Potrebbero piacerti anche

- Mobile Payments - Go-To-Market StrategyDocumento7 pagineMobile Payments - Go-To-Market StrategyRachit KulshresthaNessuna valutazione finora

- B SDocumento36 pagineB SkeithguruNessuna valutazione finora

- Corporate - Strategy - Food PandaDocumento4 pagineCorporate - Strategy - Food PandaAmna NoorNessuna valutazione finora

- P&G Japan: The SK-II GlobalizationDocumento12 pagineP&G Japan: The SK-II Globalizationfawad_hussain_293% (14)

- Discussion 1Documento3 pagineDiscussion 1Gynessa Therewillbenoother WoodardNessuna valutazione finora

- Group Assignment Movie Review Chapter 1: Code of Ethics For AuditorsDocumento6 pagineGroup Assignment Movie Review Chapter 1: Code of Ethics For AuditorsDaud Farook IINessuna valutazione finora

- Open Compensation Plan A Complete Guide - 2020 EditionDa EverandOpen Compensation Plan A Complete Guide - 2020 EditionNessuna valutazione finora

- Types of Stamps and Some Concepts of Stamp DutyDocumento5 pagineTypes of Stamps and Some Concepts of Stamp DutyNikhil Kasat100% (3)

- Marketing Strategy of Maggi: A Case StudyDocumento96 pagineMarketing Strategy of Maggi: A Case Studyfazeelath90% (51)

- 6Ps Brand Growth Model One PagerDocumento2 pagine6Ps Brand Growth Model One PagerArun S Bharadwaj80% (5)

- Scope of FMCG Sector in Rural IndiaDocumento37 pagineScope of FMCG Sector in Rural IndiaGunjangupta550% (2)

- Smartphones - A Microeconomic AnalysisDocumento27 pagineSmartphones - A Microeconomic AnalysisIshan ShahNessuna valutazione finora

- Qualities of A TrainerDocumento8 pagineQualities of A TrainerKommineni Ravie KumarNessuna valutazione finora

- LearnMedix - ContentDocumento6 pagineLearnMedix - ContentOur PastNessuna valutazione finora

- Organizational Effectiveness and PerformanceDocumento5 pagineOrganizational Effectiveness and PerformanceDung, DoanNessuna valutazione finora

- The Multi-Task, Multi-Intelligent Teacher - by Eugenia Papaioannou - 30.12.2017Documento2 pagineThe Multi-Task, Multi-Intelligent Teacher - by Eugenia Papaioannou - 30.12.2017Eugenia Papaioannou100% (1)

- Computer Assisted Instruction For Patient EducationDocumento9 pagineComputer Assisted Instruction For Patient EducationCorrine IvyNessuna valutazione finora

- Curriculum Planning & DevelopmentDocumento13 pagineCurriculum Planning & DevelopmentMark Madridano100% (1)

- Managerial Grid Model of LeadershipDocumento6 pagineManagerial Grid Model of LeadershipVirusdhakaNessuna valutazione finora

- Chapter 1. What Is Action Research?Documento9 pagineChapter 1. What Is Action Research?Lea Alyana CapatiNessuna valutazione finora

- Group DynamicsDocumento5 pagineGroup DynamicsJiten DasNessuna valutazione finora

- Reliablity Validity of Research Tools 1Documento19 pagineReliablity Validity of Research Tools 1Free Escort Service100% (1)

- Workshop, Exibition - Programmed InstructionDocumento22 pagineWorkshop, Exibition - Programmed InstructionSudharani B BanappagoudarNessuna valutazione finora

- Training of Trainers Manual-2Documento82 pagineTraining of Trainers Manual-2sethasarakmonyNessuna valutazione finora

- Nursing ProcessDocumento5 pagineNursing ProcessStacy CamposNessuna valutazione finora

- Educational Media in Teaching Learning ProcessDocumento8 pagineEducational Media in Teaching Learning ProcessRatih AsmaraNessuna valutazione finora

- PGPM-19-20-T4-Managing Personal Investments-Prof. B. VenkateshDocumento8 paginePGPM-19-20-T4-Managing Personal Investments-Prof. B. VenkateshSiddharth GuptaNessuna valutazione finora

- Non-Parametric TestDocumento2 pagineNon-Parametric Testutcm77Nessuna valutazione finora

- Centralized Organizations Have Some AdvantagesDocumento15 pagineCentralized Organizations Have Some AdvantagesDengAwutNessuna valutazione finora

- Budgeting in Health Care System in IndiaDocumento16 pagineBudgeting in Health Care System in IndiaABINASHNessuna valutazione finora

- Strategies, Policies & Planning PremisesDocumento16 pagineStrategies, Policies & Planning PremisesKajal MakwanaNessuna valutazione finora

- MangementDocumento21 pagineMangementshubham rathodNessuna valutazione finora

- CCE Grading SystemDocumento4 pagineCCE Grading SystemnavinkapilNessuna valutazione finora

- Objectives of Distance EducationDocumento2 pagineObjectives of Distance EducationLing Siew EeNessuna valutazione finora

- Course Outline-SWOT AnalysisDocumento2 pagineCourse Outline-SWOT AnalysisraiyanduNessuna valutazione finora

- Overview of Plans - PPTX NewDocumento47 pagineOverview of Plans - PPTX NewNaman BajajNessuna valutazione finora

- Management by Objectives & Role Play: Presented By: Mridul AggarwalDocumento16 pagineManagement by Objectives & Role Play: Presented By: Mridul Aggarwaladihind100% (1)

- Management by Objectives (Mbo) : by Alzira Xavier Assistant Professor Assistant TPODocumento23 pagineManagement by Objectives (Mbo) : by Alzira Xavier Assistant Professor Assistant TPORicha DivkarNessuna valutazione finora

- Task 3Documento3 pagineTask 3Fleur De Liz Jagolino100% (1)

- Model of Curriculum DevelopmentDocumento15 pagineModel of Curriculum DevelopmentSupriya chhetryNessuna valutazione finora

- Teacher's Guide For IMNCI Training of Students-441Documento121 pagineTeacher's Guide For IMNCI Training of Students-441National Child Health Resource Centre (NCHRC)Nessuna valutazione finora

- Simulation PDFDocumento4 pagineSimulation PDFGitamoni BoroNessuna valutazione finora

- Questionnaire & InterviewsDocumento26 pagineQuestionnaire & InterviewszedNessuna valutazione finora

- Memo For Media Evaluation RubricDocumento3 pagineMemo For Media Evaluation Rubricnisev2003Nessuna valutazione finora

- Assessment of Attitudes and Communication SkillsDocumento19 pagineAssessment of Attitudes and Communication SkillsDissa Naratania HantraNessuna valutazione finora

- Tribune - Marketing PlanDocumento16 pagineTribune - Marketing PlanPalmodiNessuna valutazione finora

- College Administration PresentationDocumento79 pagineCollege Administration PresentationWendimagen Meshesha Fanta100% (1)

- Normal Probability DistributionDocumento13 pagineNormal Probability DistributionPratikshya SahooNessuna valutazione finora

- Distance Education PDFDocumento250 pagineDistance Education PDFsyamtripathy1Nessuna valutazione finora

- Cronbach - S AlphaDocumento3 pagineCronbach - S AlphaEllen Mae Causing DelfinNessuna valutazione finora

- OumDocumento4 pagineOumMdm CT NurulNessuna valutazione finora

- Community Based Management Information SystemDocumento12 pagineCommunity Based Management Information SystemTee SiNessuna valutazione finora

- Assignment 1 - Marketing ManagementDocumento9 pagineAssignment 1 - Marketing Managementwidi tigustiNessuna valutazione finora

- Educational ObjectivesDocumento20 pagineEducational ObjectivesSadiq Merchant100% (1)

- 1.recruitment SelectionDocumento46 pagine1.recruitment Selectionbetcy georgeNessuna valutazione finora

- Foriegn Collabration TypesDocumento9 pagineForiegn Collabration TypesKarmjit KaurNessuna valutazione finora

- CBTPDocumento30 pagineCBTPDaroo D.TNessuna valutazione finora

- Types of Lecture MethodsDocumento30 pagineTypes of Lecture MethodsAdnan KhattakNessuna valutazione finora

- B Ed. Semester SystemDocumento33 pagineB Ed. Semester SystemShoaib YounisNessuna valutazione finora

- The Definition of Syllabus and Grading SystemDocumento16 pagineThe Definition of Syllabus and Grading SystemGesia Wulandari100% (1)

- PHD Regulations 2011Documento8 paginePHD Regulations 2011karthipriyaNessuna valutazione finora

- Micro Teaching and Its NeedDocumento15 pagineMicro Teaching and Its NeedEvelyn100% (2)

- 683 1683 1 PBDocumento8 pagine683 1683 1 PBSubhas RoyNessuna valutazione finora

- 1-The Nature and Scope of EconomicsDocumento28 pagine1-The Nature and Scope of EconomicsHassan AliNessuna valutazione finora

- Planning CycleDocumento25 paginePlanning CycleJennifer OestarNessuna valutazione finora

- Career Planning: Minu Mathew Neeraj VijayDocumento14 pagineCareer Planning: Minu Mathew Neeraj Vijayminuannapoovelil7642Nessuna valutazione finora

- Administering, Analyzing, and Improving TestsDocumento3 pagineAdministering, Analyzing, and Improving TestsJessa Mae Cantillo100% (1)

- T & D Notes Unit-IDocumento20 pagineT & D Notes Unit-Irohanmodgil71Nessuna valutazione finora

- MetLife Final SatishDocumento24 pagineMetLife Final SatishSatish VermaNessuna valutazione finora

- Income Declaration Scheme Rules, 2016: Form 1Documento9 pagineIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatNessuna valutazione finora

- Sale DeedDocumento5 pagineSale DeedNitin GoyalNessuna valutazione finora

- DTL Sec 10Documento14 pagineDTL Sec 10Nikhil KasatNessuna valutazione finora

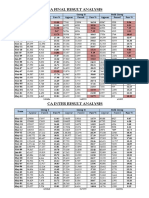

- CA Result AnalysisDocumento1 paginaCA Result AnalysisNikhil KasatNessuna valutazione finora

- Derivatives Markets in Interest Rate & Foreign Exchange RateDocumento20 pagineDerivatives Markets in Interest Rate & Foreign Exchange RatehdjfhsjfhwjfNessuna valutazione finora

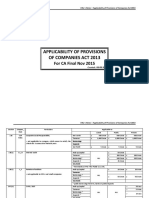

- ApplicabiliTY of ProvisionsDocumento3 pagineApplicabiliTY of ProvisionsNikhil KasatNessuna valutazione finora

- Valuation of InventoriesDocumento4 pagineValuation of InventoriesNikhil KasatNessuna valutazione finora

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Documento21 pagineSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatNessuna valutazione finora

- BLack Money RulesDocumento23 pagineBLack Money RulesLive LawNessuna valutazione finora

- Banca SuranceDocumento32 pagineBanca SuranceNikhil KasatNessuna valutazione finora

- Black Money BillDocumento30 pagineBlack Money BillNikhil KasatNessuna valutazione finora

- Hedging With Financial DerivativesDocumento30 pagineHedging With Financial DerivativesNikhil KasatNessuna valutazione finora

- Delhi Dvat Registration InformationDocumento4 pagineDelhi Dvat Registration InformationNikhil KasatNessuna valutazione finora

- CA Final Writing Professional Ethics AnswersDocumento2 pagineCA Final Writing Professional Ethics AnswersNikhil KasatNessuna valutazione finora

- Fees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratDocumento10 pagineFees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratNikhil KasatNessuna valutazione finora

- Directors Report As Per StatusDocumento5 pagineDirectors Report As Per StatusNikhil KasatNessuna valutazione finora

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDocumento9 pagineAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatNessuna valutazione finora

- Tds On SalariesDocumento55 pagineTds On SalariespunitNessuna valutazione finora

- Web Base Timesheet ApplicationDocumento4 pagineWeb Base Timesheet ApplicationNikhil KasatNessuna valutazione finora

- List of Indian As Convergence With IfrsDocumento1 paginaList of Indian As Convergence With IfrsNikhil KasatNessuna valutazione finora

- Anf 4dDocumento3 pagineAnf 4dNikhil KasatNessuna valutazione finora

- Ind As 2015Documento2 pagineInd As 2015Nikhil KasatNessuna valutazione finora

- Cusoms Valuation MaterialDocumento8 pagineCusoms Valuation MaterialNikhil KasatNessuna valutazione finora

- August Month CompliancesDocumento1 paginaAugust Month CompliancesNikhil KasatNessuna valutazione finora

- Curriculum VitaeDocumento13 pagineCurriculum VitaeNikhil KasatNessuna valutazione finora

- Privileges To Small CompaniesDocumento2 paginePrivileges To Small CompaniesNikhil KasatNessuna valutazione finora

- Importance of ArticleshipDocumento6 pagineImportance of ArticleshipNikhil KasatNessuna valutazione finora

- C01Documento23 pagineC01Silvery DoeNessuna valutazione finora

- Euromonitor - Leveraging Product Claims To Build A Successful Brand Strategy - wpProductClaimsDocumento15 pagineEuromonitor - Leveraging Product Claims To Build A Successful Brand Strategy - wpProductClaimsjfmansillagNessuna valutazione finora

- Objective Broad ObjectiveDocumento29 pagineObjective Broad ObjectiveTouhidur RahmanNessuna valutazione finora

- Project PDFDocumento63 pagineProject PDFAtheesha M VenuNessuna valutazione finora

- Mark30063 Product-Mgt ImDocumento48 pagineMark30063 Product-Mgt ImJayson MeperaqueNessuna valutazione finora

- Bc07 - Team 3 - Case Ufll 2015Documento21 pagineBc07 - Team 3 - Case Ufll 2015Nguyễn Hoàng NamNessuna valutazione finora

- Products and PricingDocumento9 pagineProducts and PricingBernice SaminaNessuna valutazione finora

- Divisio N Revenue Profit EFE Scores IFE ScoresDocumento3 pagineDivisio N Revenue Profit EFE Scores IFE ScoresCresenciano MalabuyocNessuna valutazione finora

- Case Study#1 (Tata Sky)Documento9 pagineCase Study#1 (Tata Sky)Ananta MallikNessuna valutazione finora

- Literature Review On Marketing Mix StrategyDocumento7 pagineLiterature Review On Marketing Mix Strategyamjatzukg100% (2)

- Noble & Gruca MKSC 1999Documento22 pagineNoble & Gruca MKSC 1999Amanda RoseroNessuna valutazione finora

- Amazon Strategic Plan 2023-2025Documento29 pagineAmazon Strategic Plan 2023-2025ELECTRIC EGYPT100% (3)

- Marketing Analytics - S1Documento23 pagineMarketing Analytics - S1Nistala YashikaNessuna valutazione finora

- Summary of Business Strategy Application Level Interactive Questions With Immediate AnswerDocumento118 pagineSummary of Business Strategy Application Level Interactive Questions With Immediate AnswerIQBAL MAHMUDNessuna valutazione finora

- BCG and GE Analysis On Idea CellularDocumento14 pagineBCG and GE Analysis On Idea CellularMaverick_raj83% (6)

- Paper:: 14 Marketing Management 35, Pricing: Methods and StrategiesDocumento9 paginePaper:: 14 Marketing Management 35, Pricing: Methods and StrategiesstudentNessuna valutazione finora

- The LEGO Group - CaseDocumento6 pagineThe LEGO Group - CaseVijay KoushalNessuna valutazione finora

- Marketing Management Project: Chew Till Your Heart DesiresDocumento28 pagineMarketing Management Project: Chew Till Your Heart DesiresIONITA GABRIELNessuna valutazione finora

- Samsung SwotDocumento30 pagineSamsung Swotsahil pednekarNessuna valutazione finora

- Project Manager SeriesDocumento8 pagineProject Manager SeriesAyushi MehtaNessuna valutazione finora

- Case Study II - RoffDocumento3 pagineCase Study II - RoffNikhil MaheshwariNessuna valutazione finora

- Dynamic BUsiness EnvironmentDocumento16 pagineDynamic BUsiness EnvironmentHibernation PetersonNessuna valutazione finora

- Revlon Case Study AnalysisDocumento7 pagineRevlon Case Study AnalysisBilal ZuberiNessuna valutazione finora