Potrebbero piacerti anche

- Thailand: Industrialization and Economic Catch-UpDa EverandThailand: Industrialization and Economic Catch-UpNessuna valutazione finora

- Business Environment and Policy: Dr. V L Rao Professor Dr. Radha Raghuramapatruni Assistant ProfessorDocumento41 pagineBusiness Environment and Policy: Dr. V L Rao Professor Dr. Radha Raghuramapatruni Assistant ProfessorRajeshwari RosyNessuna valutazione finora

- Case Study Group1 (Final)Documento19 pagineCase Study Group1 (Final)hina abbasNessuna valutazione finora

- ChinaDocumento17 pagineChinasn07860Nessuna valutazione finora

- Indian Service SectorDocumento34 pagineIndian Service Sectorpinku_thakkar0% (1)

- Technical and Vocational Education and Training in the Philippines in the Age of Industry 4.0Da EverandTechnical and Vocational Education and Training in the Philippines in the Age of Industry 4.0Nessuna valutazione finora

- Rama Velamuri: More On EntrepreneurshipDocumento15 pagineRama Velamuri: More On EntrepreneurshipNational Press FoundationNessuna valutazione finora

- MTICDocumento17 pagineMTICshanky22Nessuna valutazione finora

- SynthesisDocumento52 pagineSynthesisKaye GarciaNessuna valutazione finora

- Infosys vs. TcsDocumento30 pagineInfosys vs. TcsRohit KumarNessuna valutazione finora

- Caim 99Documento71 pagineCaim 99darbha91Nessuna valutazione finora

- Macro Session 1Documento56 pagineMacro Session 1Susmriti ShresthaNessuna valutazione finora

- Part 4 LaborDocumento8 paginePart 4 LaborAtty MglrtNessuna valutazione finora

- Social Change 1.0Documento6 pagineSocial Change 1.0Mohd NazrinNessuna valutazione finora

- Challenges in Creation of New Jobs in GlobalisationDocumento4 pagineChallenges in Creation of New Jobs in Globalisationspandana chowdaryNessuna valutazione finora

- Economy of Singapore-WikipediaDocumento11 pagineEconomy of Singapore-WikipediaJosé Manuel NavarroNessuna valutazione finora

- Sri Lanka: Fostering Workforce Skills through EducationDa EverandSri Lanka: Fostering Workforce Skills through EducationNessuna valutazione finora

- Mapping Property Tax Reform in Southeast AsiaDa EverandMapping Property Tax Reform in Southeast AsiaNessuna valutazione finora

- Tapping Technology to Maximize the Longevity Dividend in AsiaDa EverandTapping Technology to Maximize the Longevity Dividend in AsiaNessuna valutazione finora

- Dismantling The American Dream: How Multinational Corporations Undermine American ProsperityDocumento33 pagineDismantling The American Dream: How Multinational Corporations Undermine American ProsperityCharlene KronstedtNessuna valutazione finora

- Impact of Globalization On Indian EconomyDocumento33 pagineImpact of Globalization On Indian EconomySrikanth ReddyNessuna valutazione finora

- Research Paper of DR Fernando Aldaba (As of 21 May)Documento37 pagineResearch Paper of DR Fernando Aldaba (As of 21 May)meagon_cjNessuna valutazione finora

- GM AssignmentDocumento26 pagineGM AssignmentLong TrầnNessuna valutazione finora

- Tcs v. InfosysDocumento40 pagineTcs v. Infosysneetapai3859Nessuna valutazione finora

- Anna Catharina - Assignment 1Documento6 pagineAnna Catharina - Assignment 1Anna GreeffNessuna valutazione finora

- MC 4GoalsDocDocumento4 pagineMC 4GoalsDocmmagidimisa3129Nessuna valutazione finora

- PWC India em Outlook 2011 081211Documento152 paginePWC India em Outlook 2011 081211Chetan SagarNessuna valutazione finora

- Tsecoman Team 2 Carillo Raflores Lagdameo VariasDocumento24 pagineTsecoman Team 2 Carillo Raflores Lagdameo VariasGausty NituNessuna valutazione finora

- MM 2-Assingment (DENESH DISSANAYAKA)Documento21 pagineMM 2-Assingment (DENESH DISSANAYAKA)Dinesh DhammikaNessuna valutazione finora

- September 2012Documento60 pagineSeptember 2012princelyprinceNessuna valutazione finora

- IPP 2014 Appendix 1 Sectoral AnalysesDocumento63 pagineIPP 2014 Appendix 1 Sectoral AnalysesRose Ann AguilarNessuna valutazione finora

- 7aad - Shadow-of-Chinese-Dragon-on-IndiaDocumento84 pagine7aad - Shadow-of-Chinese-Dragon-on-India7aadkhanNessuna valutazione finora

- Year GDPDocumento9 pagineYear GDPishwaryaNessuna valutazione finora

- Content Group-2 Economic ProductivityDocumento8 pagineContent Group-2 Economic ProductivityLê Phương LinhNessuna valutazione finora

- Tales from the Development Frontier: How China and Other Countries Harness Light Manufacturing to Create Jobs and ProsperityDa EverandTales from the Development Frontier: How China and Other Countries Harness Light Manufacturing to Create Jobs and ProsperityNessuna valutazione finora

- The Strategic Importance of The Philippine Manufacturing SectorDocumento6 pagineThe Strategic Importance of The Philippine Manufacturing SectorchialunNessuna valutazione finora

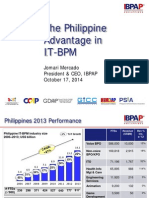

- Philippine Advantage in IT-BPMDocumento17 paginePhilippine Advantage in IT-BPMtintinchanNessuna valutazione finora

- Engg Write UpDocumento4 pagineEngg Write UpAshish PalkarNessuna valutazione finora

- Towards Higher Quality Employment in Asia (Paper)Documento22 pagineTowards Higher Quality Employment in Asia (Paper)ADB Poverty ReductionNessuna valutazione finora

- Wages Report 2011Documento321 pagineWages Report 2011Clemence TanNessuna valutazione finora

- India As Knowledge Economy1Documento19 pagineIndia As Knowledge Economy1Roshan KumarNessuna valutazione finora

- New EconomyDocumento5 pagineNew Economyyen yenNessuna valutazione finora

- IT Industry AnalysisDocumento32 pagineIT Industry AnalysisEthan ChristopherNessuna valutazione finora

- Makro 401Documento11 pagineMakro 401askerow0073Nessuna valutazione finora

- How Countries CompeteDocumento137 pagineHow Countries CompeteJim Freud100% (3)

- Advertising in ChinaDocumento34 pagineAdvertising in Chinathoreau63Nessuna valutazione finora

- Annualreport2009 10Documento132 pagineAnnualreport2009 10Abhishek KumarNessuna valutazione finora

- Chapter-3 Long Run Economic GrowthDocumento33 pagineChapter-3 Long Run Economic GrowthNishan ShettyNessuna valutazione finora

- China and India: A Comparison of Recent Economic Growth TrajectoriesDocumento33 pagineChina and India: A Comparison of Recent Economic Growth TrajectoriesSubhavya JainNessuna valutazione finora

- Week 4 Economic Growth and ProductivityDocumento27 pagineWeek 4 Economic Growth and Productivitydaisyruyu2001Nessuna valutazione finora

- Economics - Chapter 4 ManufacturingDocumento20 pagineEconomics - Chapter 4 ManufacturingBANZON, MAELYEN KAYE B.Nessuna valutazione finora

- Business To Business Marketing in India and The Asian Region. Evolution of TeDocumento19 pagineBusiness To Business Marketing in India and The Asian Region. Evolution of TesumanthdixitNessuna valutazione finora

- Philippines Electronics IndustryDocumento36 paginePhilippines Electronics IndustryelynjovergaraNessuna valutazione finora

- Consumer Durables: Market Analysis - IndiaDocumento13 pagineConsumer Durables: Market Analysis - IndiaPrantor Chakravarty100% (1)

- Tholons Whitepaper Outsourcing Multiplier 2011Documento15 pagineTholons Whitepaper Outsourcing Multiplier 2011Amana PatNessuna valutazione finora

- Nguyen Nhat Nhan - s3480570Documento22 pagineNguyen Nhat Nhan - s3480570NhanNguyenNessuna valutazione finora

- Presented By: Group 10Documento17 paginePresented By: Group 10Juhi MitraNessuna valutazione finora

- Macro Session 1Documento27 pagineMacro Session 1Susmriti ShresthaNessuna valutazione finora

- (DTQT) Chaebols in South KoreaDocumento8 pagine(DTQT) Chaebols in South Koreale ngoc tramNessuna valutazione finora

- Of Blog Post Ideas: The Ultimate ListDocumento1 paginaOf Blog Post Ideas: The Ultimate ListChandra RashaNessuna valutazione finora

- AutoCAD Beginners Guide To 2D & 3D Drawings PDFDocumento13 pagineAutoCAD Beginners Guide To 2D & 3D Drawings PDFChandra RashaNessuna valutazione finora

- 2009 National Standard Plumbing CodeDocumento332 pagine2009 National Standard Plumbing Codemelvin_parilla7774100% (1)

- Understanding SexualityDocumento382 pagineUnderstanding SexualityChandra Rasha100% (1)

- Autocad MEP 2016Documento20 pagineAutocad MEP 2016Chandra RashaNessuna valutazione finora

- Particle Board Kronospan TDSDocumento1 paginaParticle Board Kronospan TDSChandra RashaNessuna valutazione finora

- Citizen'S Charter: Republic of The Philippines City Government of Tacloban City Assessor'S OfficeDocumento18 pagineCitizen'S Charter: Republic of The Philippines City Government of Tacloban City Assessor'S OfficeChandra RashaNessuna valutazione finora

- Parc 100Documento2 pagineParc 100Chandra RashaNessuna valutazione finora

- Pioneer Marine - Epoxy Data SheetDocumento1 paginaPioneer Marine - Epoxy Data SheetChandra RashaNessuna valutazione finora

- How To Study For The Certification Examination: by Dr. Aaron RoseDocumento5 pagineHow To Study For The Certification Examination: by Dr. Aaron RoseChandra RashaNessuna valutazione finora

- UNION Door Closers: N8824BC Medium DutyDocumento2 pagineUNION Door Closers: N8824BC Medium DutyChandra RashaNessuna valutazione finora

- N8825Documento2 pagineN8825Chandra RashaNessuna valutazione finora

- Under HDMF Circular No. 310 in YearsDocumento1 paginaUnder HDMF Circular No. 310 in YearsChandra RashaNessuna valutazione finora

- Surveyors' Companion For Civil 3DDocumento247 pagineSurveyors' Companion For Civil 3DChandra RashaNessuna valutazione finora

- Date: Permit: Product Applicant .BoxDocumento3 pagineDate: Permit: Product Applicant .BoxChandra RashaNessuna valutazione finora

- Savings Interest Calculator: Savings Plan Inputs Summary of ResultsDocumento2 pagineSavings Interest Calculator: Savings Plan Inputs Summary of ResultsChandra RashaNessuna valutazione finora

- Hidden-City Ticketing The Cause and ImpactDocumento27 pagineHidden-City Ticketing The Cause and ImpactPavan KethavathNessuna valutazione finora

- Scope of Entrepreneurship Development in IndiaDocumento47 pagineScope of Entrepreneurship Development in Indiavenkata2891% (11)

- The World of Advertising and Integrated Brand PromotionDocumento24 pagineThe World of Advertising and Integrated Brand PromotionjojojojojoNessuna valutazione finora

- Module #1 E-Procurement PreparationDocumento20 pagineModule #1 E-Procurement PreparationAayush100% (1)

- Nullification Crisis and States Rights L2Documento16 pagineNullification Crisis and States Rights L2mjohnsonhistory100% (1)

- Surfcam Velocity BrochureDocumento8 pagineSurfcam Velocity BrochureLuis Chagoya ReyesNessuna valutazione finora

- Module 013 Week005-Statement of Changes in Equity, Accounting Policies, Changes in Accounting Estimates and ErrorsDocumento7 pagineModule 013 Week005-Statement of Changes in Equity, Accounting Policies, Changes in Accounting Estimates and Errorsman ibeNessuna valutazione finora

- 4A. Financial Proposal Submission Form. 4B. Summary of Costs. 4C. Breakdown of CostDocumento6 pagine4A. Financial Proposal Submission Form. 4B. Summary of Costs. 4C. Breakdown of Costpankaj kadkolNessuna valutazione finora

- Chapter 1 MGMT481 - Summer 2021Documento23 pagineChapter 1 MGMT481 - Summer 2021Jelan AlanoNessuna valutazione finora

- Bus Ticket Invoice 1673864116Documento2 pagineBus Ticket Invoice 1673864116SP JamkarNessuna valutazione finora

- 1930 Hobart DirectoryDocumento82 pagine1930 Hobart DirectoryAnonymous X9qOpCYfiBNessuna valutazione finora

- Essay BusinessDocumento2 pagineEssay Businessali basitNessuna valutazione finora

- Ust Multiple Rework SpoilageDocumento6 pagineUst Multiple Rework SpoilageJessica Shirl Vipinosa100% (1)

- IFRS Metodo Del Derivado HipoteticoDocumento12 pagineIFRS Metodo Del Derivado HipoteticoEdgar Ramon Guillen VallejoNessuna valutazione finora

- Grade 8 EMS Classic Ed GuideDocumento41 pagineGrade 8 EMS Classic Ed GuideMartyn Van ZylNessuna valutazione finora

- Aped Manual Volume I 2012Documento463 pagineAped Manual Volume I 2012Arif Ahmed100% (1)

- Approved Employers - LahoreDocumento15 pagineApproved Employers - Lahoreraheel97Nessuna valutazione finora

- Data Cleaning With SSISDocumento25 pagineData Cleaning With SSISFreeInformation4ALLNessuna valutazione finora

- Air India (HRM) - Invitation Letter - 2 PDFDocumento2 pagineAir India (HRM) - Invitation Letter - 2 PDFNilesh Sanap100% (2)

- Cold Box Overview enDocumento18 pagineCold Box Overview enSasa DjordjevicNessuna valutazione finora

- Stevenson7ce PPT Ch03Documento86 pagineStevenson7ce PPT Ch03Anisha SidhuNessuna valutazione finora

- Economia - 2018-03Documento84 pagineEconomia - 2018-03Hifzan ShafieeNessuna valutazione finora

- Ansi Isa-S91.01-1995Documento12 pagineAnsi Isa-S91.01-1995jf2587Nessuna valutazione finora

- REBUTTAL REPORT OF DR. ROBERT McCORMICK IN SUPPORT OF ANTITRUST PLAINTIFFS' MOTION FOR CLASS CERTIFICATIONDocumento199 pagineREBUTTAL REPORT OF DR. ROBERT McCORMICK IN SUPPORT OF ANTITRUST PLAINTIFFS' MOTION FOR CLASS CERTIFICATIONInsideSportsLawNessuna valutazione finora

- Unit 2 Consumer BehaviourDocumento14 pagineUnit 2 Consumer Behaviournileshstat5Nessuna valutazione finora

- Cost AccountingDocumento57 pagineCost AccountingM.K. TongNessuna valutazione finora

- Chai Qawali AssignmentDocumento15 pagineChai Qawali AssignmentCadet SaqlainNessuna valutazione finora

- Deed of SaleDocumento7 pagineDeed of SaleRab AlvaeraNessuna valutazione finora

- MCQDocumento9 pagineMCQthaker richaNessuna valutazione finora

- Vishnu AgenciesDocumento2 pagineVishnu AgenciesBack-End MarketingNessuna valutazione finora