Potrebbero piacerti anche

- Guidance To Prepare WPS-PQR For WeldingDocumento1 paginaGuidance To Prepare WPS-PQR For WeldingSaran Kumar83% (6)

- Accounting For Manufacturing BusinessDocumento56 pagineAccounting For Manufacturing Businessrajahmati_2890% (20)

- Partnership: (Definition, Nature, Formation) Lucille Myschkin Flores, MBADocumento38 paginePartnership: (Definition, Nature, Formation) Lucille Myschkin Flores, MBAYbonne BatleNessuna valutazione finora

- Accounting For Corporation Share CapitalDocumento54 pagineAccounting For Corporation Share CapitalZephaniah Reign GonzalesNessuna valutazione finora

- WWW - Mcnp.edu - PH Adminoffice@mcnp - Edu.ph: International School of Asia and The PacificDocumento14 pagineWWW - Mcnp.edu - PH Adminoffice@mcnp - Edu.ph: International School of Asia and The PacificKing Ezekiah VergaraNessuna valutazione finora

- Accounting For Partnerships 2Documento35 pagineAccounting For Partnerships 2Lazarus Henga100% (1)

- Cash and Cash EquivalentsDocumento16 pagineCash and Cash Equivalentsspur iousNessuna valutazione finora

- Recipe Book and Autobiography by Colonel Harland SandersDocumento184 pagineRecipe Book and Autobiography by Colonel Harland SandersAdam Buchnowski100% (3)

- Tanker BodyDocumento5 pagineTanker BodyAghil BuddyNessuna valutazione finora

- Accounting For InventoriesDocumento58 pagineAccounting For InventoriesMarriel Fate CullanoNessuna valutazione finora

- Property Plant and EquipmentDocumento13 pagineProperty Plant and EquipmentWilsonNessuna valutazione finora

- Deferred Tax Lecture SlidesDocumento38 pagineDeferred Tax Lecture Slidesmd salehinNessuna valutazione finora

- PFRS 15Documento4 paginePFRS 15Annie JuliaNessuna valutazione finora

- INTERMEDIATEACCOUNTINGIIDocumento154 pagineINTERMEDIATEACCOUNTINGIINita Costillas De MattaNessuna valutazione finora

- Difference Between GAAP and IFRSDocumento3 pagineDifference Between GAAP and IFRSGoutam SoniNessuna valutazione finora

- Accounting For ReceivablesDocumento23 pagineAccounting For ReceivablesFelekePhiliphosNessuna valutazione finora

- Pfrs 2 Share-Based PaymentsDocumento3 paginePfrs 2 Share-Based PaymentsR.A.Nessuna valutazione finora

- Talent ManagementDocumento40 pagineTalent ManagementPratibha Goswami100% (1)

- Lean101 Train The Trainer Slides tcm36-68577Documento66 pagineLean101 Train The Trainer Slides tcm36-68577zakari100% (1)

- Chapter 10 Answers: Lojero, Princess Glaidine C. Coa BLK 1C Conceptual Framework Accounting Standards (Ae 102)Documento20 pagineChapter 10 Answers: Lojero, Princess Glaidine C. Coa BLK 1C Conceptual Framework Accounting Standards (Ae 102)glaide lojeroNessuna valutazione finora

- Jabfloor JabliteDocumento10 pagineJabfloor JabliteAshik ShahNessuna valutazione finora

- IAS 16 Property Plant EquipmentDocumento4 pagineIAS 16 Property Plant EquipmentMD Hafizul Islam HafizNessuna valutazione finora

- Pas 24 Related Party DisclosureDocumento3 paginePas 24 Related Party DisclosureR.A.Nessuna valutazione finora

- 13 Current LiabilitiesDocumento37 pagine13 Current LiabilitiesJoseph P. McDeejoz100% (1)

- Chapter 6 Property, Plant and EquipmentDocumento13 pagineChapter 6 Property, Plant and EquipmentKrissa Mae Longos100% (1)

- GEMSS-M-35 Rev 01 Painting & Coating Protection SystemDocumento11 pagineGEMSS-M-35 Rev 01 Painting & Coating Protection SystemAzhar AliNessuna valutazione finora

- Injection MouldingDocumento23 pagineInjection MouldingPrathmeshBhokari100% (1)

- Accounting For DerivativesDocumento8 pagineAccounting For DerivativesPrateek PatelNessuna valutazione finora

- Pas 26 Accounting and Reporting by Retirement Benefit PlansDocumento2 paginePas 26 Accounting and Reporting by Retirement Benefit PlansR.A.Nessuna valutazione finora

- Proceedings English Complete - RevBDocumento217 pagineProceedings English Complete - RevBFran Jimenez100% (1)

- Aud Prob Part 1Documento106 pagineAud Prob Part 1Ma. Hazel Donita DiazNessuna valutazione finora

- Pas 32Documento34 paginePas 32Iris SarigumbaNessuna valutazione finora

- Financial Instruments: PAS 32 and PFRS 9Documento116 pagineFinancial Instruments: PAS 32 and PFRS 9Anna WilliamsNessuna valutazione finora

- #16 Investment PropertyDocumento4 pagine#16 Investment PropertyClaudine DuhapaNessuna valutazione finora

- Toa Interim ReportingDocumento17 pagineToa Interim ReportingSam100% (1)

- Module 3 - Events After The Reporting Period PDFDocumento7 pagineModule 3 - Events After The Reporting Period PDFCaroline Bagsik100% (1)

- Kaizen Lean Management Service Sector2Documento22 pagineKaizen Lean Management Service Sector2Mahathir FansuriNessuna valutazione finora

- Pfrs 16 LeasesDocumento4 paginePfrs 16 LeasesR.A.Nessuna valutazione finora

- Accntg4 Non-Current Assets Held For Sale and Discontinued Operations NewDocumento32 pagineAccntg4 Non-Current Assets Held For Sale and Discontinued Operations NewALYSSA MAE ABAAGNessuna valutazione finora

- Chapter 13 Property Plant and Equipment Depreciation and deDocumento21 pagineChapter 13 Property Plant and Equipment Depreciation and deEarl Lalaine EscolNessuna valutazione finora

- Ifrs 16 LeasesDocumento19 pagineIfrs 16 LeasesR SharmaNessuna valutazione finora

- Toa - Preboard - May 2016Documento11 pagineToa - Preboard - May 2016Kenneth Bryan Tegerero Tegio100% (1)

- Principles of Accounting Chapter 13Documento43 paginePrinciples of Accounting Chapter 13myrentistoodamnhigh100% (1)

- Activities - Cash Payments To Acquire PropertyDocumento2 pagineActivities - Cash Payments To Acquire PropertyPrecious ViterboNessuna valutazione finora

- CM1 PAS1 Presentation of Financial StatementsDocumento16 pagineCM1 PAS1 Presentation of Financial StatementsMark GerwinNessuna valutazione finora

- Corporation QuizDocumento13 pagineCorporation Quizjano_art21Nessuna valutazione finora

- Book Value Per ShareDocumento18 pagineBook Value Per ShareRechelleNessuna valutazione finora

- Article 1804Documento1 paginaArticle 1804Christine ChuaunsuNessuna valutazione finora

- Impairment of AssetsDocumento19 pagineImpairment of AssetsTareq SojolNessuna valutazione finora

- Premiums and WarrantiesDocumento17 paginePremiums and WarrantiesKaye Choraine NadumaNessuna valutazione finora

- 41 DepletionDocumento5 pagine41 DepletionjsemlpzNessuna valutazione finora

- Partnership Formation and Operation (Better)Documento44 paginePartnership Formation and Operation (Better)Camille Salvador100% (1)

- Events After The Reporting Period Final 6 KiloDocumento13 pagineEvents After The Reporting Period Final 6 Kilonati100% (1)

- RetainedDocumento66 pagineRetainedJhonalyn Montimor GaldonesNessuna valutazione finora

- IA 3 Single EntryDocumento26 pagineIA 3 Single EntryIvy RosalesNessuna valutazione finora

- Ias 24 Related Party DisclosuresDocumento3 pagineIas 24 Related Party DisclosurescaarunjiNessuna valutazione finora

- Investments in Associates: Rowena Buan-Yost, CPA-MBADocumento21 pagineInvestments in Associates: Rowena Buan-Yost, CPA-MBARowenaBuan-YostNessuna valutazione finora

- Chapter 14 - Pas 16 Property, Plant and Equipment: Measurement After RecognitionDocumento5 pagineChapter 14 - Pas 16 Property, Plant and Equipment: Measurement After RecognitionVince PeredaNessuna valutazione finora

- Financialaccounting 3 Theories Summary ValixDocumento10 pagineFinancialaccounting 3 Theories Summary ValixDarwin Competente LagranNessuna valutazione finora

- Trade Receivable & AllowancesDocumento7 pagineTrade Receivable & Allowancesmobylay0% (1)

- Final Reviewer in RFLIBDocumento14 pagineFinal Reviewer in RFLIBMichelle EsternonNessuna valutazione finora

- Investment in Securities (Notes)Documento5 pagineInvestment in Securities (Notes)Karla BordonesNessuna valutazione finora

- Related Party Disclosures - AS 18Documento18 pagineRelated Party Disclosures - AS 18B.S KumarNessuna valutazione finora

- Book Value and Earnings Per ShareDocumento3 pagineBook Value and Earnings Per ShareAlejandrea LalataNessuna valutazione finora

- Ias 24 Related Party Disclosure PDFDocumento5 pagineIas 24 Related Party Disclosure PDFsimply PrettyNessuna valutazione finora

- Final Tfa CompiledDocumento109 pagineFinal Tfa CompiledAsi Cas JavNessuna valutazione finora

- Home Quiz Partnership AccountingDocumento3 pagineHome Quiz Partnership AccountingKeith Anthony AmorNessuna valutazione finora

- Financial Accounting and Reporting - Volume 1A PDFDocumento61 pagineFinancial Accounting and Reporting - Volume 1A PDFKharen Valdez100% (1)

- 2 - FSA1 Handout (Topic 4 Reading 25, 28) - InventoryDocumento51 pagine2 - FSA1 Handout (Topic 4 Reading 25, 28) - InventoryGuyu PanNessuna valutazione finora

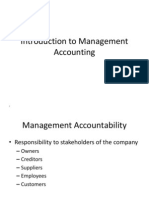

- Introduction To Management AccountingDocumento34 pagineIntroduction To Management AccountingriyakalpetaNessuna valutazione finora

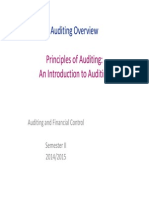

- Curs 4 AuditDocumento33 pagineCurs 4 AuditcociorvanmiriamNessuna valutazione finora

- Czech RepublicDocumento7 pagineCzech RepubliccociorvanmiriamNessuna valutazione finora

- Semivariance MacrosDocumento1 paginaSemivariance MacroscociorvanmiriamNessuna valutazione finora

- Portofolio Management - From SimonaDocumento14 paginePortofolio Management - From SimonacociorvanmiriamNessuna valutazione finora

- ReportDocumento314 pagineReportOnel FlorianNessuna valutazione finora

- Ex Portfolio StructureDocumento11 pagineEx Portfolio StructurecociorvanmiriamNessuna valutazione finora

- Audit Curs 1Documento42 pagineAudit Curs 1cociorvanmiriam100% (1)

- Curs 7 AuditDocumento35 pagineCurs 7 AuditcociorvanmiriamNessuna valutazione finora

- Curs 5 AuditDocumento18 pagineCurs 5 AuditcociorvanmiriamNessuna valutazione finora

- Audit Curs 3Documento50 pagineAudit Curs 3cociorvanmiriamNessuna valutazione finora

- Audit Curs 1Documento42 pagineAudit Curs 1cociorvanmiriam100% (1)

- Avon and OriflameDocumento17 pagineAvon and OriflamecociorvanmiriamNessuna valutazione finora

- Curs 6 AuditDocumento23 pagineCurs 6 Auditcociorvanmiriam100% (1)

- Audit Curs 2Documento31 pagineAudit Curs 2cociorvanmiriamNessuna valutazione finora

- Principles of Credit Risk ManagementDocumento2 paginePrinciples of Credit Risk ManagementcociorvanmiriamNessuna valutazione finora

- Italy Vs Uk Tax ComplianceDocumento7 pagineItaly Vs Uk Tax CompliancecociorvanmiriamNessuna valutazione finora

- A Good Practice Guide To Co-Operation Between External and Internal AuditorsDocumento47 pagineA Good Practice Guide To Co-Operation Between External and Internal AuditorscociorvanmiriamNessuna valutazione finora

- US GAAP Vs IFRSDocumento52 pagineUS GAAP Vs IFRSSumair ShahidNessuna valutazione finora

- Romanian Malpractice CaseDocumento2 pagineRomanian Malpractice CasecociorvanmiriamNessuna valutazione finora

- 2013-2014 Worldwide Personal Tax GuideDocumento1.399 pagine2013-2014 Worldwide Personal Tax GuideTony GallacherNessuna valutazione finora

- Tehnici Curs 4 Intubatia OrotrahealaDocumento5 pagineTehnici Curs 4 Intubatia OrotrahealacociorvanmiriamNessuna valutazione finora

- Teme Lucrari de Licenta in Lb. Engleza 2014-2015Documento2 pagineTeme Lucrari de Licenta in Lb. Engleza 2014-2015cociorvanmiriamNessuna valutazione finora

- LinksDocumento1 paginaLinkscociorvanmiriamNessuna valutazione finora

- Banking System of EnglandDocumento11 pagineBanking System of EnglandcociorvanmiriamNessuna valutazione finora

- Romanian Banking SystemDocumento11 pagineRomanian Banking SystemcociorvanmiriamNessuna valutazione finora

- Financial AccountingDocumento20 pagineFinancial AccountingcociorvanmiriamNessuna valutazione finora

- Share-Capital AccountingDocumento18 pagineShare-Capital AccountingcociorvanmiriamNessuna valutazione finora

- Statistics 1st YearDocumento6 pagineStatistics 1st YearcociorvanmiriamNessuna valutazione finora

- Industrial Engineering PresentationDocumento13 pagineIndustrial Engineering PresentationKent RodriguezNessuna valutazione finora

- Influence of Surface Finish On Cavitation ErosionDocumento9 pagineInfluence of Surface Finish On Cavitation ErosionJason BarrentineNessuna valutazione finora

- Marketing IndividualDocumento2 pagineMarketing Individualsinyi0Nessuna valutazione finora

- Chapter 8 - Heat TreatmentDocumento20 pagineChapter 8 - Heat TreatmentISANessuna valutazione finora

- Bronze Castings For Bridges and TurntablesDocumento5 pagineBronze Castings For Bridges and Turntablesnicu1212Nessuna valutazione finora

- Supply Chain Evolution - Theory, Concepts and ScienceDocumento25 pagineSupply Chain Evolution - Theory, Concepts and ScienceAhmed AmrNessuna valutazione finora

- Problem Set I For International Trade # Partial Solutions ... - CER-ETH PDFDocumento14 pagineProblem Set I For International Trade # Partial Solutions ... - CER-ETH PDFJGNessuna valutazione finora

- GER 3569G Advanced Gas Turbine Materials and Coatings PDFDocumento30 pagineGER 3569G Advanced Gas Turbine Materials and Coatings PDFcheche640% (1)

- MIM DesignGuideDocumento28 pagineMIM DesignGuideSubhojit SamontaNessuna valutazione finora

- PomDocumento3 paginePomNadine Clare FloresNessuna valutazione finora

- Rolling ProcessDocumento17 pagineRolling ProcessRavichandran GNessuna valutazione finora

- M S Ramaiah Institute of Technology Department of CIVIL ENGINEERINGDocumento10 pagineM S Ramaiah Institute of Technology Department of CIVIL ENGINEERINGPrashant SunagarNessuna valutazione finora

- Cybermedia Research India Vlsi Design Services Study 2012 RevealsDocumento4 pagineCybermedia Research India Vlsi Design Services Study 2012 Revealsrajt123Nessuna valutazione finora

- By: Loy Lobo Aapa Angchekar Priyanka BendaleDocumento45 pagineBy: Loy Lobo Aapa Angchekar Priyanka BendaleLoy LoboNessuna valutazione finora

- Aeg Lavamat l64850l - Manual 071013Documento36 pagineAeg Lavamat l64850l - Manual 071013Sakthipriya JeganathanNessuna valutazione finora

- Consumption of Formalin in Industries of PakistanDocumento2 pagineConsumption of Formalin in Industries of PakistanAzfer HayatNessuna valutazione finora

- Double Deck Bus Body Structure and Driver's Cab DesignDocumento28 pagineDouble Deck Bus Body Structure and Driver's Cab DesignBambang Setyo UtomoNessuna valutazione finora

- 2008 AACEi TransactionsDocumento6 pagine2008 AACEi TransactionsAnonymous 19hUyemNessuna valutazione finora

- SCMDocumento46 pagineSCMankita merchantNessuna valutazione finora

- WalmartDocumento3 pagineWalmartanissaNessuna valutazione finora

- Section 13Documento21 pagineSection 13HAFIZ IMRAN AKHTERNessuna valutazione finora