Potrebbero piacerti anche

- Q2 Audit ChecklistDocumento43 pagineQ2 Audit ChecklistBilly Croker100% (15)

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsDa EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNessuna valutazione finora

- Mid MonthDocumento4 pagineMid Monthcipollini50% (2)

- Credit Risk Modelling - A PrimerDocumento42 pagineCredit Risk Modelling - A PrimersatishdwnldNessuna valutazione finora

- Basel II and Credit RiskDocumento18 pagineBasel II and Credit RiskVasuki BoopathyNessuna valutazione finora

- RiskMetrics (Monitor) 1Documento40 pagineRiskMetrics (Monitor) 1Angel Gutiérrez ChambiNessuna valutazione finora

- 3 - 1-Asset Liability Management PDFDocumento26 pagine3 - 1-Asset Liability Management PDFAlaga ZelkanovićNessuna valutazione finora

- Asset Liability ManagementDocumento18 pagineAsset Liability Managementmahesh19689Nessuna valutazione finora

- Chapters 6-7 and DerivativesDocumento68 pagineChapters 6-7 and DerivativesLouise0% (1)

- Parts Ageing ReportDocumento3.193 pagineParts Ageing ReportPriyanka AggarwalNessuna valutazione finora

- Marketing Challenges in A Turbulent Business EnvironmentDocumento671 pagineMarketing Challenges in A Turbulent Business EnvironmentpervezkanjuNessuna valutazione finora

- Modern credit risk management techniquesDocumento5 pagineModern credit risk management techniquesmpr176Nessuna valutazione finora

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiDa EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNessuna valutazione finora

- Quantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskDa EverandQuantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskValutazione: 3.5 su 5 stelle3.5/5 (1)

- ALMDocumento15 pagineALMGaurav PandeyNessuna valutazione finora

- Credit Risk Mgmt. at ICICIDocumento60 pagineCredit Risk Mgmt. at ICICIRikesh Daliya100% (1)

- Intro To Credit Risk Exposure MeasurementDocumento36 pagineIntro To Credit Risk Exposure MeasurementALNessuna valutazione finora

- Standardized Approach For Counterparty Credit RiskDocumento2 pagineStandardized Approach For Counterparty Credit RiskjalutukNessuna valutazione finora

- Fundamental Review of The Trading Book: Briefing NotesDocumento5 pagineFundamental Review of The Trading Book: Briefing NotesDipank PandeNessuna valutazione finora

- Value at Risk - Theory and IllustrationsDocumento75 pagineValue at Risk - Theory and IllustrationsMohamed Amine ElmardiNessuna valutazione finora

- Asset Liability Management: in BanksDocumento44 pagineAsset Liability Management: in Bankssachin21singhNessuna valutazione finora

- KMV - Ved PureshwarDocumento45 pagineKMV - Ved PureshwarAmit KawleNessuna valutazione finora

- CH 6 Credit Risk Measurement and Management AnswersDocumento362 pagineCH 6 Credit Risk Measurement and Management AnswersTushar MehndirattaNessuna valutazione finora

- The Basel II IRB Approach For Credit PortfoliosDocumento30 pagineThe Basel II IRB Approach For Credit PortfolioscriscincaNessuna valutazione finora

- Capital and Risk Management Report 31 December 2011Documento68 pagineCapital and Risk Management Report 31 December 2011Sikandar GujjarNessuna valutazione finora

- Basel II-III Credit Risk Modelling and Validation Training BrochureDocumento7 pagineBasel II-III Credit Risk Modelling and Validation Training BrochuremakorecNessuna valutazione finora

- Basel IIIDocumento31 pagineBasel IIIRahul WaniNessuna valutazione finora

- Rating Credit Risks - OCC HandbookDocumento69 pagineRating Credit Risks - OCC HandbookKent WhiteNessuna valutazione finora

- Credit RiskDocumento57 pagineCredit RiskmefulltimepassNessuna valutazione finora

- Asset Liability Management Under Risk FrameworkDocumento9 pagineAsset Liability Management Under Risk FrameworklinnnehNessuna valutazione finora

- Introduction To VaRDocumento21 pagineIntroduction To VaRRanit BanerjeeNessuna valutazione finora

- ABCs of ABCP, 2009Documento42 pagineABCs of ABCP, 2009ed_nycNessuna valutazione finora

- DICO-IfRS 9 Modelling and ImplementationDocumento28 pagineDICO-IfRS 9 Modelling and ImplementationRadian Adhi100% (1)

- CH 5 MARKET RISK - VaRDocumento29 pagineCH 5 MARKET RISK - VaRAisyah Vira AmandaNessuna valutazione finora

- Pragya: The Best FRM Revision Course!Documento26 paginePragya: The Best FRM Revision Course!mohamedNessuna valutazione finora

- CREDIT RISK MODELLING CURRENT PRACTICES AND APPLICATIONSDocumento65 pagineCREDIT RISK MODELLING CURRENT PRACTICES AND APPLICATIONSPriya RanjanNessuna valutazione finora

- Credit Risk: Monetary Authority of SingaporeDocumento29 pagineCredit Risk: Monetary Authority of SingaporeNikhil ChandeNessuna valutazione finora

- Expected Shortfall - An Alternative Risk Measure To Value-At-RiskDocumento14 pagineExpected Shortfall - An Alternative Risk Measure To Value-At-Risksirj0_hnNessuna valutazione finora

- Bank's 2013-14 Credit Risk Policy Highlights Key ElementsDocumento14 pagineBank's 2013-14 Credit Risk Policy Highlights Key ElementsSaran Saru100% (2)

- FRM SwapsDocumento64 pagineFRM Swapsakhilyerawar7013Nessuna valutazione finora

- BIS and Basel Norms: ObjectiveDocumento6 pagineBIS and Basel Norms: ObjectiveJoyNessuna valutazione finora

- Capital Adequacy Framework for Indian BanksDocumento326 pagineCapital Adequacy Framework for Indian BanksucoNessuna valutazione finora

- Market Risk AssessmentDocumento59 pagineMarket Risk Assessmentclama2000Nessuna valutazione finora

- Introduction To Value-at-Risk PDFDocumento10 pagineIntroduction To Value-at-Risk PDFHasan SadozyeNessuna valutazione finora

- Monetary and Financial Economics: Interest Rate and Currency SwapsDocumento41 pagineMonetary and Financial Economics: Interest Rate and Currency SwapsIsmaîl TemsamaniNessuna valutazione finora

- Internal Credit Risk Rating Model by Badar-E-MunirDocumento53 pagineInternal Credit Risk Rating Model by Badar-E-Munirsimone333Nessuna valutazione finora

- Credit Risk Analysis - Control - GC - 2Documento176 pagineCredit Risk Analysis - Control - GC - 2Keith Tanaka MagakaNessuna valutazione finora

- Basel IV & CRR II: Revised Standardised Approach For Market RiskDocumento52 pagineBasel IV & CRR II: Revised Standardised Approach For Market RiskNasim AkhtarNessuna valutazione finora

- Market Risk SlidesDocumento80 pagineMarket Risk SlidesChen Lee Kuen100% (5)

- Counterparty LimitDocumento413 pagineCounterparty Limitmuhammad firmanNessuna valutazione finora

- The Non-Performing LoansDocumento34 pagineThe Non-Performing Loanshannory100% (1)

- Interest Rate SwapDocumento2 pagineInterest Rate SwapRahul Kumar TantwarNessuna valutazione finora

- Point-In-Time (PIT) LGD and EAD Models For IFRS9/CECL and Stress TestingDocumento16 paginePoint-In-Time (PIT) LGD and EAD Models For IFRS9/CECL and Stress TestingdavejaiNessuna valutazione finora

- Cva HedgingDocumento16 pagineCva HedgingjeanturqNessuna valutazione finora

- Introduction To Basel Iii: Implications and ConsequencesDocumento26 pagineIntroduction To Basel Iii: Implications and ConsequencesAakashNessuna valutazione finora

- Modeling of EAD and LGD: Empirical Approaches and Technical ImplementationDocumento21 pagineModeling of EAD and LGD: Empirical Approaches and Technical Implementationh_y02Nessuna valutazione finora

- Risk Management For Banking SectorDocumento46 pagineRisk Management For Banking SectorNaeem Uddin88% (17)

- Structured Products in The Swiss MarketDocumento51 pagineStructured Products in The Swiss Marketbenjamin100% (1)

- An Overview of Modeling Credit PortfoliosDocumento23 pagineAn Overview of Modeling Credit PortfoliosKhaledNessuna valutazione finora

- JP Morgan CreditMetricsDocumento16 pagineJP Morgan CreditMetricsKSNessuna valutazione finora

- An Actuarialmodel For Credit RiskDocumento17 pagineAn Actuarialmodel For Credit RiskMiguel RevillaNessuna valutazione finora

- CLO Investing: With an Emphasis on CLO Equity & BB NotesDa EverandCLO Investing: With an Emphasis on CLO Equity & BB NotesNessuna valutazione finora

- Managing Liquidity in Banks: A Top Down ApproachDa EverandManaging Liquidity in Banks: A Top Down ApproachNessuna valutazione finora

- The Impact of Mergers and Acquisitions On Acquirer PerformanceDocumento10 pagineThe Impact of Mergers and Acquisitions On Acquirer Performancemadnansajid87650% (1)

- Impact of Risk Management On Non-Performing Loans and Profitability of Banking Sector of PakistanDocumento9 pagineImpact of Risk Management On Non-Performing Loans and Profitability of Banking Sector of Pakistanmadnansajid8765Nessuna valutazione finora

- PIA Quantitative and Quality AnalysisDocumento62 paginePIA Quantitative and Quality Analysismadnansajid876525% (4)

- National Bank of PakistanDocumento44 pagineNational Bank of Pakistanmadnansajid8765Nessuna valutazione finora

- HRMDocumento37 pagineHRMmadnansajid8765Nessuna valutazione finora

- Bank Al - Falah Internship ReportDocumento92 pagineBank Al - Falah Internship Reportmadnansajid8765Nessuna valutazione finora

- PTCLDocumento88 paginePTCLmadnansajid8765Nessuna valutazione finora

- "Develop The Scenario of Financial Transaction Which Reflects at Least Five Types of Risk and Discuss Their Interrelation As Well.Documento2 pagine"Develop The Scenario of Financial Transaction Which Reflects at Least Five Types of Risk and Discuss Their Interrelation As Well.madnansajid8765Nessuna valutazione finora

- HRMDocumento21 pagineHRMmadnansajid8765Nessuna valutazione finora

- Dnan Ajid: Address: Asad Colony Sheikhupura Road Gujranwala, Pakistan. Contact #: 0312-6150001 Email AddressDocumento2 pagineDnan Ajid: Address: Asad Colony Sheikhupura Road Gujranwala, Pakistan. Contact #: 0312-6150001 Email Addressmadnansajid8765100% (1)

- Culture of An Organization ..... BOSS Moulded FurnitureDocumento31 pagineCulture of An Organization ..... BOSS Moulded Furnituremadnansajid8765Nessuna valutazione finora

- Fast Food Industry Complete AnalysisDocumento32 pagineFast Food Industry Complete Analysismadnansajid8765100% (1)

- Mitchell's Ratio AnalysisDocumento3 pagineMitchell's Ratio Analysismadnansajid8765Nessuna valutazione finora

- Muslim Commercial Bank Internship ReportDocumento69 pagineMuslim Commercial Bank Internship Reportmadnansajid8765Nessuna valutazione finora

- Final ProjectDocumento33 pagineFinal Projectmadnansajid8765Nessuna valutazione finora

- Managerial Finance Basic TermsDocumento11 pagineManagerial Finance Basic Termsmadnansajid8765Nessuna valutazione finora

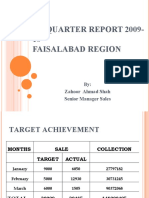

- 3rd Quarter Report 2009-10Documento22 pagine3rd Quarter Report 2009-10madnansajid8765Nessuna valutazione finora

- Kinnow Processing Plant (Sitrus Fruit)Documento26 pagineKinnow Processing Plant (Sitrus Fruit)madnansajid8765Nessuna valutazione finora

- Telenor Pakistan Training and DevelopmentDocumento28 pagineTelenor Pakistan Training and Developmentmadnansajid8765100% (1)

- Telenor Human Resource ManagementDocumento55 pagineTelenor Human Resource ManagementRaheela MuhammadNessuna valutazione finora

- Report On Telenor (Human Resource Management)Documento21 pagineReport On Telenor (Human Resource Management)madnansajid8765Nessuna valutazione finora

- Online Recruitment in Telenor PakistanDocumento38 pagineOnline Recruitment in Telenor Pakistanmadnansajid8765Nessuna valutazione finora

- Project On UBLDocumento10 pagineProject On UBLmadnansajid8765Nessuna valutazione finora

- Project On NestleDocumento7 pagineProject On Nestlemadnansajid8765Nessuna valutazione finora

- Company MeetingDocumento9 pagineCompany Meetingmadnansajid8765Nessuna valutazione finora

- IMF & Developing CountriesDocumento6 pagineIMF & Developing Countriesmadnansajid8765Nessuna valutazione finora

- Project On Macro PakistanDocumento8 pagineProject On Macro Pakistanmadnansajid8765Nessuna valutazione finora

- Project On PESPIDocumento13 pagineProject On PESPImadnansajid8765Nessuna valutazione finora

- Project On Allied Bank of PakistanDocumento23 pagineProject On Allied Bank of Pakistanmadnansajid8765Nessuna valutazione finora

- Strategic Business AnalysisDocumento19 pagineStrategic Business AnalysisErica Piga ButacNessuna valutazione finora

- Cybersecurity Policy FrameworkDocumento44 pagineCybersecurity Policy FrameworkAhmed100% (1)

- GAP Polymers-Abdelrahman Naji - Sara Gamal - Ahmed Mahmoud Aly - Abdel Halim AllamDocumento30 pagineGAP Polymers-Abdelrahman Naji - Sara Gamal - Ahmed Mahmoud Aly - Abdel Halim AllamAhmed AlyNessuna valutazione finora

- BAT AR20 F 2018 Financial StatementsDocumento138 pagineBAT AR20 F 2018 Financial StatementsK DonovichNessuna valutazione finora

- Applied Social Sciences, Phoenix Pub. House: Pp. 245-253 HUMSS: P 610Documento5 pagineApplied Social Sciences, Phoenix Pub. House: Pp. 245-253 HUMSS: P 610Angel Dela CruzNessuna valutazione finora

- QCOSDocumento18 pagineQCOSYou UZBNessuna valutazione finora

- PAC: Choosing the Best Procurement RouteDocumento40 paginePAC: Choosing the Best Procurement RouteYani100% (1)

- OPMAN - Chapter 10 (ISO 9000 - Quality Management System)Documento28 pagineOPMAN - Chapter 10 (ISO 9000 - Quality Management System)polxrixNessuna valutazione finora

- Cisco Change Management Best PracticesDocumento14 pagineCisco Change Management Best PracticessmuliawNessuna valutazione finora

- Module 3 A Sustaining Natural Resources and Environmental Quality 3Documento65 pagineModule 3 A Sustaining Natural Resources and Environmental Quality 3PRAVIN GNessuna valutazione finora

- Gann Plan: Trading LetterDocumento5 pagineGann Plan: Trading Letterchanu100% (3)

- Proposal Writing Simplified For NGOs in Developing Countries by FundsforngosDocumento17 pagineProposal Writing Simplified For NGOs in Developing Countries by FundsforngosDimitri Sekhniashvili100% (1)

- Designation As Alternate DRRM CoordinatorDocumento1 paginaDesignation As Alternate DRRM CoordinatorMICHEROSE SALADAGANessuna valutazione finora

- Audit Evidence, Audit Sampling Dan Working PaperDocumento42 pagineAudit Evidence, Audit Sampling Dan Working PaperMoza PangestuNessuna valutazione finora

- Child Safe Standards GuideDocumento52 pagineChild Safe Standards GuideÀlexNessuna valutazione finora

- Preface TYPEDocumento77 paginePreface TYPEmanishsaxena88Nessuna valutazione finora

- Qa Imco Hse Ms QT 001 Hse Management SystemDocumento21 pagineQa Imco Hse Ms QT 001 Hse Management SystemFrancis Enriquez TanNessuna valutazione finora

- Pleat - Panel Brochure AFP 1 102BDocumento8 paginePleat - Panel Brochure AFP 1 102BluisNessuna valutazione finora

- Chapter 8 254-262Documento9 pagineChapter 8 254-262Anthon AqNessuna valutazione finora

- The Economic Institutions of Capitalism: Firms, Markets and Relational Contracting Oliver E. WilliamsonDocumento19 pagineThe Economic Institutions of Capitalism: Firms, Markets and Relational Contracting Oliver E. WilliamsonyoobygigandetNessuna valutazione finora

- Ai Research PaperDocumento6 pagineAi Research Paperapi-712836484Nessuna valutazione finora

- 67551b61c24b8db754b170e31c7fc079Documento48 pagine67551b61c24b8db754b170e31c7fc079Leonardo BritoNessuna valutazione finora

- Credit AppraisalDocumento49 pagineCredit AppraisalRam Vishrojwar50% (2)

- VAL - 170401 - BMAA VAL Activity 3 URS - Template PDFDocumento10 pagineVAL - 170401 - BMAA VAL Activity 3 URS - Template PDFDineshNessuna valutazione finora

- © The Institute of Chartered Accountants of IndiaDocumento9 pagine© The Institute of Chartered Accountants of IndiaIBBF FitnessNessuna valutazione finora