Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Because of The Doubtful Nature of Some Debts P RudentDocumento1 paginaBecause of The Doubtful Nature of Some Debts P RudentAmit PandeyNessuna valutazione finora

- Chapter 4Documento15 pagineChapter 4nicole bancoro100% (1)

- Financial StatementsDocumento30 pagineFinancial StatementsPrincess BersaminaNessuna valutazione finora

- Final AccountsDocumento27 pagineFinal AccountsNafis Siddiqui100% (1)

- BLTDocumento30 pagineBLTJemson Yandug0% (1)

- Accounting 5Documento38 pagineAccounting 5Shehara GamlathNessuna valutazione finora

- Readymade Chappathi Project ReportDocumento13 pagineReadymade Chappathi Project ReportachusmohanNessuna valutazione finora

- CLO Interest - Aug 09Documento18 pagineCLO Interest - Aug 09rlinskiNessuna valutazione finora

- Financial Accounting: Tools For Business Decision Making (6th Ed.) .Documento44 pagineFinancial Accounting: Tools For Business Decision Making (6th Ed.) .Avonda Lashell Trader67% (3)

- Application For Occupancy: Form Valid For Georgia Apartment Association Members OnlyDocumento4 pagineApplication For Occupancy: Form Valid For Georgia Apartment Association Members OnlyPatricia WellsNessuna valutazione finora

- C4 GoldenDocumento4 pagineC4 GoldenJonuelin Infante100% (1)

- Export and Import FinancingDocumento4 pagineExport and Import FinancingTamzid AlifNessuna valutazione finora

- 14 Interest Rate and Currency SwapsDocumento28 pagine14 Interest Rate and Currency SwapslalitjaatNessuna valutazione finora

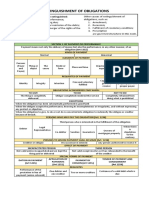

- Summary Note - EXTINGUISHMENT OF OBLIGATIONSDocumento8 pagineSummary Note - EXTINGUISHMENT OF OBLIGATIONSGiah Mesiona100% (2)

- Financial Statements Year Ended December 31, 20X5: ABC CompanyDocumento11 pagineFinancial Statements Year Ended December 31, 20X5: ABC CompanysaraNessuna valutazione finora

- Accounting Theory Chapter 11 - GodfreyDocumento40 pagineAccounting Theory Chapter 11 - GodfreyRozanna Amalia100% (1)

- Statement of Cash FlowsDocumento6 pagineStatement of Cash FlowsJustine VeralloNessuna valutazione finora

- Simple Interest (LOD 01) : Test Series at For Tricks and Approximation Techniques Refer Sessions of Dr. Kiran DerleDocumento9 pagineSimple Interest (LOD 01) : Test Series at For Tricks and Approximation Techniques Refer Sessions of Dr. Kiran DerleG R Shanker SaiNessuna valutazione finora

- NFTs in Real EstateDocumento3 pagineNFTs in Real EstateOnkita GhoshNessuna valutazione finora

- Cash Flow and Fund Flow StatementDocumento23 pagineCash Flow and Fund Flow StatementRishul BhasinNessuna valutazione finora

- Investment Management: UNIT-2 Securities MarketsDocumento10 pagineInvestment Management: UNIT-2 Securities MarketsChand BashaNessuna valutazione finora

- Balance Sheet Income StatementDocumento50 pagineBalance Sheet Income Statementgurbaxeesh0% (1)

- Profitability INTRODUCTIONDocumento19 pagineProfitability INTRODUCTIONDEEPANessuna valutazione finora

- PranDocumento43 paginePranRaja Rumi70% (10)

- Gul AhmedDocumento18 pagineGul AhmedMINDPOW100% (1)

- Risk in Capital Structure Arbitrage 2006Documento46 pagineRisk in Capital Structure Arbitrage 2006jinwei2011Nessuna valutazione finora

- Chapter 3Documento18 pagineChapter 3Annur SofeaNessuna valutazione finora

- Ch03 Money MarketDocumento8 pagineCh03 Money MarketPaw VerdilloNessuna valutazione finora

- 0130 G R No 150197 July 28 2005 Prudential Bank Vs Don A AlviarDocumento5 pagine0130 G R No 150197 July 28 2005 Prudential Bank Vs Don A AlviarRandy SantosNessuna valutazione finora

- Donald Kieso Chapt 5Documento76 pagineDonald Kieso Chapt 5Ridha Ansari100% (1)