxation Section A: Income Tax Law Part - II: Receipts PaymentsVaishnavi ShindeNessuna valutazione finora

- FABM 2 - Lesson1 5Documento78 pagineFABM 2 - Lesson1 5Sis HopNessuna valutazione finora

- Illustrations AmalgamationDocumento4 pagineIllustrations Amalgamationajay2741100% (1)

- MODULE 1 Variable and Absorption CostingDocumento9 pagineMODULE 1 Variable and Absorption Costingjerico garciaNessuna valutazione finora

- Mary Anne C. Bantog: ObjectiveDocumento4 pagineMary Anne C. Bantog: ObjectiveUWatch TVNessuna valutazione finora

- Preliminary Topic Five - Financial MarketsDocumento12 paginePreliminary Topic Five - Financial MarketsBaro LeeNessuna valutazione finora

- How To Know Fraud in AdvanceDocumento6 pagineHow To Know Fraud in AdvanceMd AzimNessuna valutazione finora

- Tax Review Dimaampao Midterms SamplexDocumento14 pagineTax Review Dimaampao Midterms Samplexdenbar15100% (4)

- Quiz 2 Problem - SolutionDocumento9 pagineQuiz 2 Problem - SolutionCharice Anne VillamarinNessuna valutazione finora

- Kishore KumarDocumento4 pagineKishore KumarRakesh GowdaNessuna valutazione finora

- Tugas Fia Pertemuan 6 - Ester Sabatini - 8312419007Documento2 pagineTugas Fia Pertemuan 6 - Ester Sabatini - 8312419007Ester SabatiniNessuna valutazione finora

- GM 19Documento3 pagineGM 19Bhavdeep singh sidhuNessuna valutazione finora

- Abakada Guro Party List Vs ErmitaDocumento3 pagineAbakada Guro Party List Vs ErmitakitakatttNessuna valutazione finora

- 1smied Vs CirDocumento2 pagine1smied Vs CirBam BathanNessuna valutazione finora

- Analysis of HCLDocumento34 pagineAnalysis of HCLRidhima KalraNessuna valutazione finora